Swisscom Ltd – Annual report – 31 December 2025

Industry: telecoms

3 Operating assets and liabilities (extract)

3.1 Net current operating assets (extract)

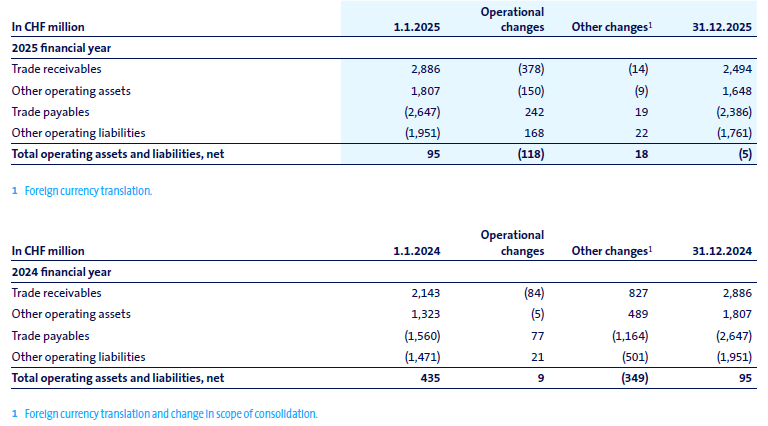

Change in operating assets and liabilities (extract)

Trade receivables

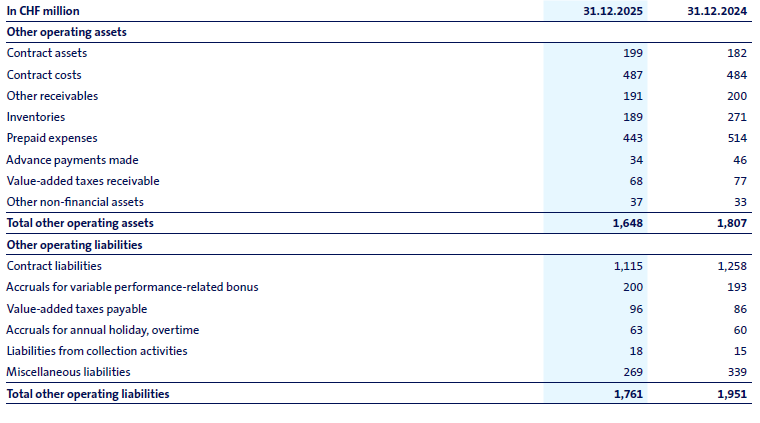

Other operating assets and liabilities

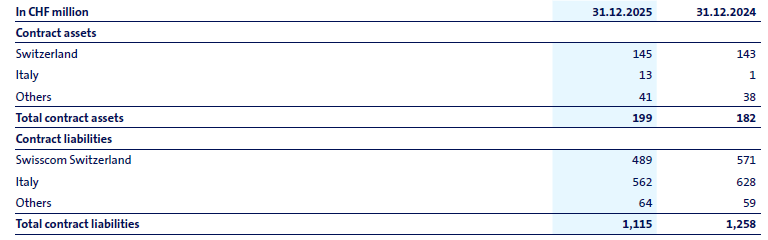

Contract assets and liabilities

Contract assets in the Switzerland segment mainly relate to deferred revenue arising from bundled offerings in the mobile business. Under these arrangements, mobile handsets are sold at a subsidised price together with a mobile service contract. Due to the allocation of revenue between the handset (a pre-delivered component) and the service element, revenues are recognised earlier than the invoicing, resulting in the recognition of contract assets. Contract liabilities mainly comprise deferred revenue from payments for prepaid cards and subscription fees relating to prepaid services.

Accounting policies

Operating assets and liabilities

Total operating assets and liabilities used in the normal course of business are disclosed as current items in the balance sheet.

Trade receivables

Trade receivables are measured at amortised cost less impairment losses. Impairment losses on trade receivables are recognised, depending on the nature of the underlying transaction, either on an individual basis or using a portfolio-based approach which reflects the anticipated credit default risk. For portfolio-based valuation allowances, financial assets are grouped by homogeneous credit risk characteristics and assessed collectively for expected credit losses. In determining impairment losses, Swisscom considers contractual payment terms, historical default rates, as well as current and forward-looking information relevant to credit risk. Impairment losses on trade receivables are recognised as direct costs.

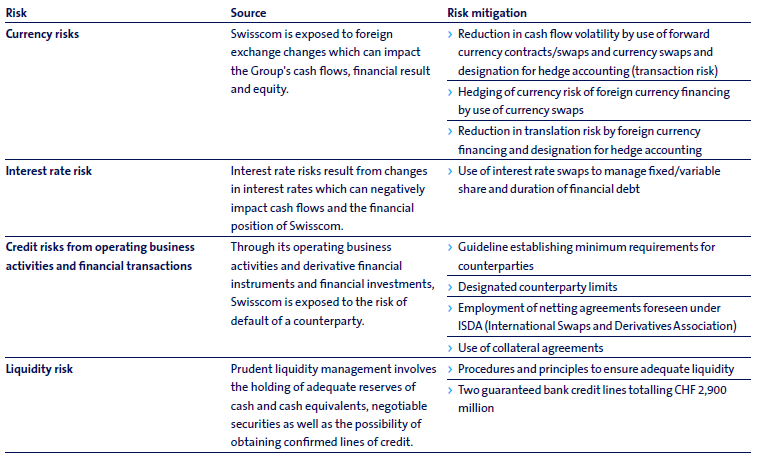

2.5 Financial risk management (extract)

Swisscom is exposed to various financial risks arising from its operating and financing activities. The management of financial risk is conducted in accordance with established guidelines, with the objective of limiting the potential adverse effects on Swisscom’s financial position.

Identified risks and measures implemented to mitigate these risks

Credit risks (extract)

Financial risks from operating activities

Credit risks on trade receivables, contract assets and other receivables arise from Swisscom’s operating activities. Credit risks from other receivables are insignificant. Swisscom allocates credit risks from operating activities to the operating segments Switzerland and Italy. The risk of default primarily depends on the specific characteristics of each customer, as well as on the credit quality of customer groups and the industry sector. Swisscom operates a receivables management system designed to minimise credit losses. New customers are assessed for creditworthiness and maximum payment terms are defined for each customer group. Customers are classified into groups according to their creditworthiness for ongoing monitoring of default risks, distinguishing, among other factors, between residential and business customers. In addition, the ageing profile of receivables and the industry in which a business customer operates are taken into account.

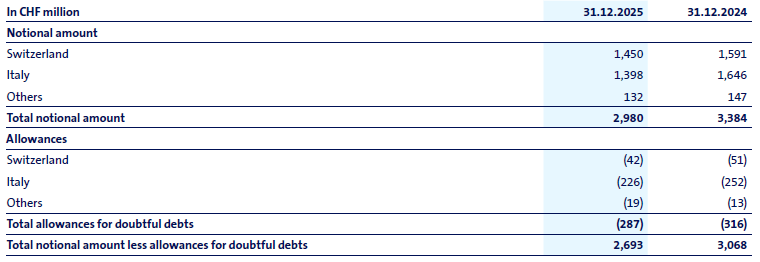

The split of trade receivables and contract assets by operating segment is as follows:

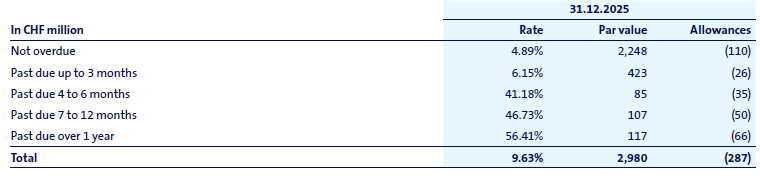

As at 31 December 2025, the ageing of trade receivables and contract assets, including related loss allowances, is as follows:

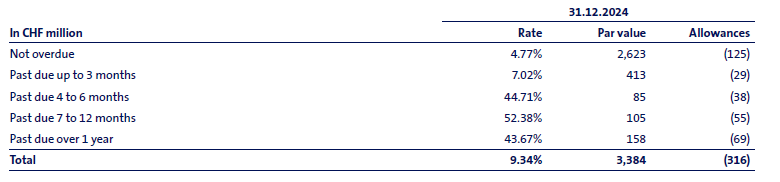

As at 31 December 2024, the ageing of trade receivables and contract assets, including related loss allowances, is as follows:

Movements in loss allowances for trade receivables and contract assets are as follows: