Diageo plc – Annual report – 30 June 2025

Industry: food and drink

Accounting information and policies (extract)

(f) Hyperinflationary accounting

The group applied hyperinflationary accounting for its operations in Türkiye, Ghana and Venezuela.

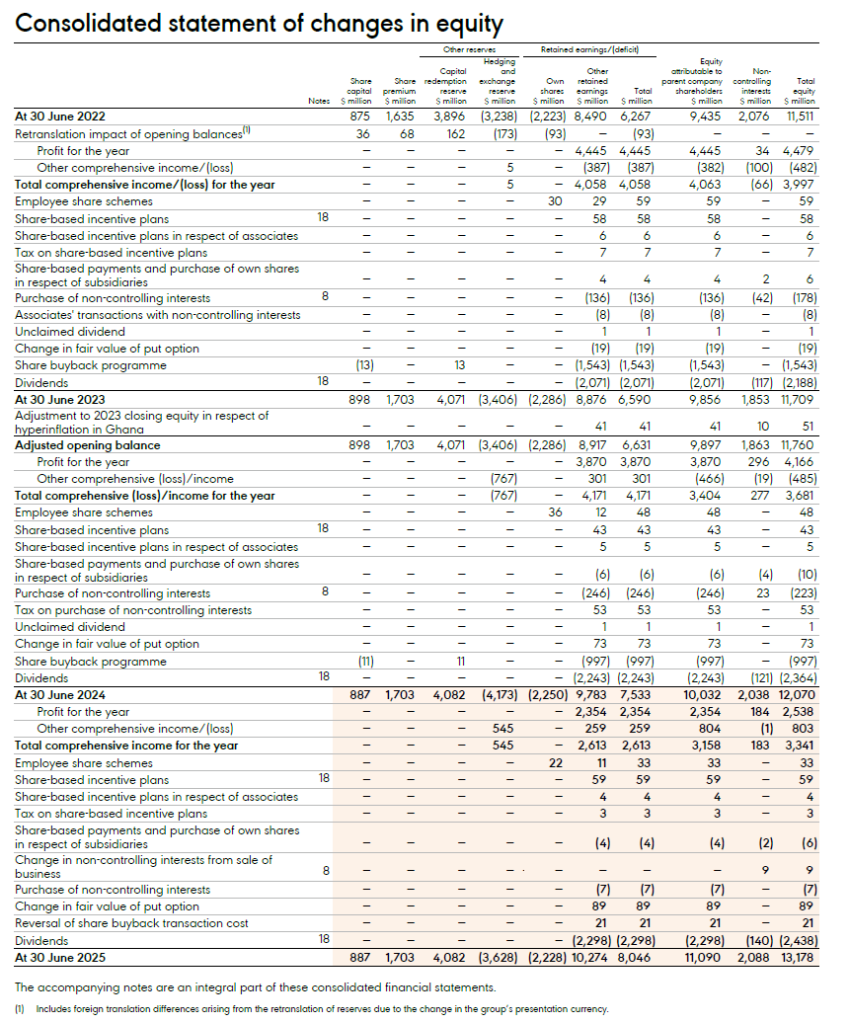

The group applies hyperinflationary accounting for its operations in Ghana starting from 1 July 2023. Hyperinflationary accounting needs to be applied as if Ghana had always been a hyperinflationary economy, hence, as per Diageo’s accounting policy choice, the differences between equity at 30 June 2023 as reported and the equity after the restatement of the non-monetary items to the measuring unit current at 30 June 2023 were recognised in retained earnings.

The group’s consolidated financial statements include the results and financial position of its operations in hyperinflationary economies restated to the measuring unit current at the end of each period, with hyperinflationary gains and losses in respect of monetary items being reported in finance income and charges. Comparative amounts presented in the consolidated financial statements are not restated. When applying IAS 29 on an ongoing basis, comparatives in stable currency are not restated and the effect of inflating opening net assets to the measuring unit current at the end of the reporting period is presented in other comprehensive income. The movement in the publicly available official price index for the year ended 30 June 2025 was 35% (2024 – 72%; 2023 – 38%) in Türkiye and 16% (2024 – 23%) in Ghana. The inflation rate used by the group for Venezuela is provided by an independent valuer because no reliable, officially published rate is available. Movement in the price index for the year ended 30 June 2025 was 171% (2024 – 77%; 2023 – 382%) in Venezuela.

During the year ended 30 June 2024, developments in Venezuela led management to change its estimate for the exchange rate of VES/$ to be the official exchange rate published by Bloomberg. Figures for the year ended 30 June 2024 and 30 June 2025 show the results of the Venezuelan operation consolidated at the official closing exchange rate of the period.

5. Finance income and charges

Accounting policies

Net interest includes interest income and charges in respect of financial instruments and the results of hedging transactions used to manage interest rate risk.

Finance charges directly attributable to the acquisition, construction or production of a qualifying asset, being an asset that necessarily takes a substantial period of time to get ready for its intended use or sale, are added to the cost of that asset. Borrowing costs which are not capitalised are recognised in the income statement using the effective interest method. All other finance charges are recognised primarily in the income statement in the year in which they are incurred.

Net other finance charges include items in respect of postemployment plans, the discount unwind of long-term obligations and hyperinflation charges. The results of operations in hyperinflationary economies are adjusted to reflect the changes in the purchasing power of the local currency of the entity before being translated to US dollar.

The impact of derivatives, excluding cash flow hedges that are in respect of commodity price risk management or those that are used to hedge the currency risk of highly probable future currency cash flows, is included in interest income or interest charge.

(1) Includes $101 million interest income and $854 million interest charge in respect of financial assets and liabilities that are not measured at fair value through income statement (2024 – $59 million income and $765 million charge; 2023 – $98 million income and $628 million charge).

(2) Cumulative impact of prior years’ unrecognised borrowing costs reclassified to qualifying assets.