Hunting PLC – Annual report – 31 December 2018

Industry: oil and gas

- Post-Employment Benefits (extract)

(a) UK Pensions

Within the UK, the Group operates a defined contribution (“DC”) plan, which is open to current employees. Contributions to the plan and other Group defined contribution arrangements are charged directly to profit and loss.

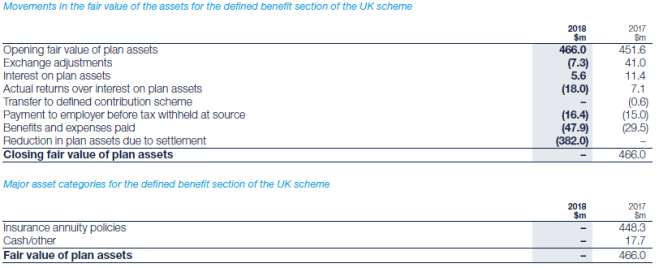

Historically, the Group operated a funded pension scheme, which provided benefits on both a defined benefit (“DB”) and defined contribution (“DC”) basis. That scheme was wound up during the year and, as part of that process, the bulk annuity policies held with insurers to cover members’ DB benefits have been transferred into individual policies for the members.

Payments totalling $16.4m were made from the Scheme on 6 December 2018 as part of the wind-up process, of which $10.6m was paid to the Group and $5.8m was paid to HMRC in relation to tax due. No further payments are due to or from the Scheme.

Risk exposures and investment strategy

At the previous year-end, the assets of the DB section of the scheme were invested in a range of deferred annuity and immediate annuity policies with a range of insurers. These policies matched the benefits to be paid to members of the Scheme. This strategy removed the Group’s investment, inflation and demographic risks relating to the Scheme’s obligations.

As the trustees’ bulk annuity policies held with insurers to cover members’ benefits were transferred into individual policies for the members during 2018, this has removed the Group’s risks relating to an insurer no longer being able to meet its obligations. The Group has no further legal responsibility to fund these benefits.

The Scheme was wound up in December 2018 and the residual assets in the Scheme of $16.4m at the point of termination were transferred to the Group and HMRC. The decrease in the Group’s pension asset seen over 2018 principally reflects these payments.

As the Scheme was wound up during 2018, there are no remaining assets at the year-end.

Amounts recognised in the income statement in respect of the UK scheme

The current service cost includes $2.1m (2017 – $1.5m) of administration costs.

In addition, employer contributions of $7.6m (2017 – $7.1m) for various Group defined contribution arrangements (including the defined contribution section of the UK scheme and UK plan) are recognised in the income statement.

Special events

The following special events occurred during the year:

- The bulk annuity policies held with insurers to cover members’ benefits were transferred to individual members during the year. As a result, these policies are no longer assets of the scheme and the members’ benefits in respect of these policies are no longer liabilities of the scheme.

- As part of the scheme’s wind-up process, members’ Additional Voluntary Contributions (“AVCs”) funds were transferred to other providers. To compensate members with AVCs for potential losses on transfer, $0.3m of the scheme’s surplus funds were used to augment their AVC funds on transfer. This has been recognised as part of the past service cost.

- In addition to this, the Trustee held various historic insurance annuity policies as at 31 December 2017. As part of the process of winding up the scheme, the Trustee has also assigned these policies to individual members with a small augmentation of $0.1m made to these members.

- Payments of $10.6m to the Group and $5.8m to HMRC were made from the scheme on 6 December 2018. This has reduced the surplus of the scheme by the combined total of the payments. There are no remaining assets of the scheme at 31 December 2018.