Deutsche Telekom AG – Annual report – 31 December 2025

Industry: telecoms

43 Financial instruments and risk management (extract)

Hedge accounting

Fair value hedges. To hedge the fair value risk of fixed-income liabilities, Deutsche Telekom primarily uses interest rate swaps (pay variable, receive fixed) denominated in EUR and USD. Fixed-income bonds denominated in EUR and USD were designated as hedged items. The changes in the fair values of the hedged items resulting from changes in the EURIBOR or USD SOFR swap rate are offset against the changes in the value of these interest rate swaps. In addition, cross-currency swaps mainly in the EUR/USD and EUR/GBP currency pairs, are designated as fair value hedges, which convert fixed-income foreign currency bonds into variable-interest EUR bonds to hedge the interest rate and currency risk. The changes in the fair value of the hedged items resulting from changes in the USD SOFR and GBP SONIA swap rate as well as the USD and GBP exchange rate, are offset against the changes in the value of these cross-currency swaps. The aim of the fair value hedges is thus to transform the fixed-income bonds into variable-interest debt, thus hedging the fair value (interest rate risk and currency risk) of these financial liabilities. Credit risks are not part of the hedging and, on account of Deutsche Telekom’s rating, have only an immaterial effect on the changes in the fair value of the hedged item.

Cash flow hedges – interest rate risks. Deutsche Telekom mainly uses payer interest rate swaps and forward-payer interest rate swaps (pay fixed, receive variable) to hedge the cash flow risk of existing and future debt. The interest payments to be made in the hedging period are the hedged items and are recognized in profit or loss in the same period. Hedged items may be individual liabilities, portfolios of liabilities, or combinations of liabilities and derivatives (aggregate risk exposure). The changes in the cash flows of the hedged items resulting from changes in the USD SOFR rate and the EURIBOR rate are offset against the changes in the cash flows of the interest rate swaps. The aim of this hedging is to transform the variable-interest bonds into fixed-income debt, thus hedging the cash flows of the financial liabilities. Credit risks are not part of the hedging and, on account of Deutsche Telekom’s rating, have only an immaterial effect on the changes in the fair value of the hedged item.

Cash flow hedges – currency risks. Deutsche Telekom entered into currency derivative and cross-currency swaps (pay fixed, receive variable) to hedge cash flows not denominated in a functional currency. The payments in foreign currency to be made in the hedging period are the hedged items and are recognized in profit or loss in the same period. The terms of the hedging relationships will end in the years 2026 through 2045. In the case of rolling cash flow hedges for hedging currency risks, short-term currency forwards are entered into, which are then extended by means of follow-up transactions.

At each reporting date, the effectiveness of the fair value and cash flow hedges is reviewed prospectively based on the main contractual features and recognized by using the dollar offset test. All hedging relationships were sufficiently effective as of the reporting date.

Hedging of a net investment. To hedge the net investment in T‑Mobile US against fluctuations in the U.S. dollar spot rate, a net investment hedge of up to a nominal USD 1.3 billion was designated in the reporting period. Short-term currency forwards were used as hedging instruments (“pay U.S. dollars – receive euros”) with a change in the U.S. dollar spot rate being designated as the hedged risk. Any changes in value of the hedged net investment resulting from changes in the U.S. dollar spot exchange rate were offset by changes in the value of the currency forwards. At each reporting date, effectiveness was reviewed prospectively based on the key characteristics and is determined retrospectively in the form of a dollar offset test. As of the reporting date, the hedging volume had declined to zero. The hedges of the net investment in T‑Mobile US against fluctuations in the U.S. dollar spot rate de-designated in prior periods did not generate any effects in 2025. The amounts recognized under cumulative other comprehensive income would be reclassified to profit or loss in the event of the disposal of T‑Mobile US.

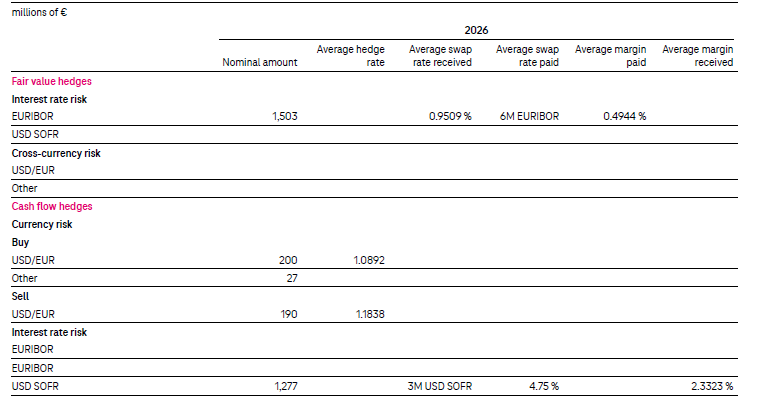

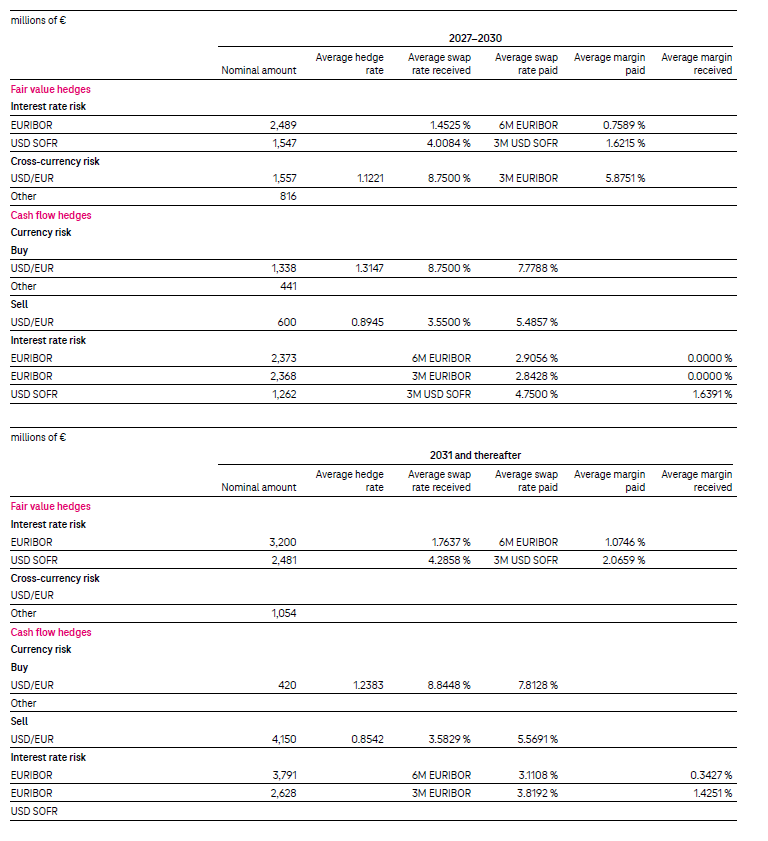

Conditions of derivative financial instruments in hedging relationshipsa

a In addition to the main hedges in euros and U.S. dollars, there are also hedges in the following currencies: pound sterling, Swiss francs, Norwegian kroner, Hong Kong dollars, and Australian dollars, which cumulate under “Other.”

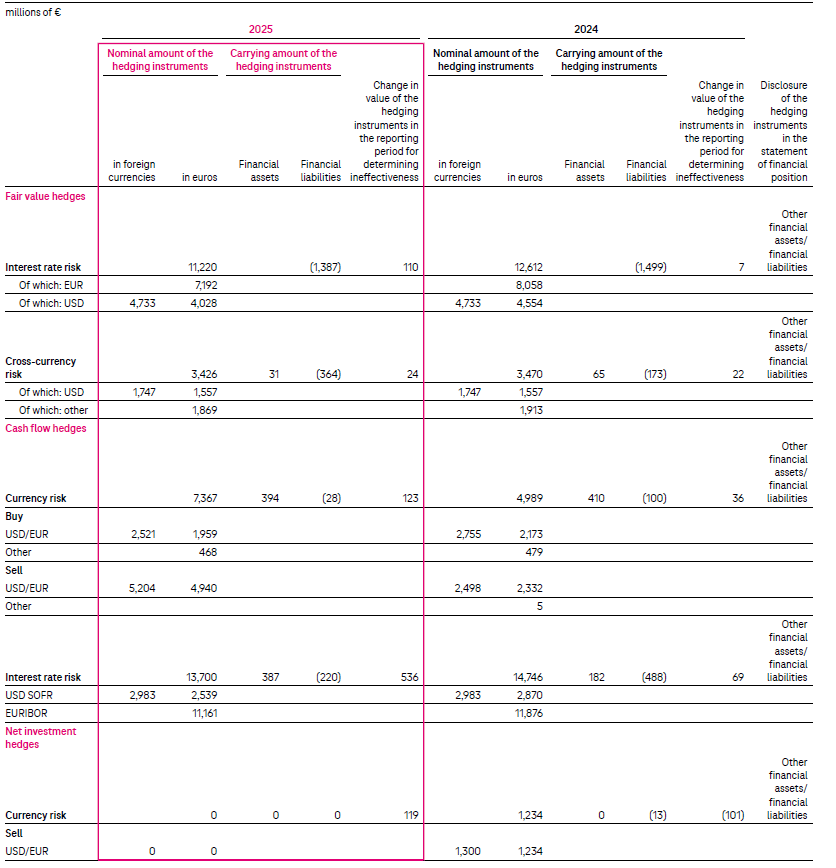

Nominal and carrying amounts of derivative financial instruments in hedging relationshipsa

a In this and the following tables on hedging relationships, losses are shown as negative amounts unless explicitly stated otherwise.

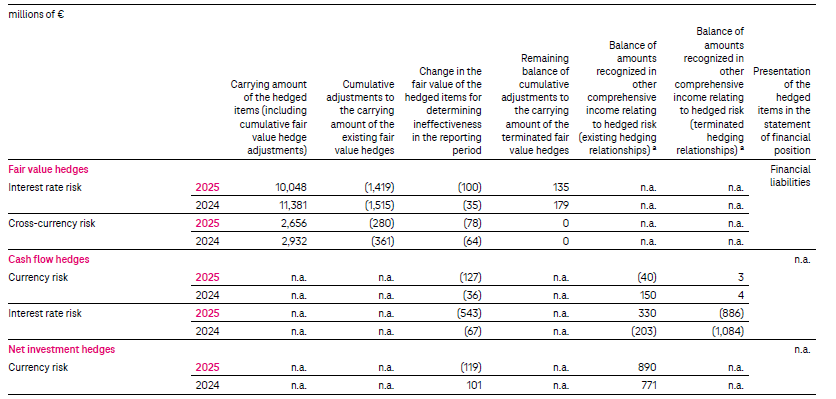

Disclosures on hedged items in hedging relationships

a Figures include non-controlling interests.

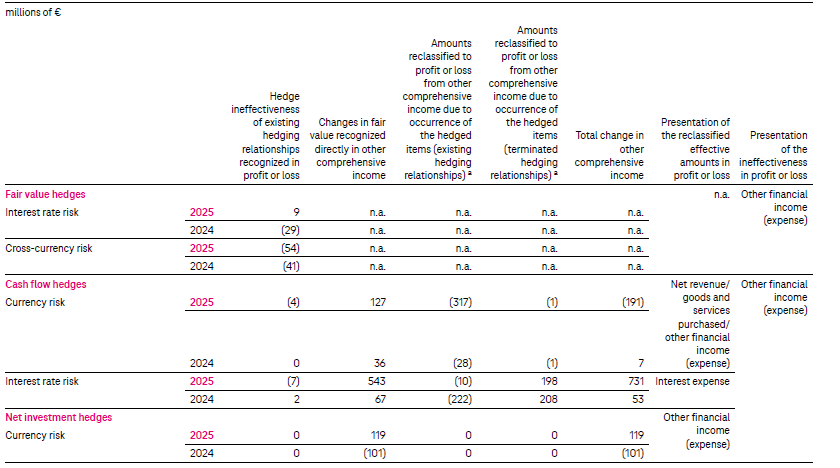

Gains or losses from hedging relationships

a Negative amounts represent gains in the consolidated income statement.

The recorded ineffectiveness in the consolidated income statement mainly resulted from the different discount rates of the hedged items (fixed-income) and designated hedging instruments (fixed-income and variable-interest). Furthermore, cross-currency interest rate hedges are impacted by effects from cross-currency basis spreads, which are included in the hedging instruments, but not in the hedged items. For some hedges, the characteristics of hedging instruments and hedged items differ, resulting in ineffectiveness. The relative amounts of the ineffectiveness are not expected to increase significantly in the future. Furthermore, there are no other potential sources of ineffectiveness.

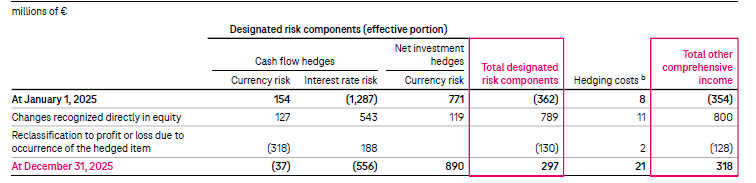

Reconciliation of total other comprehensive income from hedging relationshipsa

a Figures include non-controlling interests.

b The hedging costs relate entirely to cross-currency basis spreads.