Fairfax Media limited – Annual report – 25 June 2017

Industry: media

- SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (extract)

(D) CHANGE OF ACCOUNTING POLICY

Through historical business combinations, arising both pre and post the transition to IFRS, the Group has recognised a number of indefinite life assets which include mastheads and radio licenses. In accounting for these transactions, management applied a common accounting policy for the determination of deferred taxes on indefinite life assets considering them to be non-depreciable, and accordingly a related deferred tax liability was not recognised.

On identification of divergent practice arising the matter was taken to IFRS Interpretation Committee (IFRIC). IFRIC acknowledged the diversity in practice and in November 2016 IFRIC issued a final agenda decision clarifying that indefinite life assets are subject to consumption by the entity, it is just that the entity cannot reliably predict the time period over which the asset will be consumed. IFRIC therefore concluded that the assumption of sale could not be presumed in calculating the deferred tax on indefinite life intangibles and the normal principles of AASB 112 needed to be applied.

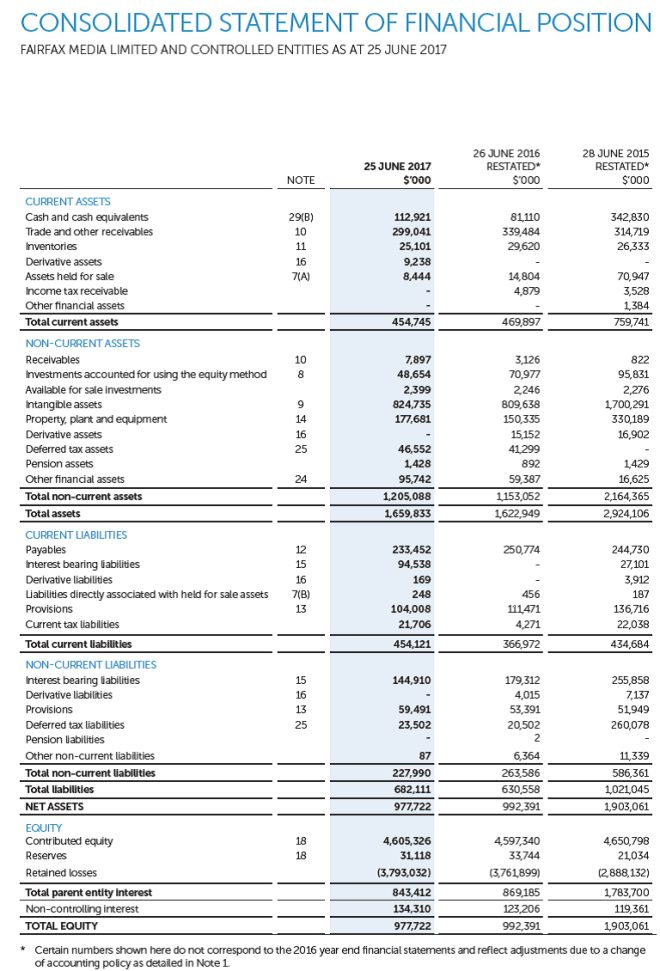

As a consequence of this decision the Company has amended its accounting policy to comply with the revised guidance and have determined that the manner of recovery for the majority of the Group’s indefinite life intangibles is held for use. The impact of the restatement is to as follows:

The accounting policy changes did not have an impact on other comprehensive income or the Group’s operating, investing or financing cashflows.

All other accounting policies are consistent with the previous financial year.