Hochtief AG – Annual report – 31 December 2019

Industry: construction

1. Accounting policies (extract 1)

Financial reporting standards applied for the first time in 2019 (extract)

IFRS 16 Leases:

As of January 1, 2019, the HOCHTIEF Group adopted IFRS 16 “Leases”, which replaces IAS 17 “Leases”, IFRIC 4 “Determining Whether an Arrangement Contains a Lease”, SIC-15 “Operating Leases—Incentives” and SIC-27 “Evaluating the Substance of Transactions Involving the Legal Form of a Lease”.

The Group adopted IFRS 16 using the full retrospective approach. HOCHTIEF did apply the practical expedient not to reassess whether a contract is, or contains, a lease at the date of initial application. It applies the definition of a lease only to contracts entered into (or changed) on or after the date of initial application. The Group also exercises the option of aggregating lease and non-lease components with the exception of real estate leases and recognizing them uniformly as leases in the balance sheet.

IFRS 16 sets out the principles for the recognition, measurement, presentation and disclosure of leases and requires lessees to account for all leases under a single on-balance sheet model similar to the accounting for finance leases under IAS 17. Lessor accounting under IFRS 16 is substantially unchanged from the accounting under IAS 17 and has no material impact on the Group.

From a lessee perspective, at the commencement date of a lease, a lessee recognizes a liability to make lease payments (“lease liability”) and an asset representing the right to use the underlying asset during the lease term (“right-of-use asset”). HOCHTIEF presents the interest expense on the lease liability separately from the depreciation charge on the right-of-use asset.

Lessees are also required to remeasure the lease liability upon the occurrence of certain events (such as a change in the lease term or lease payments). The amount of the remeasurement of the lease liability is recognized as an adjustment to the right-of-use asset.

Operating lease expenses continue to exist for short-term leases (up to 12 months) as well as for low-value assets.

Effects of first-time application of IFRS 16

The Group has applied IFRS 16 in full retrospectively and therefore, the comparative figures have been restated as if the new accounting policy had always been applied. The disclosure notes have also been restated where required for comparatives under new disclosure requirements. The adjustments due to the application of the new standard for the Consolidated Balance Sheet, Consolidated Statement of Earnings and Consolidated Statement of Cash Flows are presented below.

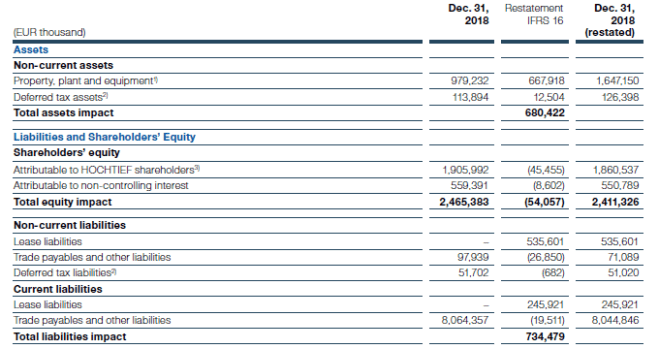

Impact on Consolidated Balance Sheet as of December 31, 2018

1) IFRS 16 has led to recognized amounts for right-of-use assets within property, plant and equipment and lease liabilities on the face of the balance sheet representing the Group’s portfolio of leased assets made up by property, plant, operating equipment and vehicles utilized by the Group.

2) Adjustments under IFRS 16 are subject to tax effect accounting and therefore the net deferred tax position has been impacted.

3) At December 31, 2018, the retained earnings adjustment has increased by around EUR 3 million (EUR 45.5 million).

Impact on Consolidated Balance Sheet as of January 1, 2018

4) IFRS 16 has led to recognized amounts for right-of-use assets within property, plant and equipment and lease liabilities on the face of the balance sheet representing the Group’s portfolio of leased assets made up by property, plant, operating equipment and vehicles utilized by the Group.

5) Adjustments under IFRS 16 are subject to tax effect accounting and therefore the net deferred tax position has been impacted.

6) Retained earnings have been adjusted at January 1, 2018 for the impact of IFRS 16 using the full retrospective method which led to a decrease in equity of EUR 48.5 million.

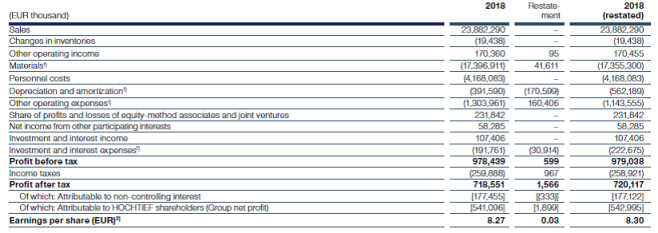

Impact on Consolidated Statement of Earnings as of December 31, 2018

1) IFRS 16 changed the amount and presentation of lease-related expenses. Under IAS 17, operating lease expenses were presented as operating expenses, whereas IFRS 16 splits the lease expense into depreciation of the right-of-use assets recognized and investment and interest expenses on lease liabilities. This has driven a decrease in the operating lease expense and increases in depreciation and finance costs. Consequently, this has also impacted the Group’s EBITDA.

2) The adjusted profit has led to a marginal change in the Group’s earnings per share.

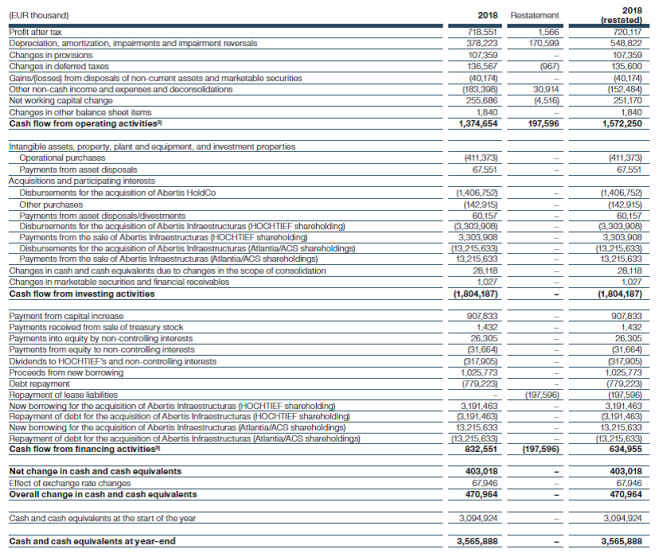

Impact on Consolidated Statement of Cash Flows as of December 31, 2018

3) Lease payments are now classified within financing activities which were previously operating cash flows. The interest portion of the cash payment has also been included as financing activities. This has led to an increase in cash flows from operating activities and a decrease in net cash inflows from financing activities.

Lease recognition

The Group as lessee

The Group assesses whether a contract is or contains a lease, at inception of a contract. A contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration. In such instances, the Group recognizes a right-of-use asset and a corresponding lease liability with respect to all lease agreements, except for short-term, cancelable leases that if canceled by the lessee, the losses associated with the cancellation are borne by the lessor and low-value leased assets. For these leases, the Group recognizes the lease payments as an operating expense on a straight-line basis over the term of the lease unless another systematic basis is more representative of the time pattern in which economic benefits from the leased assets are consumed.

The Group has a significant lease portfolio, comprising of predominately property, plant, operating equipment and fleet vehicle rentals. Given the Group’s operational involvement in the construction, construction management and services sectors, leasing equipment is a key component of the business.

Measurement and presentation of lease liability

The lease liability is initially measured at the present value of the lease payments that are not paid at the commencement date, discounted by using the rate implicit in the lease. If this rate cannot be readily determined, the Group uses its incremental borrowing rate.

The following items are also included in the measurement of the lease liability:

• Fixed lease payments offset by any lease incentives;

• Variable lease payments, for lease liabilities which are tied to a floating index;

• The amounts expected to be payable to the lessor under residual value guarantees;

• The exercise price of purchase options (if it is reasonably certain that the option will be exercised); and

• Payments of penalties for terminating leases, if the lease term reflects the lease terminating early.

The lease liability is separately disclosed in the balance sheet. The liabilities which will be repaid within 12 months are recognized as current and the liabilities which will be repaid in excess of 12 months are recognized as non-current.

The lease liability is subsequently measured by reducing the balance to reflect the principal lease repayments made and increasing the carrying amount by the interest on the lease liability.

The Group is required to remeasure the lease liability and make an adjustment to the right-of-use asset in the following instances:

• The term of the lease has been modified or there has been a change in the Group assessment of the purchase option being exercised, in which case the lease liability is remeasured by discounting the revised lease payments using a revised discount rate;

• A lease contract is modified and the lease modification is not accounted for as a separate lease, in which case the lease liability is remeasured by discounting the revised lease payments using a revised discount rate; and

• The lease payments are adjusted due to changes in the index or a change in expected payment under a guaranteed residual value, in which cases the lease liability is remeasured by discounting the revised lease payments using the initial discount rate. However, where the lease payments change is due to a change in a floating interest rate a revised discount rate is used.

Measurement and presentation of right-of-use assets

The right-of-use assets recognized by the Group comprise the initial measurement of the related lease liability, any lease payments made at or before the commencement of the contract, less any lease incentives received and any direct costs. Costs incurred by the Group to dismantle the asset, restore the site or restore the asset are included in the cost of the right-of-use asset.

It is subsequently measured under the cost model with any accumulated depreciation and impairment losses applied against the right-of-use asset. If the cost of the right-of-use asset reflects that the Group will exercise a purchase option, the right-of-use asset is depreciated from the commencement date to the end of the useful life of the underlying asset. Otherwise, the Group depreciates the asset over the shorter period of either the useful life of the asset or the lease term. The depreciation starts at the commencement date of the lease and the carrying value of the asset is adjusted to reflect the accumulated depreciation balance.

Any remeasurement of the lease liability is also applied against the right-of-use asset value.

The right-of-use assets are presented within property, plant and equipment in the balance sheet.

Lessor recognition

The Group enters into lease agreements as a lessor with respect to some property subleases as well as renting equipment to its partners, suppliers and contractors. Those leases are recognized as either finance or operating leases. lf the terms of the lease transfer substantially all the risks and rewards of ownership to the lessee, the contract is classified as a finance lease. lf this is not the case, then the lease is recognized as an operating lease. The income received from the operating leases is recognized on a straight-line basis over the lease term. Initial direct costs incurred in negotiating and arranging operating leases are included in the carrying amount of the leased asset. Amounts due from lessees under finance leases are recognized as receivables.

1. Accounting policies (extract 2)

Judgments made by management in applying the accounting policies primarily relate to the following matters:

• Construction/PPP and construction management/services business

– determination of stage of completion;

– estimation of total contract costs;

– estimation of total contract revenue, including recognizing revenue on contract variations and claims only to the extent it is highly probable that a significant reversal in the amount recognized will not occur in the future;

– estimation of a customer’s preparedness to accept contract variations and claims;

– estimation of project completion date; and

– assumed levels of project execution productivity.

• Estimation of allowance for expected credit losses on financial assets.

• Determination of whether an arrangement constitutes a lease.

• Leases must be assessed to determine whether the substantial risks and rewards of beneficial ownership transfer to the lessee.

• Financial assets may be measured, irrespective of measurement category, at fair value through profit or loss.

• Application of the risk management strategy to hedges.

• Assets earmarked for sale must be assessed to confirm that they are available for immediate sale and their sale is highly probable. If the result of this assessment is positive, those assets and any liabilities to be disposed of in the same transaction must be reported and accounted for as assets held for sale and liabilities associated with assets held for sale.

The decision made by the HOCHTIEF Group for general application in each instance is set out under Accounting Policies in these Notes.

Preparation of the IFRS Consolidated Financial Statements requires Group management to make estimates and assumptions that affect the reported amount of assets, liabilities, income and expenses, and disclosures of contingencies, commitments, and other obligations. The main estimates and assumptions relate to the following:

• Assessing projects on a percentage of completion basis, in particular with regard to accounting for contract modifications, the timing of profit recognition, and the amount of profit recognized.

• Estimating the economic life of intangible assets, property, plant and equipment, and of investment properties.

• The measurement of expected credit losses.

• The estimation of residual value guarantees and options for the purchase of lease liabilities.

• The estimation of options to extend a lease.

• Accounting for provisions.

• Testing goodwill on the basis of the three-year plan or, in the case of listed companies, on the basis of the share price and other assets for impairment

• The assessment of the recognition of deferred taxes considering the expected future performance of the business in line with Group strategy

All estimates and assumptions are based on current circumstances and appraisals. Forward-looking estimates and assumptions made as of the balance sheet date with a view to future business performance take account of circumstances prevailing on preparation of the Consolidated Financial Statements and future trends considered realistic for the global and industry environment. Actual amounts can vary from the estimated amounts due to changes in the operating environment that are at variance with the assumptions and lie beyond management control. If such changes occur, the assumptions and, if necessary, the carrying amounts of affected assets and liabilities are revised accordingly.

6. Depreciation and amortization (extract)

In accordance with IFRS 16, depreciation on right-of-use assets from leases has been added to the 2018 figures. This increased the 2018 expense from EUR 391,590 thousand to EUR 562,189 thousand.

10. Net investment and interest income (extract)

The figures for interest and similar expenses in 2018 have been restated for the interest expense on lease liabilities. This increased interest expense for 2018 from EUR 160,758 thousand to EUR 191,672 thousand.

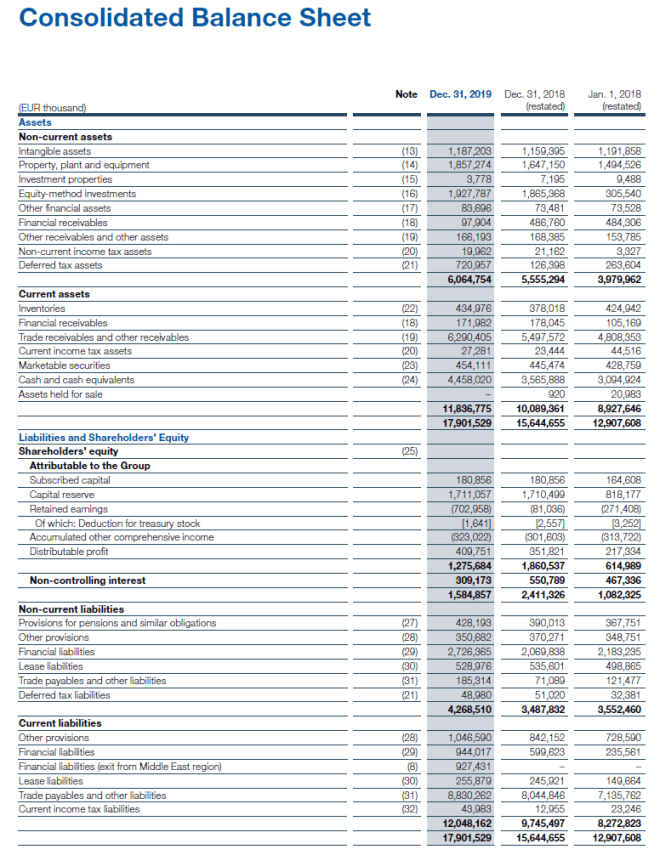

14. Property, plant and equipment

As in the prior year, no impairment losses were recorded on property, plant and equipment and, as in the prior year, property, plant and equipment is not subject to any restrictions.

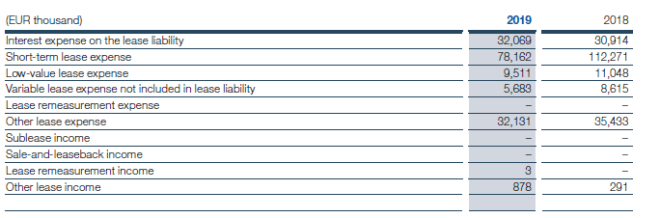

30. Lease liabilities

Lease liabilities total EUR 784,855 thousand (2018 restated: EUR 781,522 thousand), divided into non-current liabilities of EUR 528,976 thousand (2018 restated: EUR 535,601 thousand) and current liabilities of EUR 255,879 thousand (2018 restated: EUR 245,921 thousand).

The following amounts are recognized in connection with leases:

Total cash outflows from leases amount to EUR 424,768 thousand (2018: EUR 364,963 thousand).

Certain leases contain extension options by the Group up to one year before the end of the non-cancelable contract period. Where practicable, the Group seeks to include extension options in new leases to provide operational flexibility. The extension options held are exercisable only by the Group and not by the lessors. The Group assesses at lease commencement whether it is reasonably certain to exercise the extension options, and where it is reasonably certain, the extension period has been included in the lease liability. The Group reassesses whether it is reasonably certain to exercise the options if there is a significant event or significant change in circumstances within its control.

Certain lease contracts may include an option to buy out the asset at the end of the lease term or include contingent rental guarantees where the Group could be exposed to the variability of returns in relation to return conditions at lease expiry. The Group will include the payments for the contingent rental guarantee or the buy-out option only if it is reasonably certain that the payment will occur at the end of the lease term. The Group reassesses whether it is reasonably certain to exercise the options if there is a significant event or significant change in circumstances within its control.

The maturity analysis of lease liabilities is shown in Note 34.