San Miguel Corporation – Annual report – 31 December 2025

Industry: conglomerate

3. Material Accounting Policy Information

Investment Property

Investment property consists of property held to earn rentals and/or for capital appreciation but not for sale in the ordinary course of business, used in the production or supply of goods or services or for administrative purposes. Investment property, except for land, is measured at cost including transaction costs less accumulated depreciation and any accumulated impairment in value. The carrying amount includes the cost of replacing part of an existing investment property at the time the cost is incurred, if the recognition criteria are met, and excludes the costs of day-to-day servicing of an investment property. Land is stated at cost less any impairment in value.

Depreciation, which commence when the assets are available for their intended use, are computed using the straight-line method over the following estimated useful lives of the assets:

The useful lives, residual values and depreciation method are reviewed and adjusted, if appropriate, at each reporting date.

Investment property is derecognized either when it has been disposed of or when it is permanently withdrawn from use and no future economic benefit is expected from its disposal. Any gains and losses on the retirement and disposal of investment property are recognized in the consolidated statements of income in the period of retirement and disposal.

Transfers are made to investment property when, and only when, there is an actual change in use, evidenced by ending of owner-occupation or commencement of an operating lease to another party. Transfers are made from investment property when, and only when, there is an actual change in use, evidenced by commencement of the owner-occupation or commencement of development with a view to sell.

For a transfer from investment property to owner-occupied property or inventories, the cost of property for subsequent accounting is its carrying amount at the date of change in use. If the property occupied by the Group as an owner-occupied property becomes an investment property, the Group accounts for such property in accordance with the policy stated under property, plant and equipment up to the date of change in use.

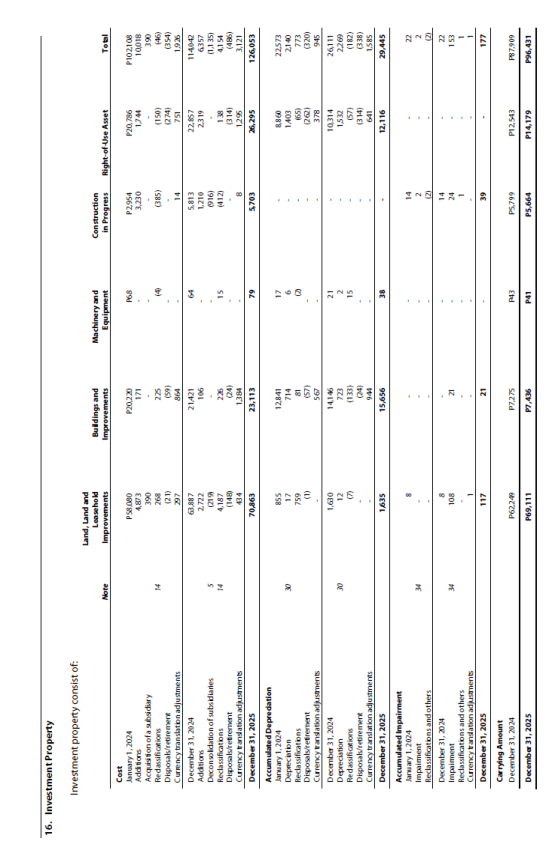

Total depreciation recognized in the consolidated statements of income amounted to P2,269, P2,140 and P2,046 in 2025, 2024 and 2023, respectively (Note 30).

The reclassification relates to the change in usage as evidenced by ending of owner-occupation or commencement of operating lease to another party which was reclassified from “Property, plant and equipment – net” account mainly by SMPI and Multi-Ventures Investment Holdings, Inc. (Note 14).

Additions in investment property in 2024 include land recognized by Petron arising from the reversal of the reconveyance of land declared as property dividends in 1993 amounting to P33 (Notes 14 and 45).

Impairment loss of P153, P2 and P14 was recognized in 2025, 2024 and 2023, respectively (Note 34).

There are no other direct selling and administrative expenses other than depreciation and real property taxes arising from investment property that generated income in 2025, 2024 and 2023.

The fair value of investment property amounting to P214,939 and P187,191 as at December 31, 2025 and 2024, respectively, has been categorized as Level 3 in the fair value hierarchy based on the inputs used in the valuation techniques (Note 4).

The fair value of investment property was determined by external, independent property appraisers having appropriate recognized professional qualifications and recent experience in the location and category of the property being valued. The independent appraisers provide the fair value of the Group’s investment property on a regular basis.

Valuation Technique and Significant Unobservable Inputs

The valuation of investment property applied the following approaches:

Cost Approach. This approach is based on the principle of substitution, which holds that an informed buyer would not pay more for a given property than the cost of an equally desirable alternative. The methodology of this approach is a set of procedures that estimate the current reproduction cost of the improvements, deducts accrued depreciation from all sources, and adds the value of investment property.

Sales Comparison Approach. The market value was determined using the Sales Comparison Approach. The comparative approach considers the sale of similar or substitute property, registered within the vicinity, and the related market data. The estimated value is established by process involving comparison. The property being valued is then compared with sales of similar property that have been transacted in the market. Listings and offerings may also be considered. The observable inputs to determine the market value of the property are the following: location characteristics; size; time element; quality and prospective use; bargaining allowance and marketability.

Income Approach. The rental value of the subject property was determined using the Income Approach. Under the Income Approach, the market value of the property is determined first, and then the proper capitalization rate is applied to arrive at its rental value. The rental value of the property is determined based on what a prudent lessor or a prospective lessee are willing to pay for its use and occupancy considering the prevailing rental rates of similar property and/or rate of return a prudent lessor generally expects on the return on its investment. A study of current market conditions indicates that the return on capital for similar real estate investment ranges from 2% to 7%.