Ørsted A/S – Annual report – 31 December 2025

Industry: utilities, energy

Note 5.3

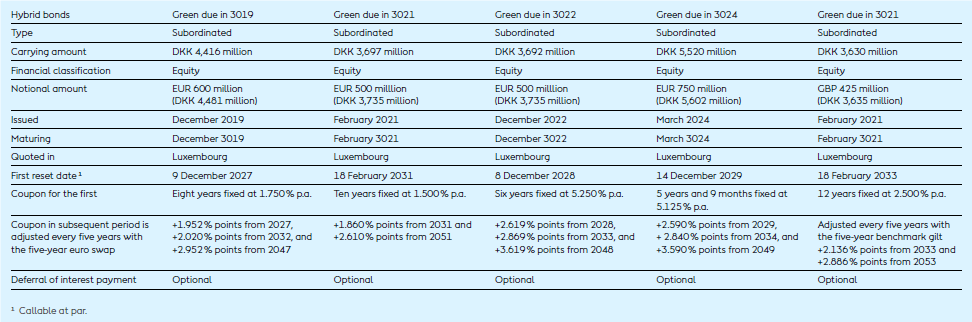

Hybrid capital

We have issued hybrid capital which is subordinate to our other creditors. The purpose of issuing hybrid capital is to strengthen our capital base and fund our investments. We have issued EUR hybrid bonds with a total nominal value of EUR 2,350 million and GBP 425 million, respectively, equivalent to DKK 21,188 million (2024: EUR 2,350 million and GBP 425 million, respectively, equivalent to DKK 21,358 million).

For all our hybrid bonds, we have the right to defer coupon payments and ultimately decide not to pay them at maturity. Deferred coupon payments become payable, however, if we decide to pay dividends to our shareholders or pay coupon payments on other hybrid bonds. As a consequence of these terms, the hybrid bonds are classified as equity, and therefore coupon payments are recognised in equity.

Accounting policies

Hybrid capital comprises issued bonds that qualify for treatment in accordance with the rules on compound financial instruments due to the special characteristics of the bonds. The notional amount, which constitutes a liability, is recognised at present value, and equity has been increased by the difference between the net proceeds received and the present value of the discounted liability. The carrying amount of the liability component amounted to nil on initial recognition as the only payment obligation is the repayment of the nominal value in 1,000 years.

Coupon payments are accounted for as dividends, which are recognised directly in equity at the time the payment obligation arises. This is because the coupon is discretionary, and therefore any deferred coupon lapses upon maturity of the hybrid capital. Coupon payments are recognised in the statement of cash flows within financing activities.

On redemption of hybrid capital, the payment will be distributed between liability and equity, applying the same ratio as when the hybrid capital was issued. This means that the difference between the payment on redemption and the net proceeds received on issue is recognised directly in equity, as the liability portion of the existing hybrid issues will be nil during the first part of the life of the hybrid capital.