TUI AG – Annual report – 30 September 2025

Industry: Leisure

(14) Property, plant and equipment (extract)

In the financial year 2025, the assumptions regarding the expected residual values of Marella Cruise Ltd’s cruise ships were revised. Unlike the previous year, it is now assumed that, upon expiry of their economic useful life, the vessels can be disposed of at values exceeding scrap value. As a result, the estimated residual values of the cruise ships were increased by €56.9 million in total. This adjustment led to a decrease in depreciation expense of €3.5m for the current financial year. For the financial year 2026, depreciation expense is expected to decline by €7.0m due to this change.

Accounting principles (extract)

Property, plant and equipment

Property, plant and equipment are measured at amortised cost. The costs to purchase include costs to bring the asset to a working condition. The costs to produce are determined on the basis of direct costs and directly attributable indirect costs and depreciation.

Borrowing costs directly associated with the acquisition, construction or production of qualifying assets are included in the costs to acquire or produce these assets until the assets are ready for their intended use.

To the extent that funds are borrowed specifically for the purpose of obtaining a qualifying asset, the underlying capitalisation rate is determined on the basis of the specific borrowing cost; in all other cases the weighted average of the borrowing costs applicable to the borrowings outstanding is applied.

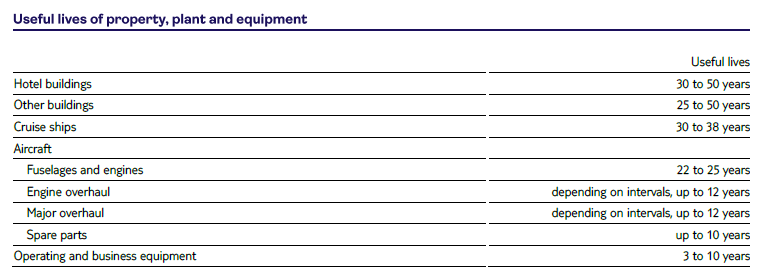

Depreciation of property, plant and equipment is based on the straight-line method over the useful economic life. The useful economic lives are as follows:

Moreover, the level of depreciation is determined by the residual values at the end of the useful life of an asset. The residual value assumed at first-time recognition for cruise ships is between 4% and 30% of the acquisition costs. In the financial year 2025, the assumptions regarding the residual value of the ships of Marella Cruise Ltd were changed. For further information, please refer to the Note 14 ‘Property, Plant and Equipment’. The determination of the depreciation of aircraft fuselages and aircraft engines in first-time recognition is based on a residual value of a maximum of 5 % of the cost of acquisition. In addition, a residual value of 20 % is used to determine the scheduled depreciation of spare parts. The payments made under a power by the hour arrangement relating to maintenance overhauls are capitalised as PPE under construction up to a maintenance event at which point the cost is transferred to the appropriate PPE category.

Both the useful lives and residual values are reviewed on an annual basis when preparing the Group financial statements. The review of the residual values is based on comparable assets at the end of their useful lives as at the balance sheet date. Any adjustments required are recognised as a correction of depreciation over the remaining useful life of the asset. Where the review results in an increase in the residual value so that it exceeds the remaining net carrying amount of the asset, depreciation is suspended. In this case, the amounts are not written back.

Any losses in value going beyond wear-and-tear depreciation are taken into account through the recognition of impairment losses. If there are any events or indications suggesting impairment, the required impairment test is performed to compare the carrying amount of an asset with the recoverable amount.