Air New Zealand Limited – Annual report – 30 June 2020

Industry: airlines

27. Impact of New Accounting Standards and Interpretations (extract)

IFRIC Interpretation

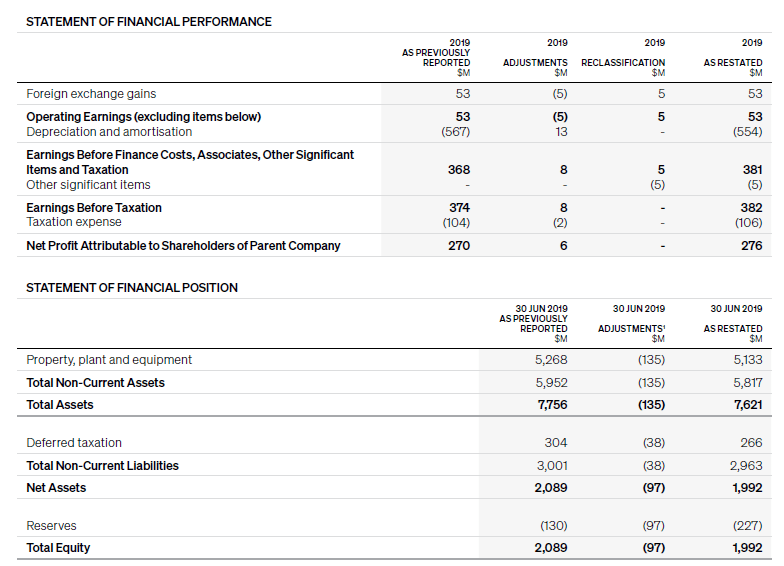

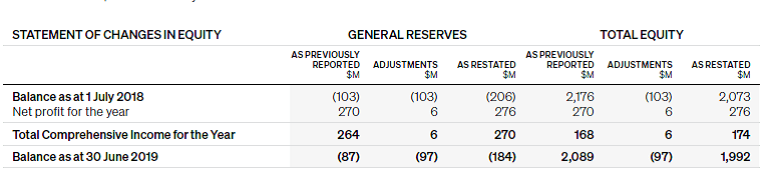

In September 2019, the International Financial Reporting Interpretations Committee (“IFRIC”) published an agenda decision in respect of a “Fair Value Hedge of Foreign Currency Risk on Non-Financial Assets”. The new interpretation by IFRIC of the principles of IFRS 9 – Financial Instruments no longer permits certain fair value hedges of underlying United States Dollar aircraft values previously undertaken by the Group. The interpretation has now been applied retrospectively. The impact of the change on the prior year comparatives is set out below:

- as a result of retrospectively applying the IFRIC agenda decision, cumulative foreign exchange gains recognised within aircraft assets were reversed. The impact in the year to 30 June 2019 was $5 million, offset by $13 million of depreciation expense on the accumulated position.

- the above adjustments resulted in $5 million of foreign exchange losses, which arose upon retranslation of previously designated debt in the year to 30 June 2019, now having no offsetting hedged item. Given that Group policy requires such items to be hedged, this has been reclassified to ‘Other significant items’.

1 As at 30 June 2019, the retrospective application of IFRIC’s agenda decision resulted in a decrease of $135 million in aircraft assets, representing accumulated foreign exchange losses recognised up to the date of the change, offset by a decrease of $38 million in deferred taxation. An amount of $103 million was recognised through opening retained earnings as at 1 July 2018 offset by net profit after taxation of $6 million in the year to 30 June 2019.

3. Other Significant Items (extract)

Other significant items are items of revenue or expenditure which due to their size and nature warrant separate disclosure to assist with the understanding of the underlying financial performance of the Group.

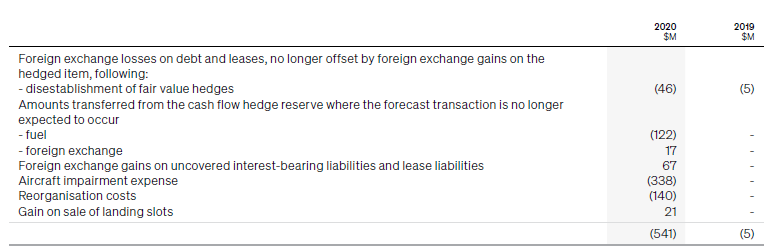

Foreign exchange losses on debt and leases, no longer offset by foreign exchange gains on the hedged item

Disestablishment of fair value hedges

In September 2019, the International Financial Reporting Interpretations Committee (“IFRIC”) published an agenda decision in respect of a “Fair Value Hedge of Foreign Currency Risk on Non-Financial Assets”. The interpretation issued by IFRIC of the principles of IFRS 9 – Financial Instruments no longer permits certain fair value hedges of underlying United States Dollar aircraft values which were previously undertaken by the Group. The interpretation has been applied retrospectively in the financial statements. The impact on the comparative period is set out in Note 27.

As a result of the reversal of the fair value hedges, $46 million of foreign currency losses arising on translation of the previously designated debt, was no longer offset by foreign currency gains arising on the hedged item for the year ended 30 June 2020 (30 June 2019: $5 million). In September 2019 the debt was subsequently re-designated in new hedge relationships in accordance with the Group’s financial risk management policies.