CLP Holdings Limited – Annual report – 31 December 2025

Industry: utility

Financial Risk Management (extract)

Credit risk

The Group’s approach to managing credit risk for trade receivables is discussed in Note 19.

On the treasury side, all finance-related hedging transactions and bank deposits of the Group entities are executed with counterparties with good credit quality in conformance to the Group treasury policies to minimise credit exposure. Good credit ratings from reputable credit rating agencies and scrutiny of the financial position of non-rated counterparties are two important criteria in the selection of counterparties. The credit quality of counterparties will be closely monitored over the life of the transaction. The Group further assigns mark-to-market limits to its financial counterparties to reduce credit risk concentrations relative to the underlying size and credit strength of each counterparty. The Group also monitors potential exposures to each financial institution counterparty. All derivatives transactions are entered into at the sole credit of the respective subsidiaries, joint ventures and associates without recourse to the Company.

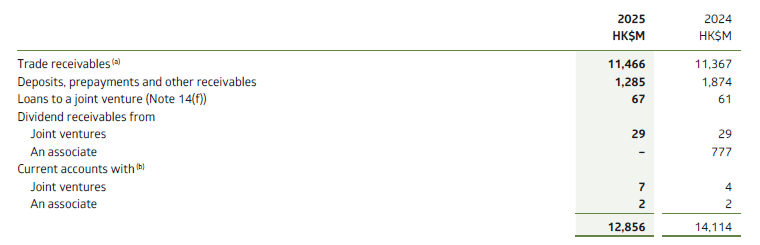

19. Trade and Other Receivables

Accounting Policy

Trade and other receivables are recognised initially at transaction price and are subsequently stated at amortised cost using the effective interest method, less allowances for expected credit losses. The Group measures the loss allowance for its trade receivables at an amount equal to the lifetime expected credit losses. The amount of expected credit losses (or reversal) that is required to adjust the loss allowance at the reporting date to its recognised amount, is recognised in profit or loss, as an impairment loss or a reversal of an impairment loss. Trade and other receivables are written off (either partially or in full) when there is no reasonable expectation of recovery.

Expected credit losses are a probability-weighted estimate of credit losses (i.e. the present value of all cash shortfalls) over the expected life of the trade receivables. Expected credit losses on trade receivables are calculated by using the provision matrix approach. Trade receivables are categorised by common risk characteristics that are representative of the customers’ abilities to pay all amounts due in accordance with the contractual terms. The provision matrix is determined based on historical observed default rates over the expected life of the trade receivables and is adjusted for forward-looking estimates. At every reporting date the historical observed default rates are updated and changes in the forward-looking estimates are analysed.

If there is no significant increase in credit risk since initial recognition, impairment on other receivables is measured at 12-month expected credit losses. If a significant increase in credit risk has occurred, then impairment is measured as lifetime expected credit losses.

Critical Accounting Estimates and Judgements: Recoverability of Trade Receivables

Provision for expected credit losses is made when the Group does not expect to collect all amounts due. The provision is determined by grouping together trade debtors with similar risk characteristics and collectively or individually assessing them for likelihood of recovery. The provision reflects lifetime expected credit losses i.e. possible default events over the expected life of the trade receivables, weighted by the probability of that default occurring. Judgement has been applied in determining the level of provision for expected credit losses, taking into account the credit risk characteristics of customers and the likelihood of recovery assessed on a combination of collective and individual basis as relevant. While the provision is considered appropriate, changes in estimation basis or in economic conditions could lead to a change in the level of provision recorded and consequently on the charge or credit to profit or loss.

Notes:

(a) Trade receivables

The ageing analysis of the trade receivables at 31 December based on invoice date is as follows:

* Including unbilled revenue

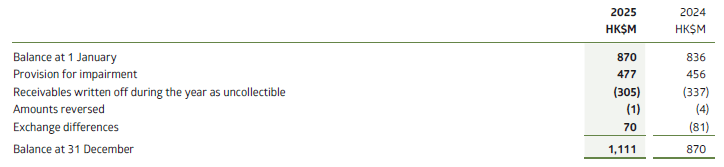

Movements in provision for impairment of trade receivables

Credit risk management

The Group has no significant concentrations of credit risk with respect to the trade receivables in Hong Kong and Australia as their customer bases are widely dispersed in different sectors and industries. The Group has established credit policies for customers in each of its retail businesses.

In Hong Kong, electricity bills are due within two weeks after issuance. To limit the credit risk exposure, the Group has a policy to require cash deposits or bank guarantees from customers for an amount determined from time to time by reference to the usage of the customers, and in the normal course of events will not exceed the highest expected charge for 60 days. For all the deposits held, customers are paid at a floating market interest rate equivalent to the HSBC bank saving rate. At 31 December 2025, such cash deposits amounted to HK$7,541 million (2024: HK$7,207 million) and the bank guarantees stood at HK$1,008 million (2024: HK$952 million). The customers’ deposits are treated on the statement of financial position as current liabilities on the basis that they are repayable on demand.

In Australia, customers are allowed to settle their electricity bills generally no more than 45 days after issuance, while commercial and industrial customers can range up to 60 days. EnergyAustralia has policies in place to ensure that sales of products and services are made to retail customers (including residential, commercial and industrial customers) with a satisfactory credit profile. For residential customers however, where EnergyAustralia is the designated Financially Responsible Market Participant for electricity customers and / or gas customers, it is obliged to accept the customer, irrespective of their credit worthiness. In these instances, information obtained in relation to the customer’s credit worthiness is utilised for the purposes of risk segmentation and prioritisation of collection strategies to mitigate risk. Collectability is reviewed on an ongoing basis.

Trade receivables arising from sales of electricity to the offtakers on the Chinese Mainland, which are mainly state-owned enterprises, are due for settlement within 30 to 90 days after bills issuance. Management has closely monitored the credit qualities and the collectability of these trade receivables.

Expected credit losses

For trade receivables relating to accounts which are long overdue with significant amounts or known insolvencies or non-response to collection activities, they are assessed individually for impairment allowance. CLP Power and EnergyAustralia determine the provision for expected credit losses by grouping together trade receivables with similar credit risk characteristics and collectively assessing them for likelihood of recovery, taking into account prevailing economic conditions and forward looking assumptions.

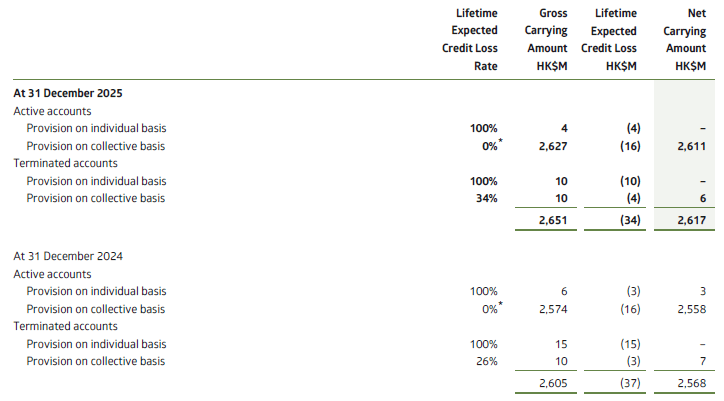

CLP Power

CLP Power classifies its trade receivables by nature of customer accounts. These include active accounts and terminated accounts.

* Expected credit loss rate is close to zero as these trade receivables are mostly secured by cash deposits or bank guarantees from customers and have no recent history of default.

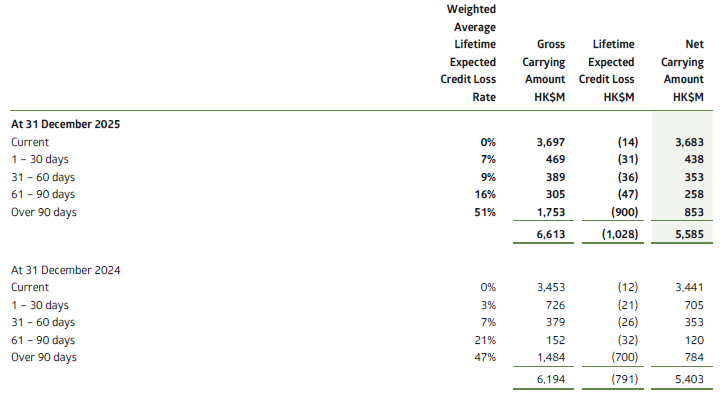

EnergyAustralia

EnergyAustralia categorises its trade receivables based on their ageing. EnergyAustralia recognises lifetime expected credit losses for receivables by assessing future cash flows for each group of trade receivables including a probability weighted amount determined by evaluating a range of possible outcomes based on twelve month rolling historical credit loss experience by customer segment, geographical region, tenure and type of customer and applying that weighting to the receivables held at reporting date.

Chinese Mainland

At 31 December 2025, the Group had total receivables of HK$2,517 million (2024: HK$2,716 million) relating to unpaid Renewable National Subsidies. The application, approval and settlement of the Renewable National Subsidy are governed by the relevant policies issued by the Central People’s Government. All of the relevant wind and solar projects are qualifiable for renewable energy subsidy in accordance with the prevailing government policies. Out of the 16 projects with unpaid Renewable National Subsidies, 5 of them are in the process of applying for approval. Management does not anticipate any foreseeable obstacles that would prevent approval by the relevant government authorities. Under normal operating cycle, it takes a relatively long time for settlement as the collection is subject to the allocation of funds by relevant government authorities to local grid companies and there is no due date for the settlement of Renewable National Subsidies. The expected credit loss is close to zero as continuous settlements have been noted with no history of default and the subsidy is funded by the Renewable Energy Development Fund set up and administered by the Ministry of Finance.

(b) The current accounts with joint ventures and an associate are unsecured, interest free and have no fixed repayment terms.