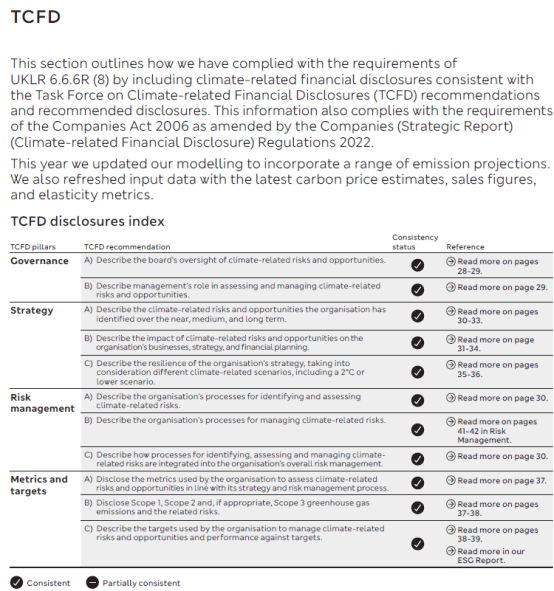

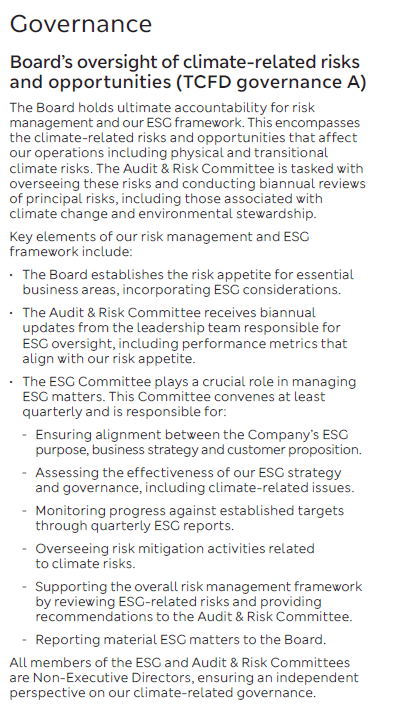

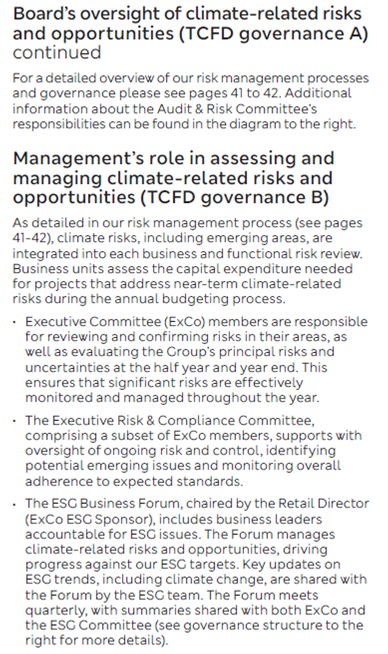

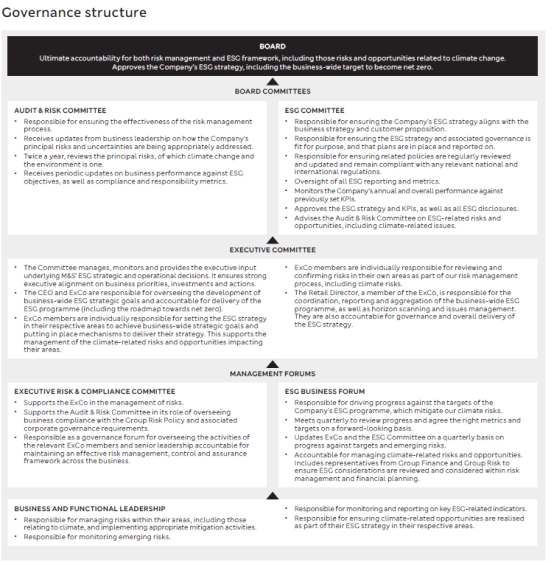

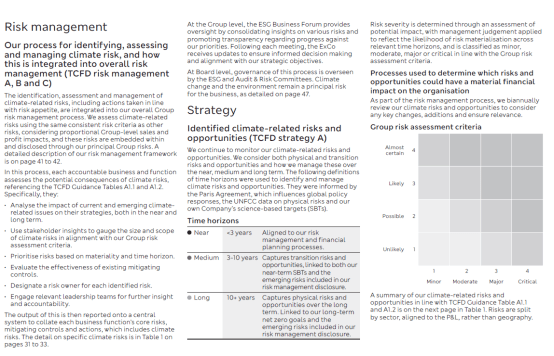

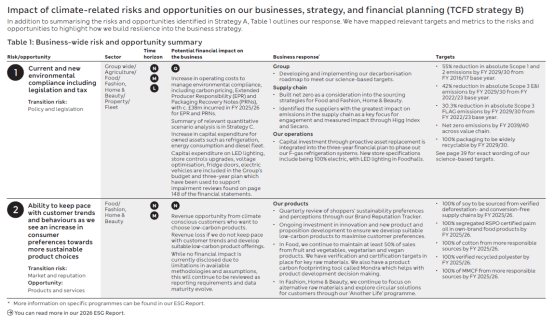

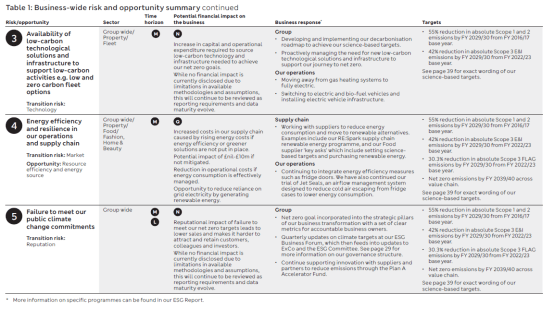

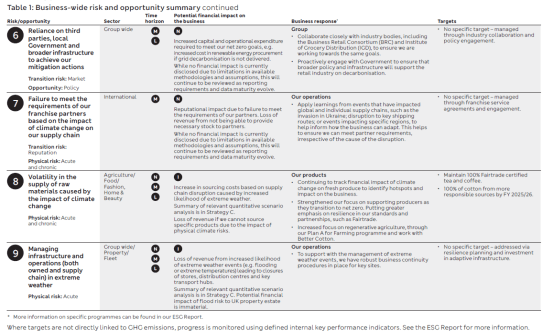

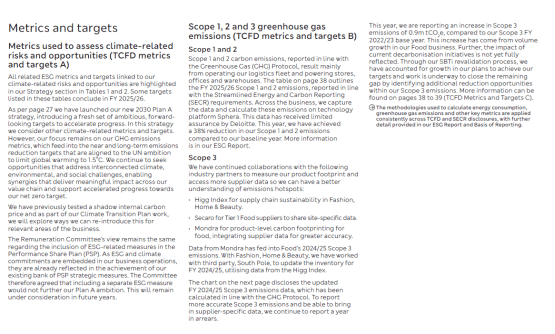

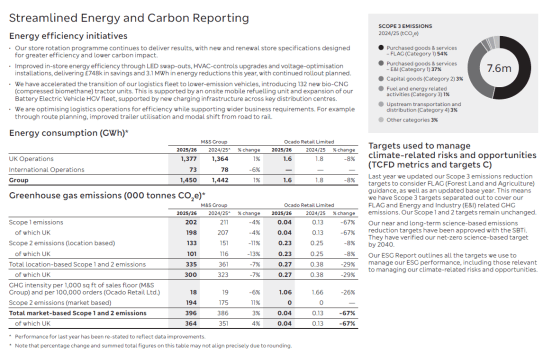

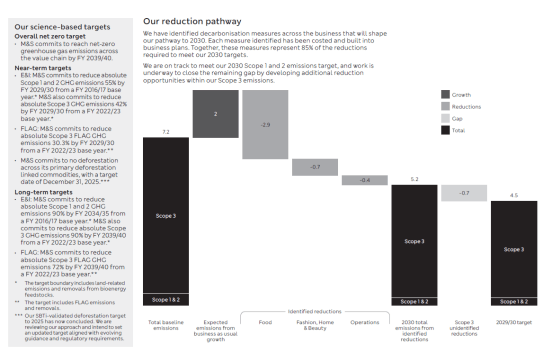

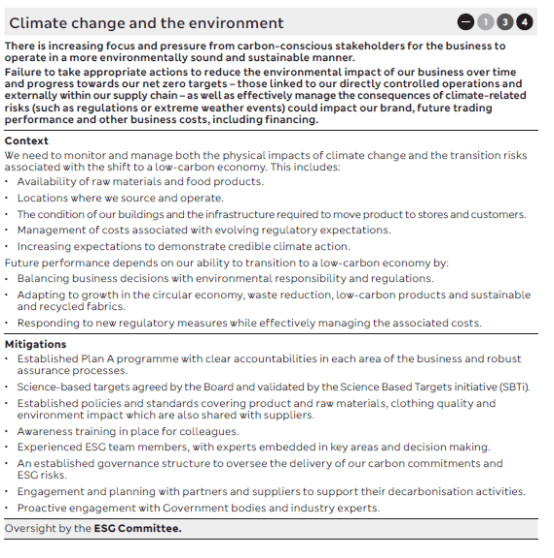

Climate change, TCFD disclosures, LR 6.6.6R, SECR, Companies Act requirements, principal risks Marks and Spencer Group plc – Annual report – 28 March 2026 Industry: retail PRINCIPAL RISKS AND UNCERTAINTIES (extract) Share this: Share on X (Opens in new window) X Share on Facebook (Opens in new window) Facebook Like Loading...