Senior plc – Half year report – 30 June 2025

Industry: manufacturing

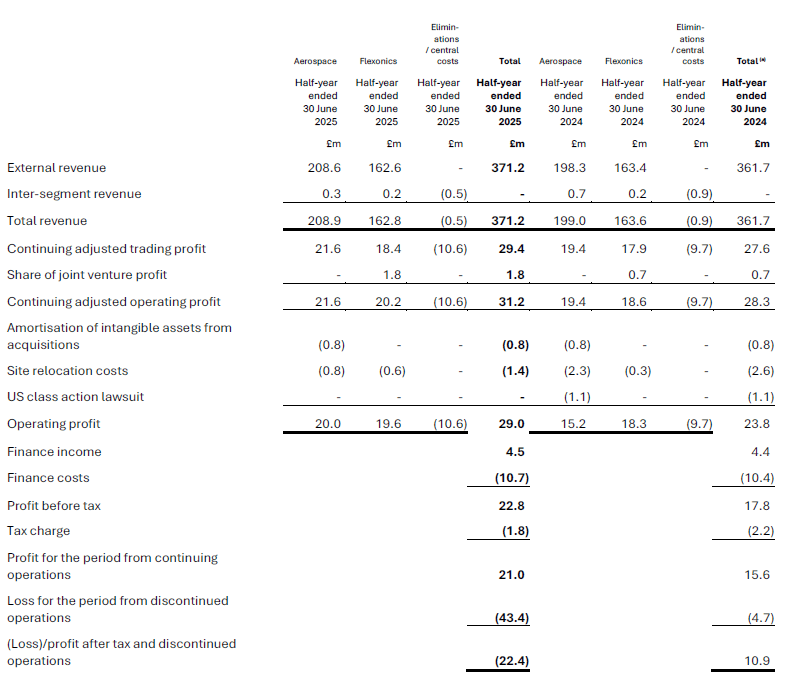

3. Segmental analysis

The Group reports its segment information as two operating divisions according to the market segments they serve, Aerospace and Flexonics, which is consistent with the oversight employed by the Executive Committee. The chief operating decision maker, as defined by IFRS 8, is the Executive Committee. The Group is managed on the same basis, as two operating divisions.

Business Segments

Segment information for revenue and operating profit and a reconciliation to the Group profit after tax is presented below:

a) Comparative information has been re-presented due to discontinued operations, see Note 18.

Trading profit and adjusted trading profit is operating profit and adjusted operating profit respectively before share of joint venture profit. See Note 4 for the derivation of adjusted operating profit.

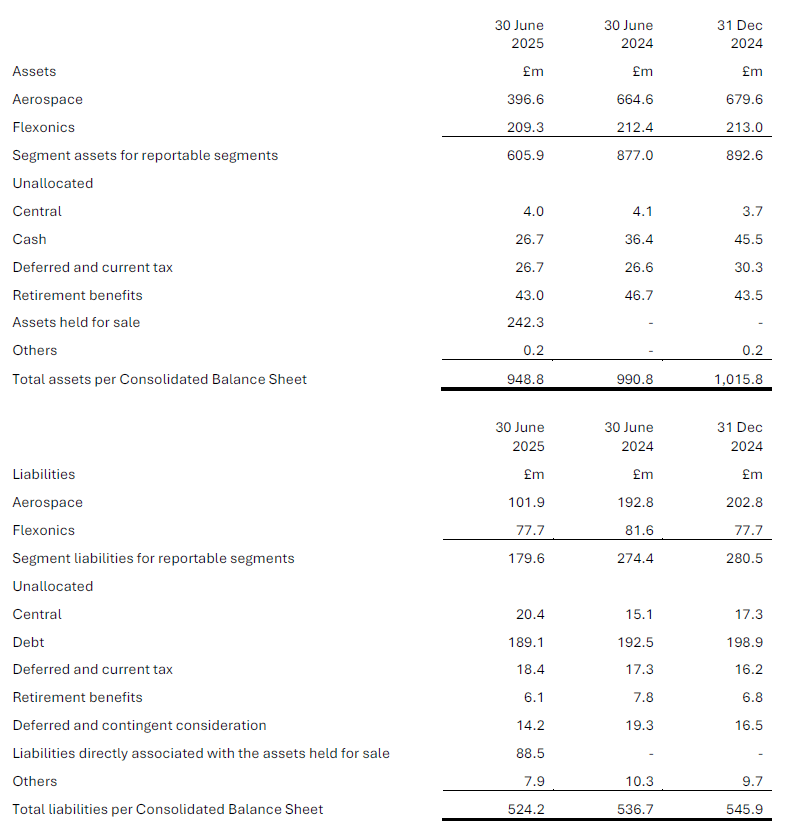

Segment information for assets and liabilities is presented below.

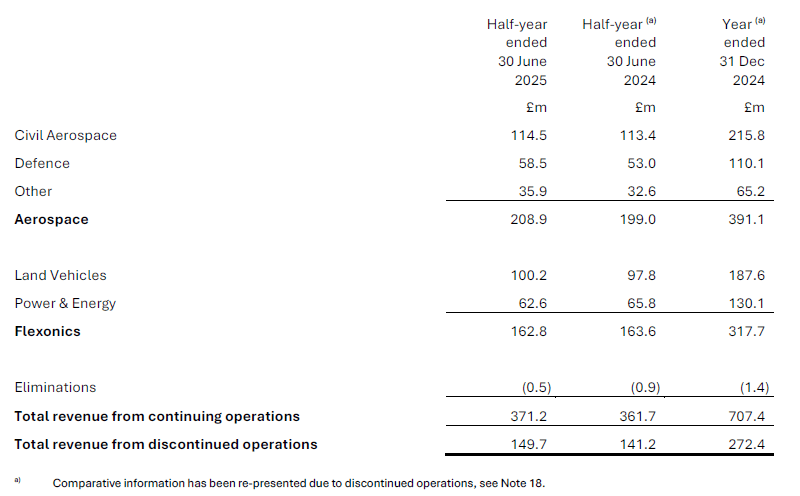

Total revenue is disaggregated by market sectors as follows:

Other Aerospace comprises space and non-military helicopters and other markets, principally including semiconductor, medical, and industrial applications.