EVN AG – Annual report – 30 September 2024

Industry: utilities

61. Risk management (extract)

Credit and default risk

Credit and default risk represents the risk of a loss when business partners fail to meet their contractual obligations. This risk is inherent to all agreements with delayed payment terms or fulfilment at a later date. Default risk generally arises in connection with trade receivables and the debt instruments held as financial assets by the Group. The carrying amount of the financial assets and contractual assets represents the maximum default risk.

To limit credit risk, the company evaluates the credit standing of its business partners. Internal and external ratings (including Standard & Poor’s, Moody’s, Fitch and KSV 1870) of the counterparties are used for this purpose, and the business volume is limited in accordance with the rating and the probability of default. Sufficient collateral is required before a transaction is entered into if the partner’s credit rating is inadequate.

EVN monitors credit risk and limits default risk for financial receivables and for derivatives and forward transactions which are concluded to hedge the risks connected with EVN’s energy business or are related to end customers and other debtors.

In order to reduce credit risk, hedging transactions are entered into only with well-known banks that have good credit ratings. EVN also ensures that funds are deposited at banks with the best possible credit standing based on international ratings.

The default risk for customers is monitored separately at EVN and supported primarily by ratings and experience-based values. Default risk is also minimised with efficient receivables management and the continuous monitoring of customer payment behaviour.

The recognition of impairment losses to financial assets carried at amortised cost and to contractual assets in accordance with IFRS 15 has been based on the ECL model for expected credit losses since 1 October 2018.

EVN measures the impairment losses for trade receivables without a significant financing component and for contractual assets at an amount equal to the expected lifetime credit losses. In contrast, the impairment losses

- for financial assets with a low default risk as of the balance sheet date and

- for bank deposits without a significant increase in the default risk since initial recognition are based on the expected 12-month credit loss.

From the viewpoint of the EVN Group, a financial asset has a low default risk when its credit rating meets the “investment grade” definition. The Group sees this condition as met with an internal rating of 4 or higher or with an equivalent rating of BBB– or higher from Standard and Poor‘s (S&P).

EVN uses appropriate and reliable information which is relevant and available without undue expenditure of time and expense to determine whether the default risk of a financial asset has increased significantly since initial recognition and to estimate the expected credit losses. The default risk of a financial asset is assumed to have increased significantly when the related credit rating has declined to 5b on EVN’s internal rating scale, which represents the S&P equivalent of B+.

The EVN Group considers a financial asset to be in default when:

- the debtor is unlikely to meet his/her credit obligations in full without measures by the Group to realise collateral (if available), or

- the financial asset declines to 5c on EVN’s internal rating scale, which represents the S&P equivalent of CCC+, or • payment on trade receivables has not been received after a second reminder or insolvency proceedings are opened over a company or private person.

Default probabilities and collection rates based on the applicable rating category are used to calculate the required impairment loss. The amount of the impairment loss equals the present value of the expected credit loss.

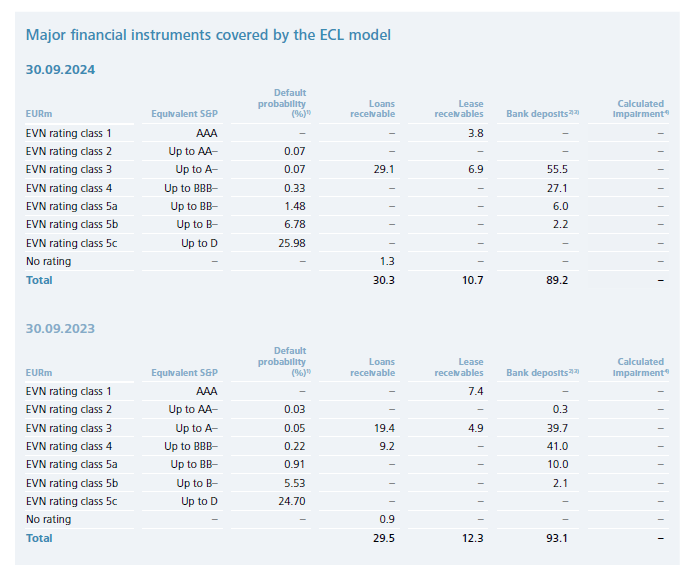

The following table includes information on the default risk and expected credit losses for financial instruments carried at amortised cost. It does not cover trade receivables, receivables from equity accounted investees, receivables from non-consolidated investments or amounts due from employees. The risk allowance for all financial instruments represents the expected 12-month credit loss because the default risk is low. The amounts shown in the table include both current and non-current components.

1) Assumed loss ratio (60% for banks, 80% for corporates)

2) Due to the daily maturity, a one-day probability of default is applied to account balances; for money market deposits, the PoD of the average volume-weighted residual term is taken into account.

3) Bank balances also include restricted cash in the amount of EUR 12.1m (previous year: EUR 22.9m).

4) The calculated impairments are not recognised in the balance sheet due to their minor magnitude.

EVN uses the practical expedient provided by IFRS 9.B5.5.35 for trade receivables and calculates the expected credit losses with a provision matrix. The input factors include analyses of default incidents in previous financial years based on different regional characteristics for the core markets. These factors form the basis for the development of a provision matrix with different time ranges.

In the current situation, it is particularly important to evaluate how the macroeconomic environment will influence the expected credit losses on trade receivables. The economic developments in recent years did not lead to a sharp rise in receivables defaults by customers, in particular because of numerous government support measures. However, this has currently been reflected in an increasing number of insolvencies in Europe, and we expect higher receivables defaults in the future. For this reason, the EVN Group recognised a EUR 5.1m (previous year: EUR 5.0m) higher impairment loss to trade receivables for the 2023/24 financial year via a forward-looking component.

The following tables include information on the default risk and expected credit losses for trade receivables, which were determined on the basis of a provision matrix for EVN’s core markets:

The overview of expected credit losses in North Macedonia includes both current and non-current trade receivables. Following the conclusion of instalment agreements with customers in North Macedonia, existing trade receivables were reclassified as non-current. These receivables are not considered part of overdue receivables and, consequently, this category carries a higher average probability of default than the category “up to 89 days overdue”.

The remaining gross trade receivables of EUR 62.2m (previous year: EUR 102.8m) are related primarily to the international project business. As the majority of clients are state-related companies, the probability of default was assessed using external ratings and the receivables were individually impaired if necessary. For receivables with a gross carrying amount of EUR 30.2m (previous year: EUR 70.7m), which fall into stage 3, impairments totalling EUR 15.4m (previous year: EUR 23.7m) were recognized.

In financial year 2023/24, impairments of EUR 36.7m (previous year: EUR 20.7m) were recognised for trade receivables. The impairments mainly resulted from expected credit losses under consideration of a provision matrix. As in the previous year, no impairment of contract assets was necessary.

The following table shows the development of impairment losses to trade receivables in 2023/24:

The Group’s maximum default risk for the items reported on the consolidated statement of financial position as of 30 September 2024 and 30 September 2023 reflect the carrying amounts shown in notes 39. Other non-current assets, 41. Trade and other receivables and 42. Securities and other financial investments, excluding financial guarantees.

The maximum default risk for derivative financial instruments equals the positive fair value (see note 63. Reporting on financial instruments).

The maximum risk from financial guarantees is described in note 65. Other obligations and risks.