3i Group plc – Annual report – 31 March 2026

Industry: investments

11 Investments in investment entity subsidiaries

Accounting policy:

Investments in investment entity subsidiaries are accounted for as financial instruments at fair value through profit and loss in accordance with IFRS 9.

These entities are typically limited partnerships and other intermediate investment holding structures which hold the Group’s interests in investments in portfolio companies. The fair value can increase or decrease from either amounts paid to or received from the investment entity subsidiaries or valuation movements in line with the Group’s valuation policy.

Substantially all of these entities meet the definition of a Fund under the IPEV guidelines and the fair value of these entities is their net asset value.

We consider the net asset value of investment entity subsidiaries to be the most appropriate to determine fair value. At each reporting period, we consider whether any additional fair value adjustments need to be made to the net asset value of the investment entity subsidiaries. These adjustments may be required to reflect market participants’ considerations about fair value that may include, but are not limited to, liquidity and the portfolio effect of holding multiple investments within the investment entity subsidiary. There was no particular circumstance to indicate that a fair value adjustment was required (31 March 2025: no adjustment required) and, after due consideration, we concluded that the net asset values were the most appropriate reflection of fair value at 31 March 2026. Transfer of portfolio investments from investment entity subsidiaries includes the transfer of investment portfolio between investment entity subsidiaries and the Company at fair value. The consideration for these transfers can either be cash or intra-group receivables.

Level 3 fair value reconciliation – investments in investment entity subsidiaries

There were no transfers of portfolio investments from investment entity subsidiaries during the year, during the year to 31 March 2025, the Company received a transfer of portfolio investments of £1,371 million from partnerships which are classified as investment entity subsidiaries, all of which related to Action. During the year to 31 March 2026, the Company transferred investment portfolio of £304 million (31 March 2025: £730 million) to partnerships which are classified as investment entity subsidiaries of which £304 million (31 March 2025: £593 million) related to Action. Transfer of assets to investment entity subsidiaries for the year to 31 March 2026 includes the £1,739 million non-cash consideration of shares issued to partnerships which are classified as investment entity subsidiaries which related to Action. See Note 17 for details.

Restrictions

3i Group plc, the ultimate parent company, receives dividend income from its subsidiaries. There is £18 million (31 March 2025: none) of restricted held in investment entity subsidiaries relating to carried interest and performance fees payable.

Support

3i Group plc continues to provide, where necessary, ongoing support to its investment entity subsidiaries for the purchase of portfolio investments. The Group’s current commitments are disclosed in Note 20.

20 Commitments

Accounting policy:

Commitments represent amounts the Group has contractually committed to pay third parties but do not yet represent a charge or asset. This gives an indication of committed future cash flows. Commitments are recognised in the balance sheet at the point of settlement subject to associated risks and rewards being transferred. Commitments at the year-end do not impact the Group’s financial results for the year.

At 31 March 2026, the Group and the Company had unquoted investment commitments of £6 million (31 March 2025: £7 million). All outstanding commitments at 31 March 2026 and 31 March 2025 were due within one year.

At 31 March 2026, the Group also had a commitment of £51 million (31 March 2025: £57 million) into partnerships which are classified as investment entity subsidiaries. All outstanding commitments at 31 March 2026 and 31 March 2025 were due within two and five years.

The amounts shown above include £57 million of commitments made by the Group and Company, to invest into funds (31 March 2025: £64 million). The Group and Company were contractually committed to these investments as at 31 March 2026.

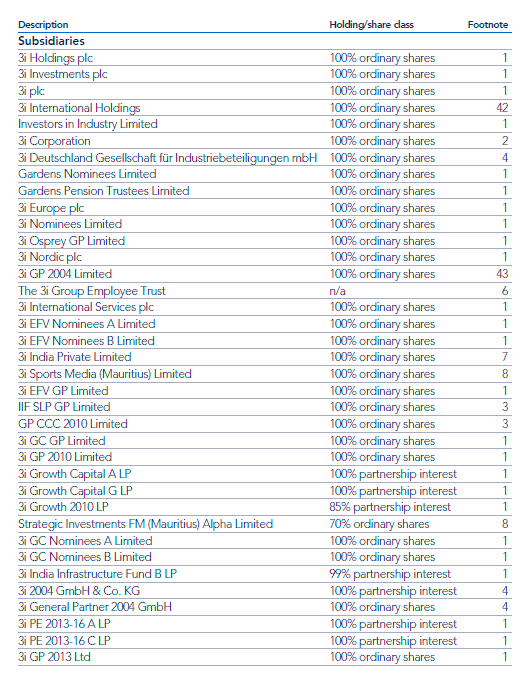

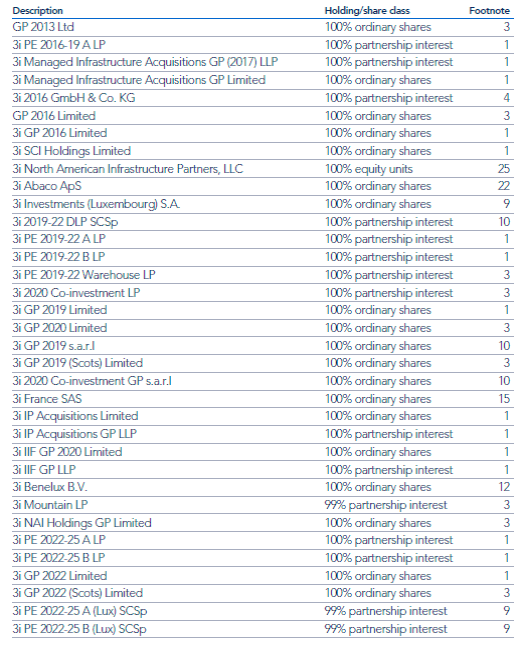

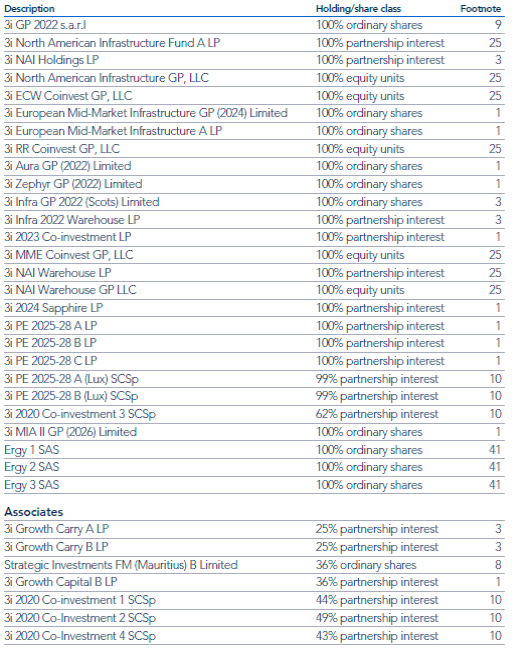

27 Subsidiaries and related undertakings

IFRS 10 deems control, as opposed to equity ownership, as the key factor when determining what meets the definition of a subsidiary. If a group is exposed to, or has rights to, variable returns from its involvement with the investee, then under IFRS 10 it has control. This is inconsistent with the UK’s Companies Act 2006, where voting rights being greater than 50% is the key factor when identifying subsidiaries.

Under IFRS 10, 35 of the Group’s portfolio company investments are considered to be accounting subsidiaries. As the Group applies the investment entity exception available under IFRS 10, these investee companies are classified as investment entity subsidiaries.

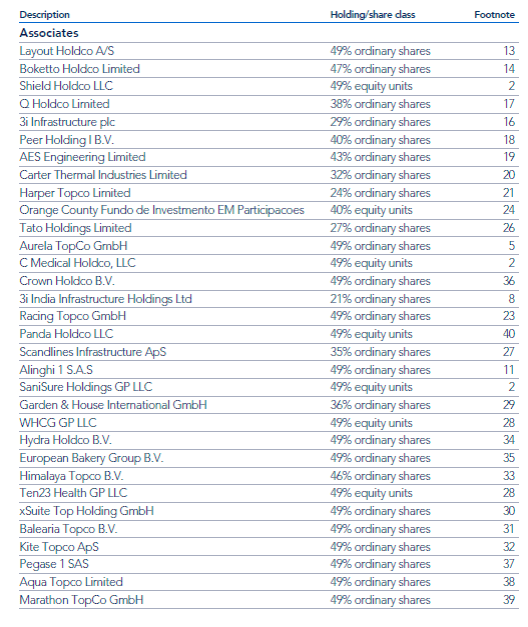

The Companies Act 2006 requires disclosure of certain information about the Group’s related undertakings. Related undertakings are subsidiaries, joint ventures, associates and other significant holdings. In this context, significant means either a shareholding greater than or equal to 20% of the nominal value of any class of shares or a book value greater than 20% of the Group’s assets.

The Company’s related undertakings at 31 March 2026 are listed as follows:

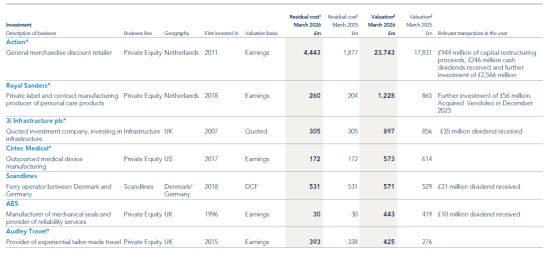

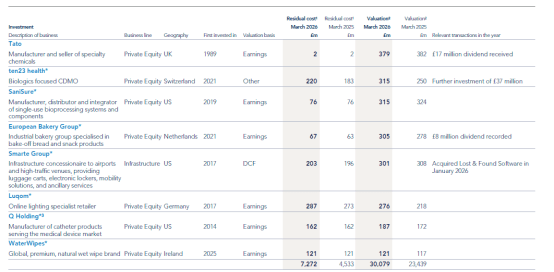

There are no joint ventures or other significant holdings. The 15 large portfolio companies by fair value are detailed on pages 232 and 233. The combination of the table above and that on pages 232 and 233 is deemed by the Directors to fulfil the requirements under IFRS 12 on the disclosure of material subsidiaries.

Portfolio and other information (extract)

The 15 investments listed below account for 95% of the portfolio at 31 March 2026 (31 March 2025: 93%). One portfolio company has been excluded due to commercial sensitivity. All investments have been assessed to establish whether they classify as accounting subsidiaries under IFRS and/or subsidiaries under the UK Companies Act. This assessment forms the basis of our disclosure of accounting subsidiaries in the financial statements.

The UK Companies Act defines a subsidiary based on voting rights, with a greater than 50% majority of voting rights resulting in an entity being classified as a subsidiary. IFRS 10 applies a wider test and, if a Group is exposed, or has rights to variable returns from its involvement with the investee and has the ability to affect these returns through its power over the investee then it has control, and hence the investee is deemed an accounting subsidiary. Controlled subsidiaries under IFRS are noted below. None of these investments are UK Companies Act subsidiaries.

In accordance with Part 5 of The Alternative Investment Fund Managers Regulations 2013 (“the Regulations”), 3i Investments plc, as AIFM, requires all controlled portfolio companies, with their registered offices in the United Kingdom, to make available to employees an annual report which meets the disclosure requirements of the Regulations. These are available either on the portfolio company’s website or through filing with the relevant local authorities.

* Controlled in accordance with IFRS.

1 Residual cost includes cash investment, non-cash investment and interest, net of cost disposed.

2 Valuation represents our unrealised value at the relevant date and does not include any realised proceeds or dividends received under our ownership.

3 The capital proceeds received in FY2023 from the partial disposal of the investment did not result in a reduction to the cost base.