Dunelm Group plc – Annual report – 29 June 2024

Industry: retail

Task Force on Climate-related Financial Disclosures (‘TCFD’)

The Board recognises the risks and opportunities posed by climate change to the Group’s business model and strategy.

Introduction

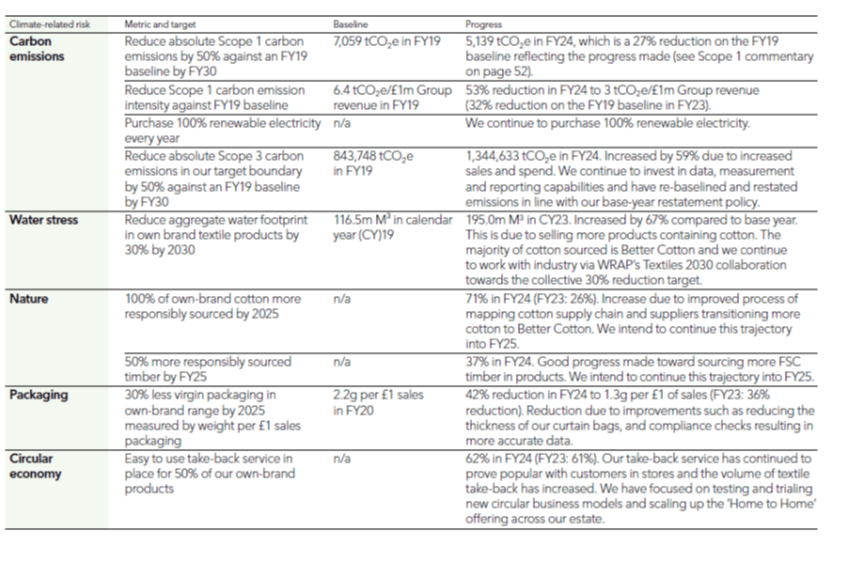

Climate change has been managed as a principal risk for the Group since FY19; the current view of this risk is described in detail on page 45. Following release of our first full TCFD report in FY22 and progress made in FY23, we have developed our approach to assessing risks and opportunities and remain committed to improving disclosures in line with evolving requirements and practice. This year, we brought in-house the assessment of financial impact for climate related risks and opportunities enabling more tailored data and assumptions to be used. Additionally, new internal processes have helped improve focus on potential impacts across the business.

Our report continues to be compliant with TCFD disclosures and UK Listing Rules. We continue to consider the potential financial impacts of climate change in the cash flow scenario modelling within our viability statement on page 55 and in our accounting policies note on page 137 of the financial statements.

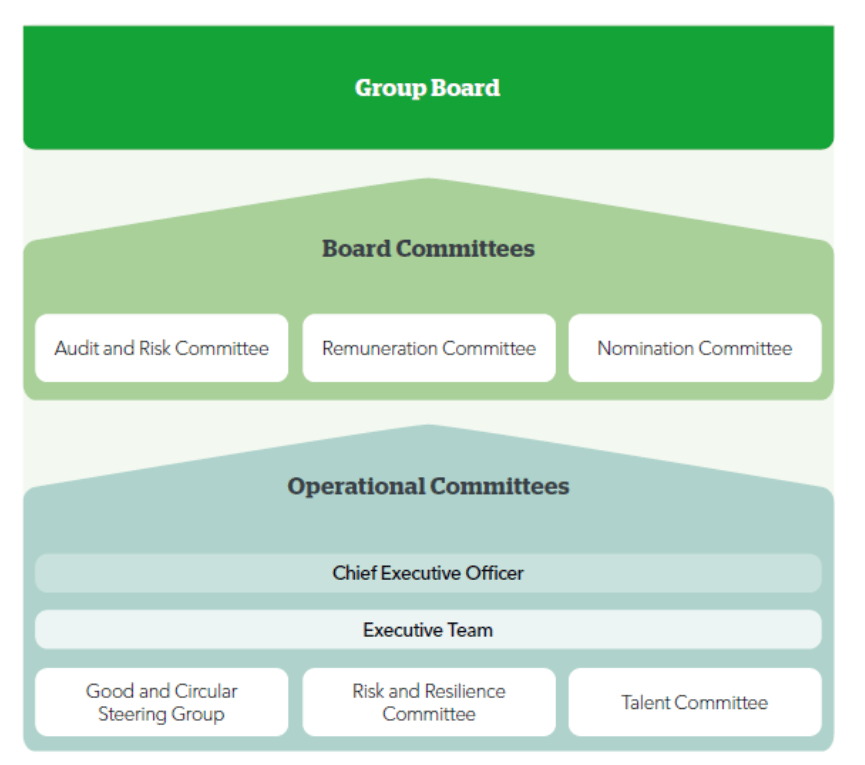

Governance

Governance a) Board’s oversight of climate-related risks and opportunities

The Board takes overall responsibility for our climate change roadmap. It considers our approach, strategy, risk management and performance, receiving regular updates on progress against our climate-related KPIs, as well as other related topics such as water reduction and product circularity. It continues to listen and learn about the implications of climate change on the Group’s business model.

This year the Board received an update on our emerging Scope 3 emissions reduction roadmap, as well as our broader ‘Good & Circular’ strategy, looking at circularity, carbon and responsible sourcing, as well as our overall approach to governance and reporting (which is explained in more detail on the following page).

The Board is supported by the Audit and Risk Committee, Remuneration Committee and Nomination Committee.