Sasol Limited – Annual report – 30 June 2025

Industry: oil and gas, mining

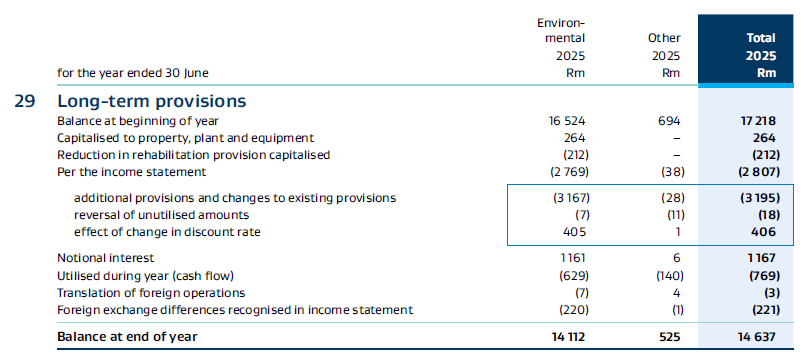

PROVISIONS

Environmental provisions

The environmental obligation includes estimated costs for the rehabilitation of coal mining, oil, gas and petrochemical sites, mainly in South Africa and Mozambique.

The present value of the environmental provisions is determined by discounting the estimated future cash outflows using interest rates of high-quality government bonds that are denominated in the currency in which the amounts will be paid, and that have terms approximating the terms of the related obligation.

The following discount rates were applied:

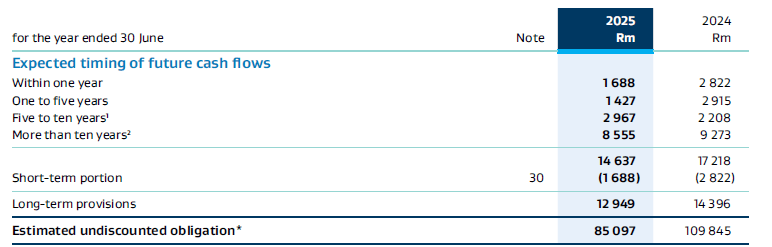

The time at which the operations cease to produce economically viable returns and the pace of transition to a low carbon economy will impact the anticipated time period over which decommissioning liabilities are expected to be incurred in future.

1 Relates largely to the rehabilitation of coal mining, oil and gas sites in South Africa.

2 Relates largely to the plugging and abandonment of gas wells in Mozambique, as well as remediation of soil and ground water contamination in South Africa.

* Decrease relates mainly to a reassessment of cost estimates based on optimised water treatment cost as a result of enhanced evaporating technology and other enhancements.

In line with the requirements of the legislation of South Africa, the utilisation of certain investments is restricted for mining rehabilitation purposes. These investments amounted to R885 million (2024 – R816 million) and are included in Other long-term investments in the statement of financial position. In addition, indemnities of R2 907 million (2024 – R2 860 million) are in place.

Accounting policies:

Estimated long-term environmental provisions, comprising pollution control, rehabilitation and mine closure, are based on the Group’s environmental policy taking into account current technological, environmental and regulatory requirements. The provision for rehabilitation is recognised as and when the environmental liability arises. To the extent that the obligations relate to the construction of an asset, they are capitalised as part of the cost of those assets. The effect of subsequent changes to assumptions in estimating an obligation for which the provision was recognised as part of the cost of the asset is adjusted against the asset. Any subsequent changes to an obligation which did not relate to the initial construction of a related asset are charged to the income statement. The increase in discounted long-term provisions as a result of the passage of time is recognised as a finance expense in the income statement.

The estimated present value of future decommissioning costs, taking into account current environmental and regulatory requirements, is capitalised as part of property, plant and equipment, to the extent that they relate to the construction of the asset, and the related provisions are raised. These estimates are reviewed at least annually.

Deferred tax is recognised on the temporary differences in relation to both the asset to which the obligation relates to and rehabilitation provision.

Areas of judgement:

The determination of long-term provisions, in particular environmental provisions, remains a key area where management’s judgement is required. Estimating the amount and timing of the future cost of these obligations is complex and requires management to make estimates and judgements because most of the obligations will only be fulfilled in the future and contracts and laws are often not clear regarding what is required. The resulting provisions could also be influenced by changing technologies and political, environmental, safety, business and statutory considerations as well as the period in which it will be settled. The pace of transition to a low carbon economy will impact the anticipated time period over which decommissioning liabilities are expected to be incurred.

Accounting policies:

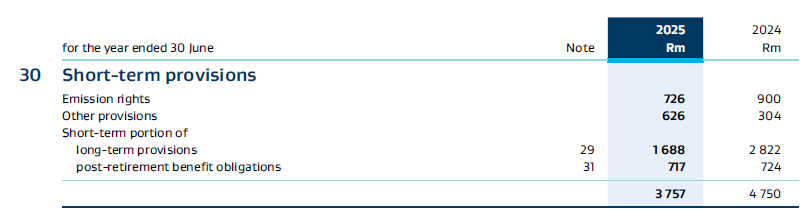

In emission schemes where a cap is set for emissions, the associated emission rights granted are recognised at fair value and classified under intangible assets. An emission liability is recognised under short-term provisions when actual emissions occur that give rise to an obligation. To the extent the liability is covered by emission rights held, the liability is measured with reference to the value of these emission rights held and for the remaining uncovered portion at current market value. The associated expense is presented under Materials, energy and consumables used. Both the emission rights intangible asset and the emission liability are derecognised upon settling the liability with the respective regulator.