Sasol Limited – Annual report – 30 June 2020

Industry: oil and gas

Sasol’s share price decreased by 62% over the financial year to a closing price on 30 June 2020 of R132,20. This together with the volatility in the share price has resulted in a R205 million credit being recognised in the current year.

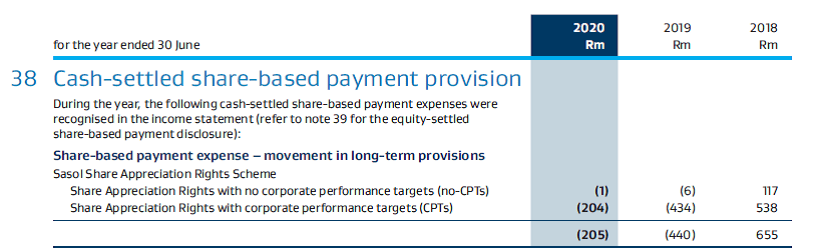

Sasol Share Appreciation Rights Scheme (closed since 2013)

The Share Appreciation Rights scheme (SARs) allows eligible senior employees to earn a long-term incentive amount calculated with reference to the increase in the Sasol Limited share price between the offer date of the SARs to the exercise of such vested rights. No shares are issued in terms of this scheme, all rights have vested and all amounts payable in terms of the scheme are settled in cash.

The offer price of these appreciation rights equals the closing market price of the underlying shares on the trading day immediately preceding the granting of the right. The fair value of the cash-settled liability is calculated at each reporting date. On resignation SARs may be exercised at the employee’s election before their last day of service. On death, the deceased’s estate has a period of 12 months to exercise these rights. On retrenchment or retirement, the employee has a period of 12 months to exercise these rights.

It is group policy that employees should not deal in Sasol Limited securities (and this is extended to the Sasol SARs) for the periods from 1 January for half year-end and 1 July for year-end until two days after publication of the results and at any other time during which they have access to price sensitive information.

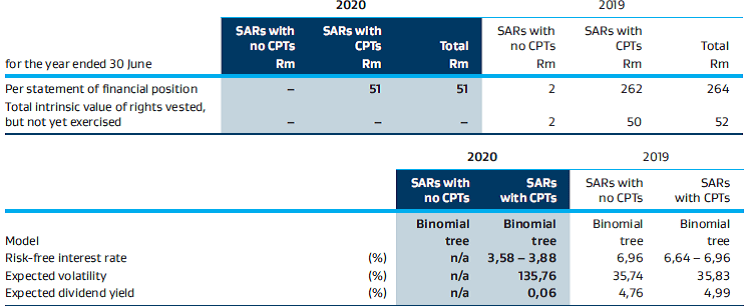

The risk-free rate for periods within the contractual term of the rights is based on the Rand swap curve in effect at the time of the valuation of the grant.

The expected volatility in the value of the rights granted is determined using the historical volatility of the Sasol share price.

The expected dividend yield of the rights granted is determined using expected dividend payments of the Sasol ordinary shares.

The valuation of the share-based payment expense requires a significant degree of judgement to be applied by management.

Accounting policies:

The cash-settled schemes allow certain senior employees the right to participate in the performance of the Sasol Limited share price, in return for services rendered, through the payment of cash incentives which are based on the market price of the Sasol Limited share. All the rights have vested with a liability recognised at fair value, at each reporting date, in the statement of financial position until the date of settlement.

Areas of judgement:

Fair value is measured using the Binomial tree option pricing models where applicable. The expected life used in the models has been adjusted, based on management’s best estimate, for the effects of non-transferability, exercise restrictions and behavioural considerations such as volatility, dividend yield and maturity of the award.