Greencore Group plc – Annual report – 29 September 2017

Industry: food and drink

Directors’ Report (extract)

CORPORATE GOVERNANCE

Statements by the Directors relating to the Group’s application of corporate governance principles, compliance with the provisions of the 2016 Code and the Irish Corporate Governance Annex (the ‘Annex’), the Group’s system of internal controls and the adoption of the going concern basis in the preparation of the Financial Statements are set out on pages 56 to 62, 94 to 100 and 103 and 104.

Greencore Group plc is registered in Ireland and as an Irish incorporated company it is not subject to the UK executive remuneration requirements as set out in the Large and Medium-sized Companies and Groups (Accounts and Reports) (Amendment) Regulations 2013. Nonetheless, in order to ensure transparency to all of our stakeholders, we have sought to comply with these requirements on a voluntary basis, to the extent possible under Irish law. The Report on Directors’ Remuneration is contained on pages 63 to 93.

ANNUAL REPORT ON REMUNERATION (extract)

SHAREHOLDER VOTING

At the 2017 AGM, the FY16 Annual Report on Remuneration received 98.0% support from shareholders, whilst the new remuneration Policy received 59.9% support. Furthermore, the amendments to the Group’s PSP Rules received 60.7% votes in favour.

The table below shows the voting outcomes of the resolutions proposed at the 2017 AGM in relation to remuneration.

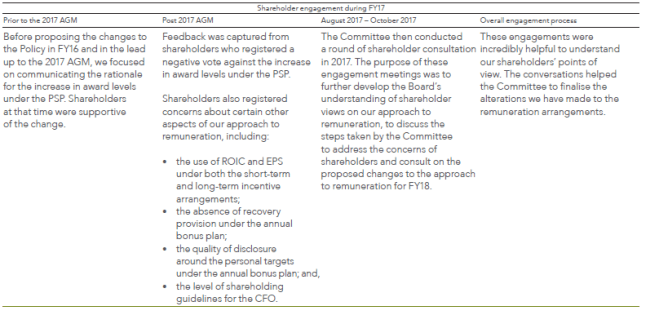

After the 2017 AGM, the Committee reviewed the voting outcome to determine our shareholders’ key concerns, and how it would address them.

Shareholders’ reasons for opposing the Policy primarily related to the increased award opportunity under the PSP, and the FY17 targets. The Committee consulted shareholders on this change in September 2016, receiving broad support at that time. However, the composition of our shareholder base changed significantly following the rights issue in December 2016, shortly before the 2017 AGM, and the level of support received at the 2017 AGM was impacted by this shift.

The Committee continues to believe that the revisions to Policy are appropriate and fair, and ultimately in the best interest of shareholders. Further explanations of the changes are set out in the Chair’s Letter on pages 63 to 66. During the year, the Committee undertook a consultation and made a number of changes aligned with best practice to remuneration for FY18 and future years, in response to feedback. Clawback has been introduced on incentive cycles for FY18 onwards, and malus provisions have been extended to apply to deferred bonus awards as well as the PSP. We have also strengthened our shareholding guidelines to 2x salary for all Executive Directors and diversified the performance measures under the PSP.

The Committee is committed to meaningful engagement with our shareholders as part of our approach to strong governance, and continues to welcome comments from shareholders.

Report on Directors’ Remuneration (extract)

LETTER FROM THE REMUNERATION COMMITTEE CHAIR (extract)

DEAR SHAREHOLDER,

Against the backdrop of a significant vote against two of our remuneration resolutions at the 2017 Annual General Meeting (‘2017 AGM’) and with a refreshed Committee, I have taken the opportunity to undertake a comprehensive review of our remuneration approach and framework.

The Committee and I have consulted and considered carefully the input from our shareholders and have sought to respond by updating the principles which will guide our remuneration decisions and incorporate a number of changes to the implementation of our remuneration Policy (‘2017 Policy’ or ‘Policy’) for FY18. Our Policy was developed to ensure a clear link between the delivery of our strategy and pay outcomes. From our discussions with shareholders we recognise the need to provide more information to show how our strategic priorities are reflected in our performance targets and consistent with actual payout levels. Throughout this report we have sought to provide more information on how our Committee decisions reflect the strategic goals and direction of the business.

The Committee and I have worked hard to ensure that our remuneration disclosures are clear and relevant to shareholders. In doing so, we examined the results of the 2017 AGM, tested our approach to remuneration and undertook an invaluable engagement exercise with shareholders. We are committed to ensuring that we are transparent about how pay and performance is reported at Greencore and how decisions made by the Committee continue to support the strategic direction of the business.

RESULTS OF THE 2017 AGM

At the 2017 AGM, shareholders endorsed the Annual Report on Remuneration with 98% votes cast in favour. In addition to our Annual Report on Remuneration, we proposed the new 2017 Policy to replace the previously approved 2015 Policy. The 2017 Policy increased the maximum award level under the Performance Share Plan (‘PSP’) from 100% to 200% of salary and 150% of salary for the Chief Executive Officer (‘CEO’) and Chief Financial Officer (‘CFO’) respectively and introduced for the first time an additional two year holding period for awards, after a three year performance and vesting period, under the PSP. While 59.9% of shareholders supported the introduction of the 2017 Policy, 40.1% voted against. The amended PSP Rules incorporating these changes received 60.7% approval. The scale of votes against the resolutions was disappointing for the Committee as we had engaged with our major shareholders prior to the finalisation of the 2017 Policy proposal in September 2016 and had received broad support for the changes outlined.

We have had very strong and consistent support for our remuneration approach before the 2017 AGM vote so the Committee and the Board immediately instigated a full analysis of the vote and feedback received, and committed to consult with our shareholders and proxy advisors to understand why a significant minority felt they could not support the 2017 Policy. Following our review of feedback and having discussed this with a large number of shareholders during our consultation the primary reason outlined was the scale of the increase in the PSP opportunity with no detailed rationale to show that there was a commensurate increase in targets. We did not make it clear that the stretch to achieve this potentially bigger pay out was increasing significantly. The increased scale of the business and overall competitiveness of our pay levels in comparison to relevant external market data were important considerations in our proposed Policy change and considered necessary to motivate, retain and appropriately reward our executive management to execute our strategy in an increasingly competitive market for top talent.

To ensure there remained appropriate stretch in the target metrics relating to the increased PSP opportunity, the Committee reviewed the strategic plans and determined there should be no change to the targets proposed for the awards granted in February 2017. This represents considerable stretch over and above previous target levels given the significant step up in capital invested in FY16 (including seven new manufacturing facilities commissioned, built or acquired during the year) and reflecting the normal timescale for new facilities to ramp up to full capacity which means a time lag before anticipated growth and returns are fully delivered.

The overall level of 200% of salary remains in line with FTSE 250 companies. Additional issues raised by shareholders were the overlap of performance measures in both long and short term incentives, the lack of some best practice features including malus and clawback in our Policy and the desire for more transparency on personal bonus targets.

It is clear from the 2017 AGM vote and our consultations that the disclosure in our FY16 Annual Report did not provide sufficient detail or rationale to all of our shareholders on the strategic and operational context for the change proposed in the 2017 Policy. An additional challenge was the significant number of new Greencore shareholders following the rights issue in December 2016 which resulted in considerable churn in the shareholder base before the 2017 AGM vote. After the 2017 AGM it became clear that there were varying levels of understanding of the strategic context influencing our proposals amongst some new shareholders.

During our consultation with shareholders, and throughout this report, we have sought to explain the background to the Policy changes in more detail. Following a period of sustained and substantial growth, the Committee continues to believe that the PSP opportunity is at an appropriate level to incentivise future long-term performance for the Company in line with our vision to be a fast-growing international convenience food leader.

We also explained that our 2017 Policy proposal introduced for the first time a holding period of two further years post vesting for all PSP awards. This extends our long-term incentive time horizon to five years which provides greater alignment with the long term interests of our shareholders and with our long-term strategy.

REVIEW OF REMUNERATION PRINCIPLES AND PROPOSALS FOR FY18 EXECUTIVE REMUNERATION

During our review of the remuneration arrangements, the Committee revisited our remuneration principles. The Committee sought to identify the most appropriate principles for the business, taking into account its underlying values set out in The Greencore Way, specifically People at the Core and the interests of stakeholders. Going forward, the Committee will seek to ensure that our remuneration framework remains aligned with the following overarching principles:

- Alignment and fairness;

- Pay-for-performance; and

- Transparency and simplicity.

Full details of how we intend to operate these in practice are outlined on page 69.

Following a review of Greencore’s approach to remuneration and taking into account the feedback from shareholders, the Committee is proposing a number of changes for FY18 executive remuneration, which I detail below.

Proposed changes to FY18 remuneration were:

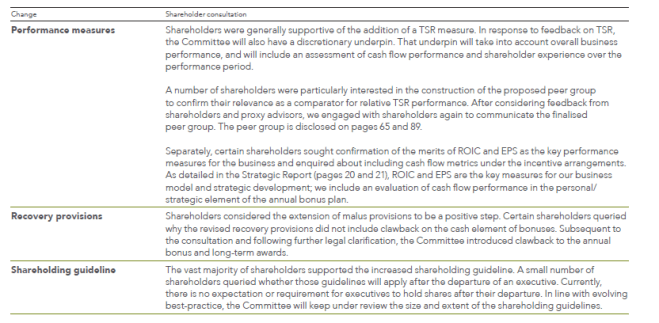

- the introduction of Total Shareholder Return (‘TSR’) as an additional measure for our long-term PSP awards, which will further augment alignment with shareholders and diversify the metrics used under the PSP;

- the extension of the malus provisions to cover short-term bonus as well as long-term PSP, which will strengthen the ability of the Company to withhold or forfeit remuneration in certain circumstances;

- increasing the shareholding guideline to 2x salary for the CFO which will strengthen the alignment between his interests and those of shareholders, and brings them in line with market practice and guidelines for the CEO; and

- a reduction in the Return on Invested Capital (‘ROIC’) target to take into account the intensive capital investment program and Peacock Foods acquisition. The new target ranges reflect the medium term downward impact on ROIC as a result of the considerable increase in our invested capital.

SHAREHOLDER ENGAGEMENT ON FY18 PROPOSALS

The Committee contacted shareholders who hold circa 55% of our issued share capital as well as the Investment Association, ISS and Glass Lewis with an outline of our proposed changes and requested a meeting to obtain their feedback and input. During this process we received feedback from shareholders representing circa 36% of our issued share capital, and the proxy agencies, from which we received very valuable input. The Board Chairman and I carried out direct consultations which included a presentation on the current Group strategy so the context of our performance measures and metrics was fully explained. Shareholders were broadly supportive of our overall remuneration Policy and approach and how it links with our current strategic priorities.

Our engagement provided some wide ranging views on remuneration in general and specifically in relation to the Group (with some divergent views between our US and UK shareholders) as detailed below on page 81. The Committee will keep all of these views under consideration.

Overall, our key proposals to apply to FY18 executive remuneration were viewed positively. Following the feedback from the consultations, the Committee re-examined recovery provisions. In addition to the extension of the malus provision, the Committee also agreed to introduce clawback on all future bonuses and PSP awards.

Throughout the consultation much of our discussions related to the introduction of TSR and the change in performance targets.

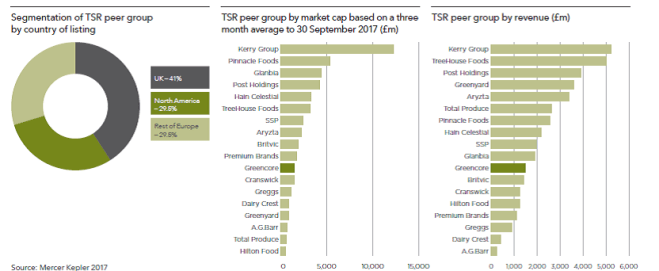

TSR PEER GROUP

In electing to include a TSR component under the PSP, the Committee was conscious of the requirement to determine appropriate peers to compare our TSR performance against. After careful consideration, the Committee has determined that 17 listed companies will comprise the peer group under the TSR measure for FY18 awards, as set out below.

The peer companies are representative of the sector we operate in and, most significantly, are companies who face similar business challenges. It includes a majority of UK companies together with other European peers. We have also included five US peers. While the Committee was aware of concerns from some stakeholders on the inclusion of companies domiciled in a different location, we now have a substantial US business with approximately 40% of our revenue stream deriving from the US market.

PERFORMANCE TARGETS

A central aspect of our consultation with shareholders was the target range for the ROIC measure under the PSP. In December 2016, we completed the acquisition of Peacock Foods for $747.5m, which included a significant rights issue. In addition to the changes to the remuneration framework outlined, the Committee spent significant time determining what impact the Peacock Foods acquisition would have on our remuneration arrangements and, particularly, the targets under our incentive schemes. The Committee has sought to ensure that the targets in place are suitably stretching while reflecting the future expected performance of our enlarged business. After careful consideration, Adjusted Earnings per Share (‘EPS’) targets for the PSP awards to be granted in December 2017 will remain unchanged (at 5% p.a. at threshold and 15% p.a. for maximum vesting). However, for the third of the award based on ROIC performance, the targets have been reduced to 10% at threshold and 13% for maximum vesting.

As discussed previously, the invested capital of the business has expanded considerably in both FY16 (11%) and FY17 (31%). The target ranges reflect the medium term downward impact on ROIC as a result of the considerable increase in our invested capital. This logic and the detailed analysis behind it was discussed in many of the meetings with our shareholders, who recognised the need to adjust the targets as a result of the disconnect between the level of capital being invested by the business and the delay in the increased returns that this investment will generate over time in line with our long-term strategy.

Based on the increase in issued share capital during FY17, the Committee is satisfied that the target range under the EPS measure is at least as difficult to achieve as under previous awards.

The Committee is fully aware of the sensitivities around the lowering of performance targets among shareholders and proxy advisors. In determining the revisions to the targets, the Committee carefully weighed shareholder feedback, consensus forecasts and internal modelling of expected performance, as detailed on page 89.

As part of our updated strategic planning post the integration of Peacock Foods, we completed an extensive review of the short and medium term plans with management to consider the alignment of the incentive structure with the strategic goals of the business.

From that exercise, we continue to believe that EPS and ROIC remain the key metrics for our business and long-term strategy. The combination of EPS, reflecting our growth objective, and ROIC, promoting capital discipline and a focus on returns, is consistent with our strategy to deliver sustainable growth in value for our shareholders.

Subsequent to the detailed review and shareholder feedback, the Committee believes that the FY18 targets are at least as challenging as the range that previously applied. For maximum vesting levels, truly exceptional performance under each of the financial measures is required.

I want to thank our shareholders for the time they have committed to consider and discuss our approach and especially for their valuable input so we can better align our remuneration approach and our key proposals for FY18 with their interests.