Rolls-Royce Holdings plc – Annual report – 31 December 2025

Industry: aerospace

1 Accounting policies (extract)

Climate change

In preparing the Consolidated Financial Statements the Directors have considered the potential impact of climate change, particularly in the context of the disclosures included in the Strategic Report that set out climate-related commitments, targets and the pillars of the Rolls-Royce energy transition strategy which are:

- optimising our operations, including decarbonising operations, facilities, product testing and business activities. This will be met through a combination of procuring clean energy, reducing overall energy demand, and clean power generation. An estimate of the investment required to meet Scope 1 + 2 emission improvements is included in the forecasts that support these Consolidated Financial Statements;

- enabling our customers, by delivering innovative products and solutions that can accelerate the global energy transition. This includes the development and deployment of a future portfolio that includes the UltraFan engine in Civil Aerospace, Battery Energy Storage Systems in Power Systems and small modular reactors. An estimate of the investment required to deliver these technologies is included in the forecasts that support the Consolidated Financial Statements; and

- engaging and collaborating with customers, suppliers, industry and policymakers supporting the necessary enabling environment to achieve collective energy transition and climate goals.

The climate change scenarios previously prepared to assess the viability of our business strategy, decarbonisation plans and approach to managing climate-related risk have continued to develop over the last year as set out in the Strategic Report. The scenarios are used to help assess the Group’s strategic resilience to climate change and the energy transition. Consideration is made of how each of them impacts: the life of assets; future revenue projections; future profitability; and whether additional costs may occur. There remains inherent uncertainty around how the scenarios will impact the Group. The Directors assess the assumptions on a regular basis to ensure that they are consistent with the risk management activities and the commitments made to investors and other stakeholders.

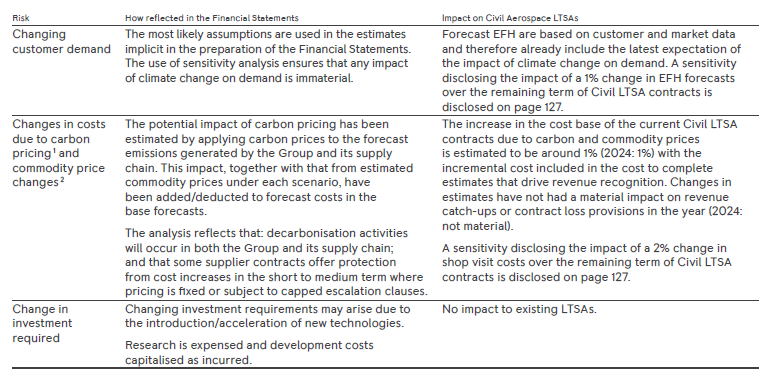

Based on the Taskforce for Climate-related Financial Disclosures (TCFD) recommendations, the Group assesses the potential impact of climate-related risks which cover transition and physical risks and opportunities. The Group has identified four key transition risks (relating to changing customer demand, changes in cost due to carbon pricing, changes in cost due to commodity price changes and change in investment requirements) and three key physical risks (relating to facility disruption, supply chain disruption and impact on product performance) which may arise from the energy transition. The transition risks are the most likely to have an impact on the Consolidated Financial Statements, as exposure to physical risks will be greater in the longer term.

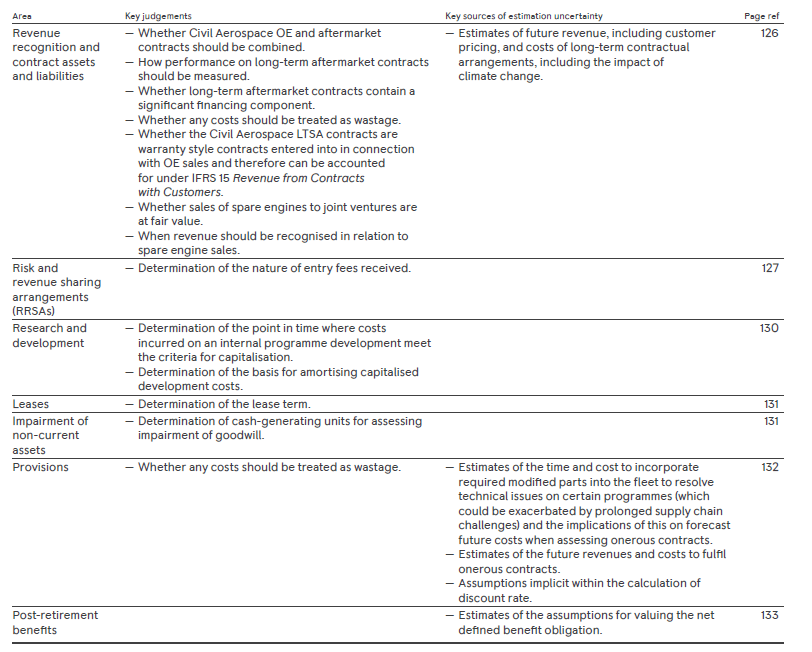

The key sources of estimation uncertainty at the balance sheet date are set out on page 124 and the Directors have considered the impact of climate change on those estimates. The key assumptions used in this assessment are consistent with those used in the climate scenarios presented in the Strategic Review. A summary of the assessment is set out below.

1 Based on the Oxford Economic Global Climate Service and Databank, with rates of $145 per tonne of carbon in 2025 increasing to c. $300 in 2030. Beyond 2030, the Group has considered a range of carbon pricing data sources with an assumed increase (in outturn economics) of c. 2% per annum to c. $475 per tonne by 2050

2 Commodity prices from the Oxford Economics, Global Climate Service and Databank

Items that may be impacted by climate-related risks, but which are not considered to be key areas of judgement or sources of estimation uncertainty in the current financial year are outlined below.

Carrying value of goodwill – The recoverable amount used in impairment testing is based on the cash flow projections of the CGUs to which the goodwill balances relate. The projections include assumptions that are based on past experience and external sources of information in relation to sales volumes, product costs and the required level of investment that could all be impacted by climate change. The climate scenarios prepared do not show a significant deterioration of demand for Civil Aerospace (including Rolls-Royce Deutschland) programmes given that all commercial aero engines are compatible with sustainable fuels, similarly the majority of the portfolio in Power Systems is compatible with alternative and more sustainable fuels. The scenarios reflect the impact of a broad range of potential costs imposed by policy or regulatory interventions (through carbon pricing) and the investment required to ensure new products will be compatible with net zero operation, and to achieve net zero Scope 1 + 2 GHG emission commitments. The scenarios do not indicate the need for an impairment charge and the Directors do not consider that any reasonably possible changes in the climate related assumptions would cause the value in use of the goodwill to fall below its carrying value.

Recoverability of programme intangible assets – The recoverable amount used in impairment testing is based on the cash flow projections of the individual programmes. The projections include assumptions in relation to sales volumes and product costs that could be impacted by climate change. Given the level of headroom in the programme intangible assets, with most engines being compatible with alternative or more sustainable fuels, and with cost estimates including an allowance for the impact of carbon pricing, there is no indication of any potential impairment as a result of climate change.

Useful lives of assets – The useful lives of property, plant and equipment and right-of-use assets could be reduced by climate-related matters, for example, as a result of physical risks, obsolescence or legal restrictions. The change in useful lives would have a direct impact on the amount of depreciation or amortisation recognised each year from the date of reassessment. The Directors’ review of useful lives has taken into consideration the impacts of the Group’s decarbonisation strategy and has not had a material impact on the results for the year. The Directors have also considered the remaining useful economic lives of material intangible assets, including the £1,993m and £814m capitalised development spend associated with the Trent and business aviation programmes disclosed in note 11. Given the measures the Group is taking, including demonstration that all the commercial aero-engines and majority of the portfolio in Power Systems are compatible with alternative and sustainable fuels, the Directors judge that no adjustment is required to the useful economic lives.

Inventory valuation – Climate-related matters may affect the value of inventories as a result of a decline in selling prices or could become obsolete due to a reduction in demand. After consideration of the typical stock-turns of the inventory in relation to the rate of change in the market the Directors consider that inventory is appropriately valued.

Recoverability of trade receivables and contract assets – The impact of climate-related matters could have an impact on the Group’s customers in the future, especially those customers in the Civil Aerospace business. No material climate-related issues have arisen during the year that have impacted the assessment of the recoverability of receivables. The Group’s expected credit loss (ECL) provision uses credit ratings which inherently will include the market’s assessment of the climate change impact on credit risk of the counter parties. Given the maturity time of trade receivables and the majority of contract assets, climate change is unlikely to cause a material increase on counter party credit risk in that time.

Recoverability of deferred tax assets on UK tax losses – Deferred tax assets are recognised to the extent it is probable that future taxable profits will be available against which the assets can be utilised. The deferred tax asset on UK tax losses primarily arises in Rolls-Royce plc and has been recognised based on the expectation that the business will generate taxable profits and tax liabilities in the future against which the losses and deductible temporary differences can be utilised. Recognising the longer term over which these assets will be recovered, the Group considers climate change scenarios that could impact future taxable profits through changes in demand for our products or their cost. The variability in taxable profits that could arise from changes in such estimates is not considered to be of sufficient magnitude that it would impact our judgement that there will be sufficient future taxable profits available against which the assets can be utilised.

Share-based payments – The Group is committed to achieving net zero by 2050. The Group has committed to reduce the total Scope 1 + 2 greenhouse gas emissions from its facilities, operations and testing by 46% by the end of 2030 (against a baseline of 2019). This metric accounts for 10% of the long-term incentive plan for awards granted in 2025, with performance measured against three-year cumulative targets.

Defined benefit pension plans – Having assessed the risks and opportunities of climate change and considered the nature of the assets of the fund, climate change is unlikely to have a material impact on the position in the Consolidated Financial Statements

Going concern – Given the short-term nature of the Group’s going concern assessment, the impact of climate change does not have a significant impact. The Directors have considered the level of liquidity available, and the potential impact of the climate change risks, in making their assessment.

Page 124 (extract)

Key areas of judgement and sources of estimation uncertainty

The determination of the Group’s accounting policies requires judgement. The subsequent application of these policies requires estimates, and the actual outcome may differ from that calculated. The key judgements and key sources of estimation uncertainty at the balance sheet date, that have a significant risk of causing material adjustment to the carrying amounts of assets and liabilities within the next financial year, are summarised below. Further details, together with sensitivities for key sources of estimation uncertainty where appropriate and practicable, are included within the significant accounting policies section of this note.