Capital & Counties Properties PLC – Annual report – 31 December 2022

Industry: real estate

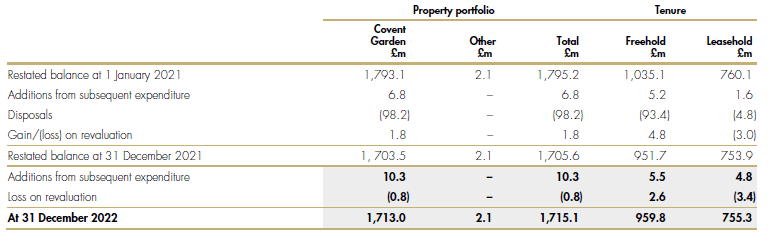

14 Property portfolio

(a) Investment and development property

(b) Market value reconciliation of total property

1. The unrecognised surplus on trading property is shown for informational purposes only and is not a requirement of IFRS. Trading property continues to be measured at the lower of cost and net realisable value in the consolidated financial statements.

The fair value of the Group’s investment, development and trading property at 31 December 2022 was determined by independent, appropriately qualified external valuers, CBRE for the Covent Garden estate and JLL for Lillie Square. The valuations conform to the Royal Institution of Chartered Surveyors (“RICS”) Valuation Professional Standards. Fees paid to valuers are based on fixed price contracts.

Each year the Company appoints the external valuers. The valuers are selected based upon their knowledge, independence and reputation for valuing assets such as those held by the Group.

Valuations are performed bi-annually and are performed consistently across all properties in the Group’s portfolio. At each reporting date appropriately qualified employees of the Group verify all significant inputs and review computational outputs. Valuers submit and present summary reports to the Group’s Audit Committee, with the Executive Directors reporting to the Board on the outcome of each valuation round.

Valuations take into account tenure, lease terms and structural condition. The inputs underlying the valuations include market rent or business profitability, likely incentives offered to tenants, forecast growth rates, yields, discount rates, construction costs including any site specific costs (for example Section 106), professional fees, planning fees, developer’s profit including contingencies, planning and construction timelines, lease re-gear costs, planning risk and sales prices based on known market transactions for similar properties or properties similar to those contemplated for development. As at 31 December 2022 all Covent Garden properties are valued under the income capitalisation technique.

As highlighted within the Group’s Net Zero Carbon Pathway published in December 2021, developments and refurbishments form a key element of the Group’s 2030 Net Zero Carbon Commitment. During the year the Group’s additions from subsequent expenditure was £10.3 million (2021: £6.8 million). This sum included both capital works which enhanced the environmental performance of assets, and design stage work to deliver environmental enhancements. While new ground up development forms a limited part of the Group activity, the design stage on refitting and refurbishment, particularly of heritage buildings, is equally important to deliver Whole Life Carbon efficiency. For further details, refer to the Responsibility section of the Strategic Report on pages 63 to 83.

Valuations are based on what is determined to be the highest and best use. When considering the highest and best use a valuer will consider, on a property by property basis, its actual and potential uses which are physically, legally and financially viable. Where the highest and best use differs from the existing use, the valuer will consider the cost and the likelihood of achieving and implementing this change in arriving at its valuation.

A number of the Group’s properties, held within the Lillie Square joint venture, have been valued on the basis of their development potential. In respect of development valuations, the valuer ordinarily considers the gross development value of the completed scheme based upon assumptions of capital values, rental values and yields of the properties which would be created through the implementation of the development. Deductions are then made for anticipated costs, including an allowance for developer’s profit, before arriving at a valuation.

At 31 December 2022, the Group was contractually committed to £1.7 million (2021: £4.1 million) of future expenditure for the purchase, construction, development and enhancement of investment, development and trading property. Refer to note 27 ‘Capital commitments’ for further information on capital commitments.

Non-financial assets carried at fair value, as is the case for investment and development property held by the Group, are required to be analysed by level depending on the valuation method adopted under IFRS 13 ‘Fair Value Measurement’ (“IFRS 13”). Trading property is exempt from IFRS 13 disclosure requirements.

The different valuation levels are defined as:

Level 1: valuation based on quoted market prices traded in active markets;

Level 2: valuation based on inputs other than quoted prices included within Level 1 that maximise the use of observable data either directly or from market prices or indirectly derived from market prices; and

Level 3: where one or more inputs to valuation are not based on observable market data. Valuations at this level are more subjective and therefore more closely managed, including sensitivity analysis of inputs to valuation models.

When the degree of subjectivity or nature of the measurement inputs changes, consideration is given as to whether a transfer between fair value levels is deemed to have occurred. Unobservable data becoming observable market data would determine a transfer from Level 3 to Level 2. All investment and development properties held by the Group are classified as Level 3 in the current and prior year.

The following table sets out the valuation techniques used in the determination of market value of investment and development property on a property by property basis, as well as the key unobservable inputs used in the valuation models.

1. Estimated rental value and capital value are expressed per square foot on a net internal area basis.

Sensitivity to changes in key assumptions

Covent Garden properties are valued under the income capitalisation method and if all other factors remained equal, an increase in estimated rental value of five per cent would result in an increased asset valuation of £73.0 million (2021: £71.9 million). A decrease in the estimated rental value of five per cent would result in a decreased asset value of £71.7 million (2021: £71.0 million). Conversely, an increased equivalent yield of 25 basis points would result in a decreased asset valuation of £102.2 million (2021: £105.2 million). A decreased equivalent yield of 25 basis points would result in an increased asset valuation of £115.3 million (2021: £119.8 million).

For Other properties valued under the income capitalisation method and if all other factors remained equal, an increase in estimated rental value of five per cent would result in an increased asset valuation of £0.1 million (2021: £0.1 million). A decrease in the estimated rental value of five per cent would result in a decreased asset value of £0.1 million (2021: £0.1 million). Conversely, an increased equivalent yield of 25 basis points would result in a decreased asset valuation of £0.2 million (2021: £0.2 million). A decreased equivalent yield of 25 basis points would result in an increased asset valuation of £0.2 million (2021: £0.2 million).

These key unobservable inputs are interdependent, partially determined by market conditions. All other factors being equal, a higher equivalent yield would lead to a decrease in the valuation, and an increase in estimated rental value would increase the capital value, and vice versa. However, there are interrelationships between the key unobservable inputs which are partially determined by market conditions, which would impact these changes.

27 Capital commitments

At 31 December 2022, the Group was contractually committed to £1.7 million (31 December 2021: £4.1 million) of future expenditure for the purchase, construction, development and enhancement of investment, development and trading property. The full amount is committed 2022 expenditure.

The Group’s share of joint venture capital commitments arising on LSJV amounts to £0.8 million (2021: £1.3 million).