Sysmex Corporation – Annual report – 31 March 2018

Industry: healthcare

- POST-EMPLOYMENT BENEFITS (extract)

Additionally, the Company and certain of its subsidiaries participate in multi-employer plans – the Pension Fund of Japan Electronics Information Technology Industry and the Osaka Pharmaceutical Employees’ Pension Fund. While these pension plans are defined benefit plans, sufficient information has not been available to use defined benefit accounting, and consequently, the amounts of contributions have been recognized as retirement benefit expenses, similar to those of defined contribution plans. In addition, special contributions to such plans are recognized as liabilities discounted to the present value for the portion in which the amount to be borne by the Group has been clarified through actuarial recalculation, while such liabilities are reversed upon payment of special contributions (see “16. PROVISIONS”).

In December 5, 2017, the Pension Fund of Japan Electronics Information Technology Industry decided to dissolve in March 31, 2018, at their conference of representatives. Residual assets would be distributed to active members, deferred members, and pensioners. However for the Company’s employees, if they desire, the residual assets allocated to them will be transferred to defined contribution plans. The Company will compensate the shortage between planned payments and allocated residual assets. The payment for the compensation will be made for four years after the distribution.

Following this event, as of March 31, 2018, the provision for special contribution of ¥1,886 million ($17,792 thousand) was reversed and recorded as reversal of “Cost of sales,” “Selling, general and administrative expenses,” and “Research and development expenses.” The shortage amount ¥285 million ($2,689 thousand) was recognized as “Long-term financial liabilities,” and recorded as “Cost of sales,” “Selling, general and administrative expences,” and “Research and development expenses.” The shortage amount will not be determined before FY2019 so it is recorded by allocation based on information from the pension.

The Osaka Pharmaceutical Employees’ Pension Fund also announced its dissolution on March 28, 2018, but this had no material impact on the financial position of the Group and its operating results.

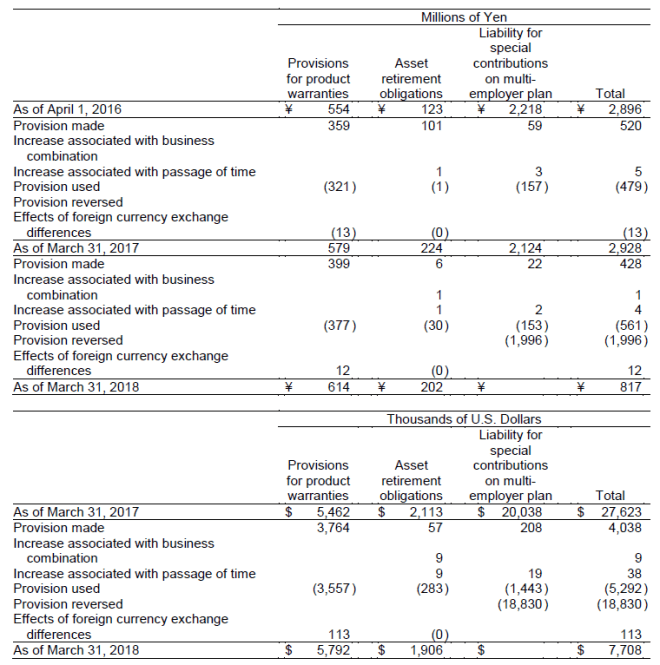

- PROVISIONS

Reconciliations of provisions from the beginning balances to the ending balances are as follows:

As a provision for product warranties, the Group recognized the expected service expenses within the warranty period based on historical data. In most cases, the warranty period is one year.

Asset retirement obligations mainly consist of obligations to restore rented buildings and other assets to their original states. While such expenses are expected to be paid after their estimated period of use, they are affected by future business plans and other factors.

For liability for special contributions on multi-employer plan, please refer to “17. POST-EMPLOYMENT BENEFITS.”