BP p.l.c. – Annual report – 31 December 2025

Industry: oil and gas

29. Financial instruments and financial risk factors (extract)

(c) Liquidity risk (extract)

Liquidity risk is the risk that suitable sources of funding for the group’s business activities may not be available. The group’s liquidity is managed centrally with operating units forecasting their cash and currency requirements to the central treasury function. Unless restricted by local regulations, generally subsidiaries pool their cash surpluses to the treasury function, which will then arrange to fund other subsidiaries’ requirements, or invest any net surplus in the market or arrange for necessary external borrowings, while managing the group’s overall net currency positions. While there is the potential for concerns about the energy transition to impact banks’ or debt investors’ appetite to finance hydrocarbon activity, we do not anticipate any material change to the group’s funding or liquidity in the short to medium term as a result of such concerns.

The group benefits from open credit provided by suppliers who generally sell on five to 60-day payment terms in accordance with industry norms. bp utilizes various arrangements in order to manage its working capital and reduce volatility in cash flow. This includes discounting receivables and, in the supply and trading businesses, managing inventory, collateral and supplier payment terms within a maximum of 60 days.

It is normal practice in the oil and gas supply and trading business for customers and suppliers to utilize letters of credit (LCs) facilities to mitigate credit and non-performance risk. Consequently, LCs facilitate active trading in a global market where credit and performance risk can be significant. In common with the industry, bp routinely provides LCs to some of its suppliers.

The group has committed LC facilities totalling $10,350 million (2024 $12,130 million), allowing LCs to be issued for a maximum 24-month duration. The facilities are held with 17 international banks.

In certain circumstances, the supplier has the option to request accelerated payment from the LC provider in order to further reduce their exposure. bp’s payments are made to the provider of the LC rather than the supplier according to the original contractual payment terms. At 31 December 2025, a portion of the group’s trade payables which were subject to the LC arrangements were payable to LC providers, with no material exposure to any individual provider. If these facilities were not available, this could result in renegotiation of payment terms with suppliers such that payment terms were shorter.

The group sometimes uses promissory notes to pay its suppliers and other counterparties. This is primarily done to facilitate the counterparty accelerating its cash inflow without also accelerating the group’s related cash outflow. For instance, if a supplier to the group’s supply, trading and shipping business would like prepayment or early-payment for a supply of goods, the group may issue a promissory note (payable at a future date) in favour of that supplier on the supplier’s desired cash inflow date, which that supplier can then convert to cash by selling it to a finance provider on the same-day. The majority of promissory notes the group issues accrue interest on the principal amount of the note at a fixed rate stated on the note from issuance to maturity. This is done to give the supplier or other counterparty certainty about the amount they will receive when they sell the note. It also gives the group flexibility to select the maturity date of the note without that impacting the net present value of the note on its issuance date. The maturity date the group selects for any promissory note that is for the purchase of goods by its supply and trading business will be no more than 60 days after the group takes (or expects to take) title to those goods.

A portion of the group’s trade payables form part of a reverse factoring arrangement with select suppliers.

Suppliers’ participation in the reverse factoring arrangement is voluntary. Suppliers that participate have the option to receive early payment on invoices from the group’s external finance provider. If suppliers choose to receive early payment, they pay a fee to the finance provider. If they opt not to receive early payment, they will pay no fee to the finance provider and will be paid the full invoice amount on the invoice due date. The group provides data about invoices subject to the arrangement directly to the finance provider. This data includes the invoice due date and the maturity date for each invoice. The invoice due date is the date the supplier would have been entitled to receive payment from the group had the invoice not been made subject to the reverse factoring arrangement. The maturity date, which is the date the group will settle that invoice by paying the finance provider, will, in some cases, be the same as the invoice due date. In other cases, it will be a date selected by the group that is no more than 60 days after the group has taken title to the goods to which the invoice relates. If the group selects a maturity date that is after the invoice due date, the group pays the finance provider a fee.

Management does not consider the reverse factoring arrangement to result in excessive concentrations of liquidity risk, in part because the finance provider has the option to (and does) sub-participate portions of the financings to other finance providers. The arrangements have been established for a variety of reasons, including to ease the administrative burden of managing high volumes of invoices from some suppliers, to facilitate some suppliers having the option to accelerate when they receive payment, often at a lower cost than that supplier’s usual cost of borrowing, and, in some cases, to manage the working capital and reduce volatility in cash flow of the group’s supply and trading business. The group has not derecognized the original trade payables relating to the arrangements because the original liability is not substantially modified on entering into the arrangements.

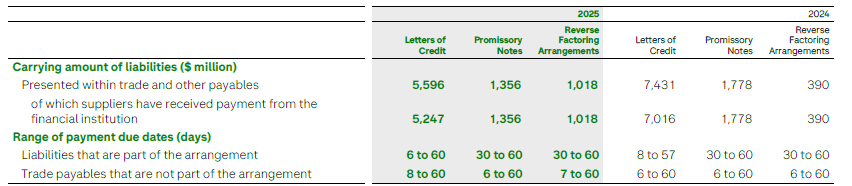

Additional information about the group’s trade payables that are subject to supplier finance arrangements is provided in the table below.

The group does not provide any collateral to the external finance provider.

There were no material business combinations or foreign exchange differences that would affect the liabilities under the supplier finance arrangement in either period.

There were no significant non-cash changes in the carrying amount of financial liabilities subject to the supplier finance arrangements. The payments to the bank are included within operating cash flows because they continue to be part of the normal operating cycle of the group and their principal nature remains operating – i.e., payment for the purchase of goods and services.

If these facilities were not available, this could result in renegotiation of payment terms with suppliers such that settlement periods were shorter.