Barratt Redrow plc – Annual report – 29 June 2025

Industry: real estate

1. Basis of preparation (extract)

Critical accounting judgements and key sources of estimation uncertainty

The preparation of Financial Statements in conformity with UK adopted IFRS requires the use of estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the Financial Statements and the reported amounts of revenues and expenses during the reporting period. Although these estimates are based on the Directors’ best knowledge of the amounts, actual results may ultimately differ from those estimates. The Directors have made no individual critical accounting judgements that have had a significant impact upon the Financial Statements, apart from those involving estimations.

The most significant estimates made by the Directors in these Financial Statements, which are the key sources of estimation uncertainty that may have a significant risk of causing a material difference to the carrying value of assets and liabilities within the next financial period, are the valuation of legacy property provisions (see note 20) and margin recognition (see note 3).

There are no key sources of estimation uncertainty in the Company Financial Statements.

20. Provisions

Provisions

Provisions are recognised when the Group has a present obligation (legal or constructive) as a result of a past event, and it is probable that the Group will be required to settle that obligation. Provisions are measured at the Directors’ best estimate of the expenditure required to settle the obligation at the balance sheet date and are discounted to present value where the effect is material.

The Company had no provisions in either year.

Costs in relation to completed developments

Following the legal completion and handover to customers of all units on a site, the Group may retain obligations which are not settled for a number of years. These include costs in relation to the adoption of roads or public open space by local authorities, other contractual obligations to third parties and, in certain cases, the costs of remedial works where defects have been identified.

Whilst a proportion of this cost will not be realised within 12 months, the Group has an obligation to complete the works immediately should it be requested to do so. The balance in total is therefore considered to be current in nature. All outstanding issues on completed developments are resolved as soon as is practicable.

Legacy property provisions

Building safety

On 13 March 2023, the Group signed the Self-Remediation Terms and Contract, codifying the commitments previously made under the Building Safety Pledge to undertake, or to fund, remediation or mitigation works on external wall systems (EWS) on all buildings of 11 metres or above in England and Wales that it has developed or refurbished in the 30 years preceding the date of the Building Safety Pledge, and to reimburse the Government’s Building Safety Fund wherever it has contributed to such activities. The Group has provided for the cost of fulfilling this commitment, as well as assisting with remedial work identified at a limited number of other legacy properties where it has a legal liability to do so, where relevant build issues have been identified, or where it is considered probable that such build issues exist.

As a result of the acquisition of Redrow plc on 21 August 2024, the Group’s obligations under the Self-Remediation Terms and Contract now include the relevant buildings developed or refurbished by the Redrow group of companies. The remediation of these buildings is now being managed with the benefit of the experience of the combined Group and the fair value of the obligations at the acquisition date included within provisions. In accordance with IFRS 3, as described in note 10, this includes the fair value of possible remediation works on properties for which there is currently no confirmation of works being required and which are deemed to be low risk, and consequently, in accordance with IAS 37, no liability was previously recognised in the financial statements of Redrow plc or its subsidiaries.

At the Redrow acquisition date, 27 buildings with a height of over 11 metres were under active review by Redrow under the Self-Remediation Contract. Responsibility for these buildings was assumed by the Group on acquisition. Following contact from building owners regarding potential issues, a net further 18 buildings with a height of over 11 metres were added to the Group scope of works in the period, including one in the Redrow portfolio.

At 29 June 2025, of the 278 buildings in the portfolio under review in the combined Group, 192 were at tender or site mobilisation or were in the process of being remediated (30 June 2024: 262 buildings, of which 137 were at tender or site mobilisation or were in the process of being remediated).

As part of the ongoing works to remediate building safety issues, it has been identified that additional work on four buildings at one development in our Southern region is required to improve the fire protection of the internal structure. Additional costs have also been recognised for the remediation of newly identified issues at a large development in London that was already part of our building safety provision. An additional £93.1m has been provided at the reporting date for these two developments, based on the current estimate of remediation cost.

At 30 June 2024, the Group held £14.8m in relation to completed developments and £18.8m in relation to reinforced concrete frames in respect of the above two developments. All work at these developments is being undertaken under a single remediation programme and therefore all related amounts have been reclassified to be shown together in the building safety provision.

A further £15.8m has been provided in respect of minor cost increases across the rest of the portfolio.

The Group continues to review all of its current and legacy buildings where it has used EWS or cladding solutions, assessing the action required in line with the latest updates to Government guidance as it applies to multi-storey and multi-occupied residential buildings.

All our buildings, including those incorporating EWS or cladding solutions, were signed off by approved inspectors as compliant with the relevant Building Regulations at the time of completion.

Management expect the majority of the works to be completed within four years. Estimated future costs are discounted to their present value using the yield for a UK gilt with maturity approximating the duration of the remediation programme. This is a complex area requiring significant estimates with respect to the estimates for the number of buildings affected, the individual remediation requirements of each building and the costs associated with that remediation (see also note 29).

The investigation of the works required at some of the buildings is at an early stage and work at others is ongoing. Therefore, it is possible that the scope of works required could change. If government legislation and regulation further evolve, or if the estimated timing of work is affected by building owner engagement or contractor availability, these estimates could change.

In relation to the Group’s obligations under the Scottish Safer Buildings Accord, signed on 31 May 2023, and the Housing (Cladding Remediation) (Scotland) Act, passed on 21 June 2024, the external wall provision is recorded on the basis that the standard of remediation required in Scotland is consistent with England and Wales. This will be determined when the final contract with the Scottish Government is signed (see note 29).

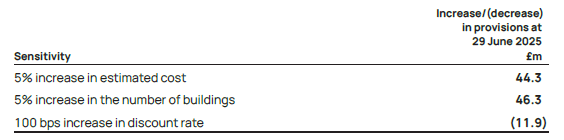

The estimates are based on key assumptions that will be updated as work and time progress. The sensitivity of the provision held at the balance sheet date, to the following possible movements in key assumptions, is shown below:

Reinforced concrete frames

The Group holds a provision for the remediation of reinforced concrete frames on developments designed by two engineering firms whose work has previously been found to be defective.

The engineering firms involved in the above developments have been determined to also have been involved in the design of certain developments constructed by the Redrow group. Initial investigations have identified similar issues to those seen at the legacy Barratt buildings at four Redrow developments. Based on a high-level assessment of the probable cost of remediation, a provision of £105.2m has been included within the liabilities assumed through the acquisition of Redrow.

For all developments where additional amounts have been provided at the reporting date, further analysis must be undertaken to determine both the exact locations within the developments which will need to be remediated and the nature of the work to be performed in each case, which may result in revisions to the estimated costs and time frame of delivery.

Management expect the majority of the works to be completed within three years. Management has made estimates as to the future costs, the extent of the remedial works required and the costs of providing alternative accommodation to any residents affected by the remedial works. These Financial Statements have been prepared based on currently available information, including known costs and quotations where possible. However, the extent, cost and timing of remedial work may change as work progresses.

29. Contingent liabilities

Contingent liabilities related to subsidiaries

The Company has guaranteed certain bank borrowings of its subsidiary undertakings.

Certain subsidiary undertakings have commitments for the purchase of trading stock entered into in the normal course of business.

In the normal course of business, the Group has given counter-indemnities in respect of performance bonds and financial guarantees. At 29 June 2025 the bonds and guarantees amount to £626.8m (2024: £419.9m) and, at the date of approval of these Financial Statements, the possibility of cash outflow is immaterial and no provision is required.

Building safety

As disclosed in note 20, on 13 March 2023, the Group signed the Self-Remediation Terms and Contract, codifying the commitments previously made under the Building Safety Pledge. The Group is currently undertaking a review of all of its current and legacy buildings where it has used EWS or cladding solutions. Approved inspectors signed off all of our buildings, including the EWS or cladding used, as compliant with the relevant building regulations at the time of completion.

At 29 June 2025, the Group held provisions of £886.4m (2024: £628.1m) in relation to building safety, based on management’s best estimate of the cost and timing of remediation of in-scope buildings. It is possible that as remediation work proceeds, additional remedial works will be required which do not relate to EWS or cladding solutions. Such works may not have been identified from the reviews and physical inspections undertaken to date and may only be identified when detailed remediation work is in progress. Therefore, the nature, timing and extent of any such costs were unknown at the balance sheet date.

It is also possible that the number of buildings requiring remediation may increase. This could occur because buildings which hold valid EWS1 certificates are found to require remediation or because investigatory works identify remediation not previously identified.

In addition, we recognise that the retrospective review of building materials and fire safety matters continues to evolve. These Financial Statements have been prepared based on currently available information and regulatory guidance. However, these estimates may be updated if government legislation and regulation further evolve.

On 31 May 2023 the Group signed the Scottish Safer Buildings Accord, committing to resolve life-critical fire safety defects in multi-occupancy residential domestic or part-domestic buildings, over 11 metres in Scotland, built by us as a developer in the period of 30 years to 1 June 2022. This Accord is not legally binding, but we are committed to working in good faith with the Scottish Government to agree a legal form contract. The Group has undertaken preliminary cost assessments at multi-occupancy buildings over 11 metres in Scotland at which fire safety defects have been identified. The Group’s EWS provision at 29 June 2025 reflects the outcome of these assessments, based on the assumption that the standard of remediation required in Scotland is consistent with that in England and Wales. The Housing (Cladding Remediation) (Scotland) Act 2024, which became law on 21 June 2024, has provided a framework on which the remediation programme in Scotland can be based but requires secondary legislation and further contractual agreement with developers to determine the details. The estimated cost may vary depending on the final form of the developer remediation contract agreed with the Scottish Government.

In November 2024, an investigation by the Institution of Fire Engineers concluded that one of its members had failed to maintain professional standards and terminated his membership. The firm at which the individual worked has provided fire risk assessments on a number of buildings which the Group has developed. Impact assessments for affected buildings are ongoing and there has been nothing to suggest that a change to the provision is required at the reporting date.

During the prior year, warranty providers received claims under warranties for building safety matters on three developments historically delivered by the Group. Further investigation is required to determine whether the nature and extent of any remediation work are incremental to that already expected and we expect this process to be completed during FY26.

Reinforced concrete frames

As disclosed in note 20, the Group is undertaking remediation at developments designed by certain engineering firms or associated companies. The Financial Statements have been prepared based on currently available information; however, the detailed review is ongoing and the extent and cost of any remedial work may change as this work progresses.

We are actively seeking to recover costs from third parties in respect of building safety and reinforced concrete frames; however, there is no certainty regarding the extent of any financial recovery.

Contingent liabilities relating to JVs

The Group has given counter-indemnities in respect of performance bonds and financial guarantees to its JVs totalling £11.9m at 29 June 2025 (2024: £5.0m).

The Group has also given a number of performance guarantees in respect of the obligations of its JVs, requiring the Group to complete development agreement contractual obligations in the event that the JVs do not perform as required under the terms of the related contracts. At 29 June 2025, the probability of any loss to the Group resulting from these guarantees is considered to be remote.

Contingent liabilities related to legal claims

Provision is made for the Directors’ best estimates of all known material legal claims and all legal actions in progress. The Group takes legal advice as to the likelihood of success of claims and actions and no provision is made (other than for legal costs) where the Directors consider, based on such advice, that claims or actions are unlikely to succeed, or a sufficiently reliable estimate of the potential obligations cannot be made.