Genus plc – Annual report – 30 June 2025

Industry: agriculture

Notes to the Group Financial Statements (extract)

16. BIOLOGICAL ASSETS

The Group applies quantitative genetics and biotechnology to animal breeding. We use these techniques to identify and select animals with the genes responsible for superior milk and meat, high health and performance traits. We sell breeding animals, semen and embryos to customers, who use them to produce offspring which yield greater production efficiency and milk and meat quality, for the global dairy and meat supply chain. We recognise that accounting for biological assets is an area which includes key sources of estimation uncertainty. These are outlined in note 4 and sensitivities are provided below.

Accounting policies

Biological assets and inventories

In bovine, we use research and development to identify genetically superior bulls in a number of breeds, primarily the Holstein dairy breed. Each selected bull has its performance measured against its peers, by using genomic evaluations and progeny testing of its daughters’ performance. We collect and freeze semen from the best bulls, to satisfy our customers’ demand. Farmers use semen from dairy breeds to breed replacement milking stock. They use the semen we sell from beef breeds in either specialist beef breeding herds, for multiplying breeding bulls for use in natural service, or on dairy cows to produce animals to be reared for meat.

Our research and development also enables us to produce and select our own genetically superior females, from which we will breed future bulls.

We hold our bovine biological assets for long-term internal use and classify them as non-current assets. We transfer bull semen to inventory at its fair value at the point of harvest, which becomes its deemed cost under IAS 2. We state our inventories at the lower of this deemed cost and net realisable value.

Sorting semen is a production process rather than a biological process. As a result, we transfer semen inventory into sexed semen production at its fair value at the point of harvest, less the cost to sell, and it becomes a component of the production process. We carry sexed semen in finished goods at production cost.

In porcine, we maintain and develop a central breeding stock (the ‘nucleus herd’), to provide genetically superior animals. These genetics help make farmers and food processors more profitable, by increasing their output of consistently high-quality products, which yield higher value. So we can capitalise on our intellectual property, we outsource the vast majority of our pig production to our global multiplier network. We also sell the offspring or semen we obtain from animals in the nucleus herd to customers, for use in commercial farming.

Pig sales generally occur in one of two ways: ‘upfront’ and ‘royalty’. Under upfront sales, we receive the full fair value of the animal at the point we transfer it to the customer. Under royalty sales, the pig is regarded as comprising two separately identifiable components: its carcass and its genetic potential. We receive the initial consideration, which is approximately the animal’s carcass value, at the point we transfer the pig to the customer. We retain our interest in the pig’s genetic potential and receive royalties for the customer’s use of this genetic potential.

The breeding animal biological assets we own, and our retained interest in the biological assets we have sold under royalty contracts, are recognised and measured at fair value at each balance sheet date. We recognise changes in fair value in the Income Statement, within operating profit for the period.

We classify the porcine biological assets we are using as breeding animals as non-current assets and carry them at fair value. The porcine biological assets we are holding for resale, which are the offspring of the breeding herd, are carried at fair value and classified as current assets.

Determination of fair values – biological assets

IAS 41 ‘Agriculture’ requires us to show the carrying value of biological assets in the Group Balance Sheet. We determine this carrying value according to IAS 41’s provisions and show the net valuation movement in the Income Statement. There are important differences in how we value our bovine and porcine assets, as explained below.

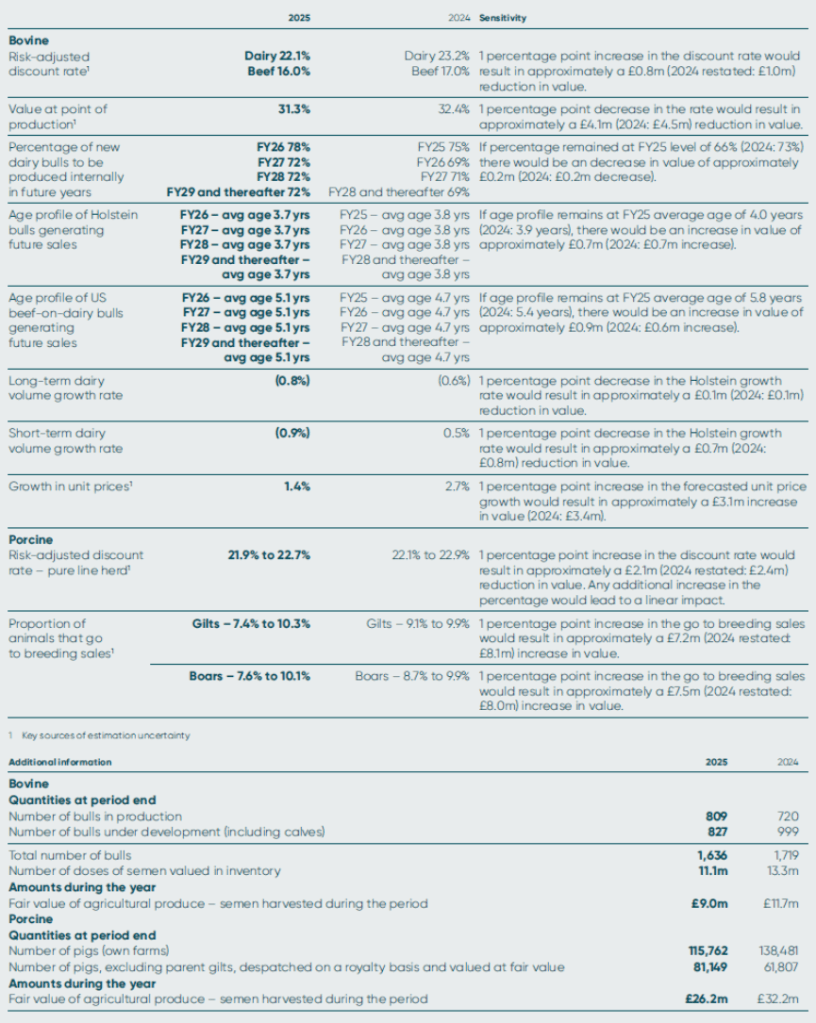

Bovine – we base the fair value of all bulls on the net cash flows we expect to receive from selling their semen, discounted at a current risk-adjusted market-determined rate. The significant assumptions determining the fair values are the expected future demand for semen, the estimated biological value and the marketable life of bulls. The biological value is the estimated value at the point of production. We adjust the fair value of the bovine herd and semen inventory where a third party earns a royalty from semen sales from a particular bull. Females are valued by reference to market prices and published independent genetic evaluations.

Porcine – the fair value of porcine biological assets includes the animals we own entirely and our retained interest in the genetics of animals we have sold under royalty arrangements. The fair value of animals we own is calculated using the animals’ average live weights, plus a premium where we believe that their genetics make them saleable. We base the live weight value and the genetic premium on recent transaction prices we have achieved. The significant assumptions in determining fair values are the breeding animals’ expected life, the percentage of production animals that are saleable as breeding animals and the expected sales prices. For our retained interest in the genetics of animals sold under royalty contracts, we base the initial fair value on the fair values we achieved in recent direct sales of similar animals, less the amount we received upfront for the carcass element. We then remeasure the fair value of our retained interest at each reporting date. The significant assumption in determining the fair value of the retained interest is the animals’ expected life.

We value the pigs in our pure line herds, which are the repository of our proprietary genetics, as a single unit of account. We do this using a discounted cash flow model, applied to the herds’ future outputs at current prices. The significant assumptions we make are the number of future generations attributable to the current herds, the fair value prices we achieve on sales, the animals’ expected useful lifespan and productivity, and the risk-adjusted discount rate.

Non-recognition of porcine multiplier contracts where the Group does not retain a contractual interest

To manage commercial risk, a very large part of our porcine business model involves selling pigs to farmers (‘multipliers’) who produce piglets on farms we neither manage nor control. We have the option, but not the obligation, to buy the offspring at slaughter market value plus a premium. Because the offspring have superior genetics, we can then sell them to other farmers at a premium.

We do not recognise the right to purchase offspring on the Group Balance Sheet, as we enter into the contracts and continue to hold them for the purpose of receiving non-financial items (the offspring), in accordance with our expected purchase requirements. This means the option is outside the scope of IFRS 9. We do not recognise the offspring as biological assets under IAS 41, as we do not own or control them.

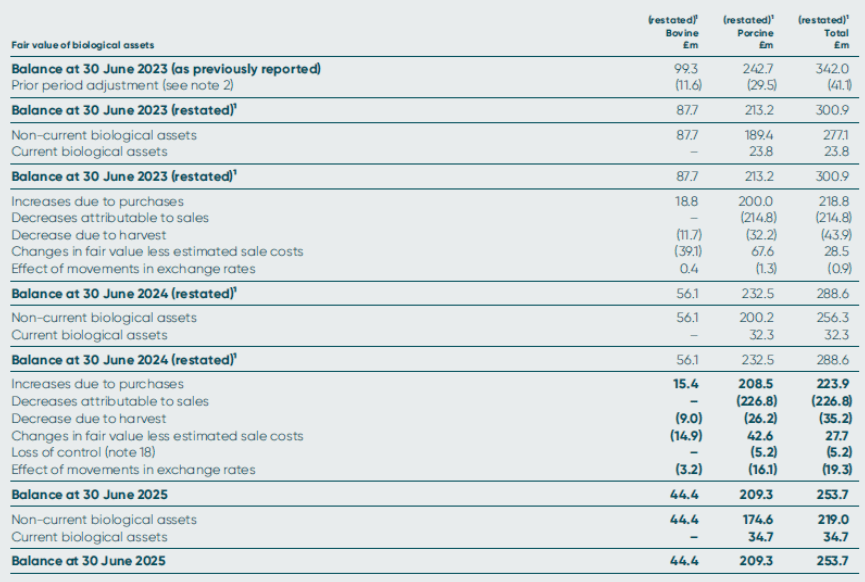

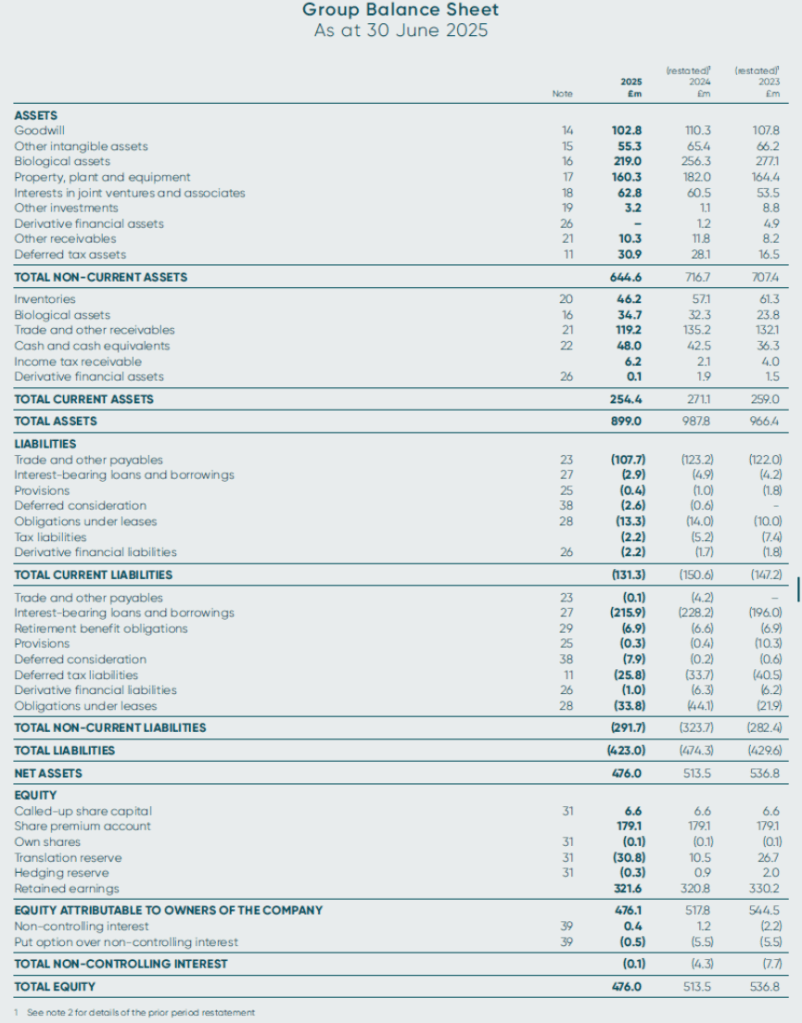

1 See note 2 for details of prior period restatement

Bovine

Bovine biological assets include £2.7m (2024: £7.7m) representing the fair value of bulls owned by third parties but managed by the Group, net of expected future payments to such third parties, which are therefore treated as assets held under leases.

There were no movements in the carrying value of the bovine biological assets in respect of sales or other changes during the year.

A risk-adjusted rate of 16.0% Beef – 22.1% Dairy (2024: 17.0% Beef – 23.2% Dairy) has been used to discount future net cash flows from the sale of bull semen.

Decreases due to harvest represent the semen extracted from the biological assets. Inventories of such semen are shown as biological asset harvest in note 20.

Porcine

Included in increases due to purchases is the aggregate increase arising during the year on initial recognition of biological assets in respect of multiplier purchases, other than parent gilts, of £72.5m (2024 restated: £76.9m).

Decreases attributable to sales during the year of £226.8m (2024 restated: £214.8m) include £96.3m (2024 restated: £129.7m) in respect of the reduction in fair value of the retained interest in the genetics of animals, other than parent gilts, transferred under royalty contracts.

Also included is £58.6m (2024 restated: £63.3m) relating to the fair value of the retained interest in the genetics in respect of animals, other than parent gilts, sold to customers under royalty contracts in the year.

Total revenue in the year, including parent gilts, includes £245.3m (2024: £259.7m) in respect of these contracts, comprising £67.7m (2024: £82.3m) on initial transfer of animals and semen to customers and £177.6m (2024: £177.4m) in respect of royalties received.

Risk-adjusted rates of between 21.9% and 22.7% (2024 restated: 22.1% and 22.9%) have been used to discount future net cash flows from the expected output of the pure line porcine herds. The number of future generations which have been taken into account is seven (2024: seven) and their estimated useful lifespan is 1.4 years (2024: 1.4 years).

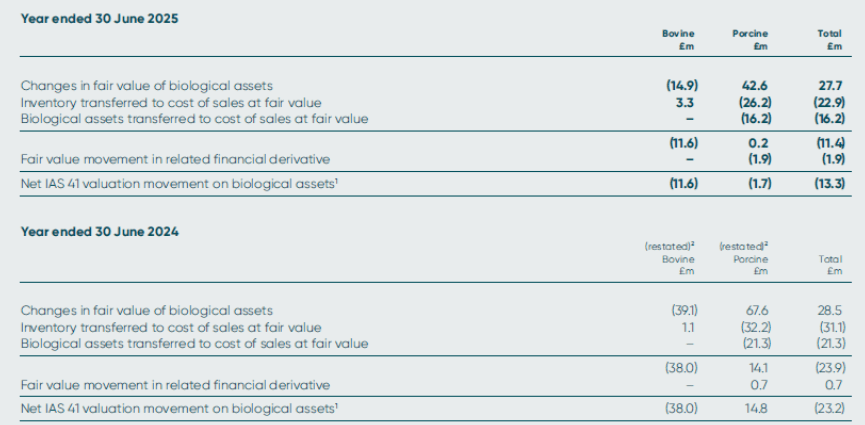

1 This represents the difference between operating profit prepared under IAS 41 and operating profit prepared under historical cost accounting, which forms part of the reconciliation to adjusted operating profit (see APMs)

2 See note 2 for details of prior period restatement

Fair value measurement

All of the biological assets inputs fall under Level 3 of the hierarchy defined in IFRS 13. Significant increases/(decreases) in any of these inputs in isolation would result in a significantly lower or higher fair value measurement.

Unobservable inputs and key sources of estimation uncertainty

4. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY (extract)

Key sources of estimation uncertainty (extract)

Determination of the fair value of biological assets including those held in equity-accounted investees (note 16 and note 18)

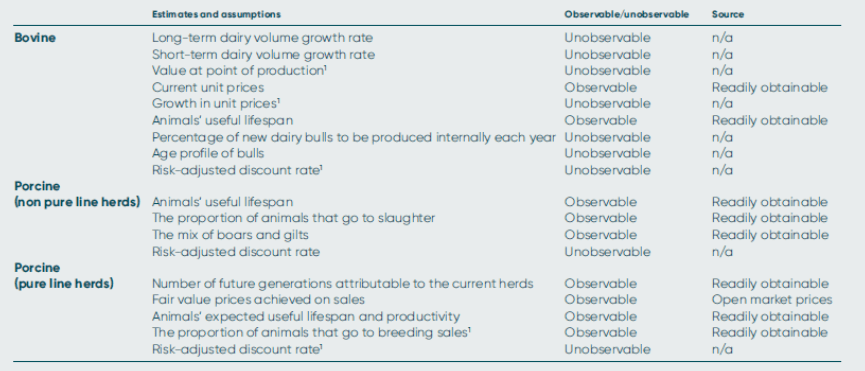

Determining the fair values of our bovine and porcine biological assets requires the application of a number of estimates and assumptions.

Below is a list of these estimates and assumptions, showing whether we consider them to be observable or unobservable inputs to the fair value determination. In addition, we identify those inputs that are ‘readily obtainable’ transactional data or ‘open market prices’. Sensitivities of the estimates and assumptions given below are disclosed in note 16.

1 Key sources of estimation uncertainty

2. BASIS OF PREPARATION (extract)

Restatement in the 2024 and 2023 Group Balance Sheet

In estimating the fair value of the bovine and porcine biological assets a discounted cash flow model is used. In assessing the appropriateness of the discount rate used we consider assumptions and estimates a market participant may use in establishing a fair value for the assets. The cash flows used in the model are pre-tax and a long-term pre-tax risk adjusted discount rate is applied which is derived from the Group’s post-tax WACC calculation. IAS 41 requires the cash flows to be applied over the living animals useful life, and we have estimated this to be 10 years for both species.

During FY25, management reviewed the approach in determining the fair value of bovine and porcine biological assets. In doing so the historical transaction information and the discount rate used to establish a fair value were considered, and it was concluded that there were insufficient recent third-party market transactions to support the approach of using a long-term pre-tax risk adjusted discount rate to establish a fair value. As such we restated the 2024 and 2023 fair values to reflect the shortening of our view of a long term pre-tax adjusted rate to 10 years consistent with the pre-tax cash flows and this has resulted in an increase in the risk adjusted discount rate used from a range of 11.4% to 13.3% if the prior years’ approach was adopted, and revised it to 16% to 22.7%, dependent on species type.

Consequently, the prior period balance sheets at 30 June 2024 and 30 June 2023 have been restated in accordance with IAS 8, and, in accordance with IAS 1 (revised). A balance sheet at 30 June 2023 is also presented together with related notes. The restatements involved are a reduction in biological assets at 30 June 2024 and 30 June 2023 of £41.1m and a reduction in related deferred tax liabilities at 30 June 2024 and 30 June 2023 of £10.7m.

Impact on the Group’s Balance Sheet for year ended 30 June 2024

For the year ended 30 June 2024, there has been no material effect on the Group Income Statement, Group Statement of Comprehensive Income and no impact on the Group Statement of Cash Flows. Therefore, there has been no restatement of the Group Income Statement and there is no adjustment to earnings per share.

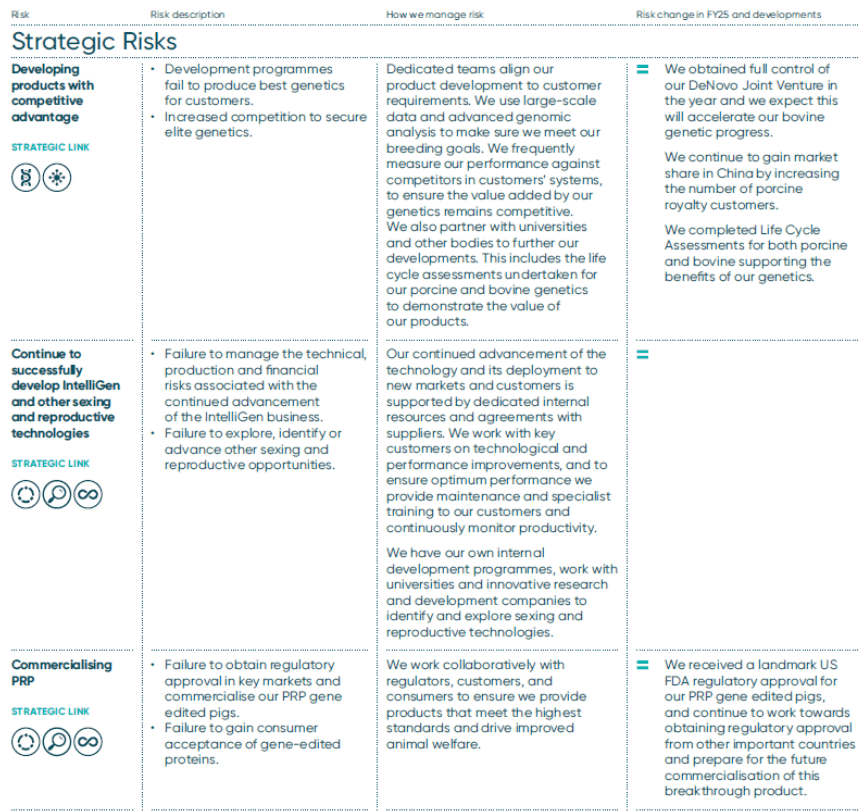

Principal Risks and Uncertainties (extract)

Strategic Risks (extract)

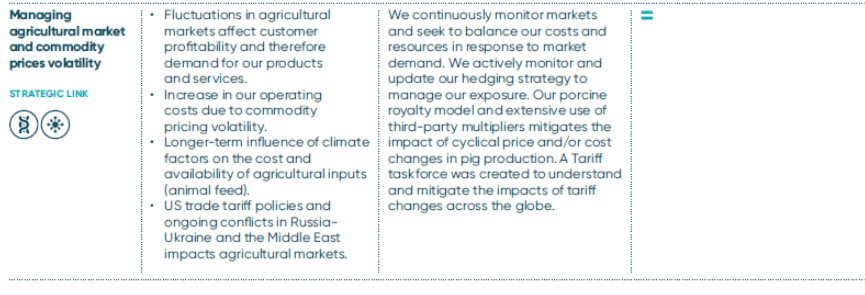

Financial Risks (extract)

Operational Risks (extract)

26. FINANCIAL INSTRUMENTS (extract)

Commodity hedges

The Group hedges both feed and slaughter exposures using Chicago Mercantile Exchange lean hog, corn and soybean meal commodity futures contracts.