Barratt Redrow plc – Annual report – 29 June 2025

Industry: real estate

Section 172 Statement

Promoting long-term success through stakeholder engagement

Stakeholder relationships are a key source of value and promote the long‑term sustainable success of the Company.

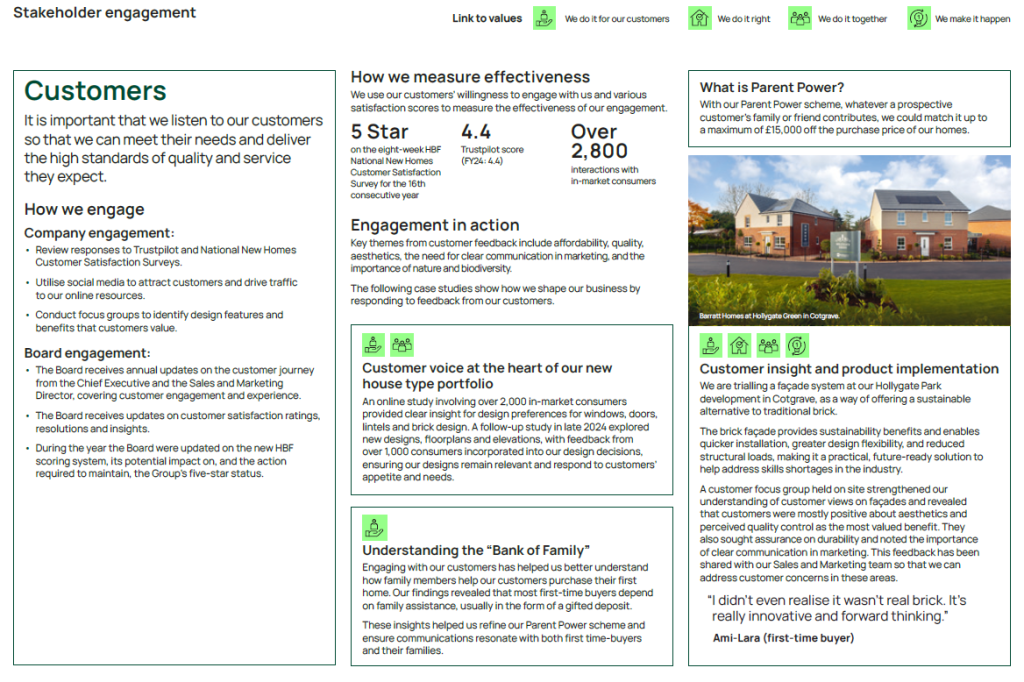

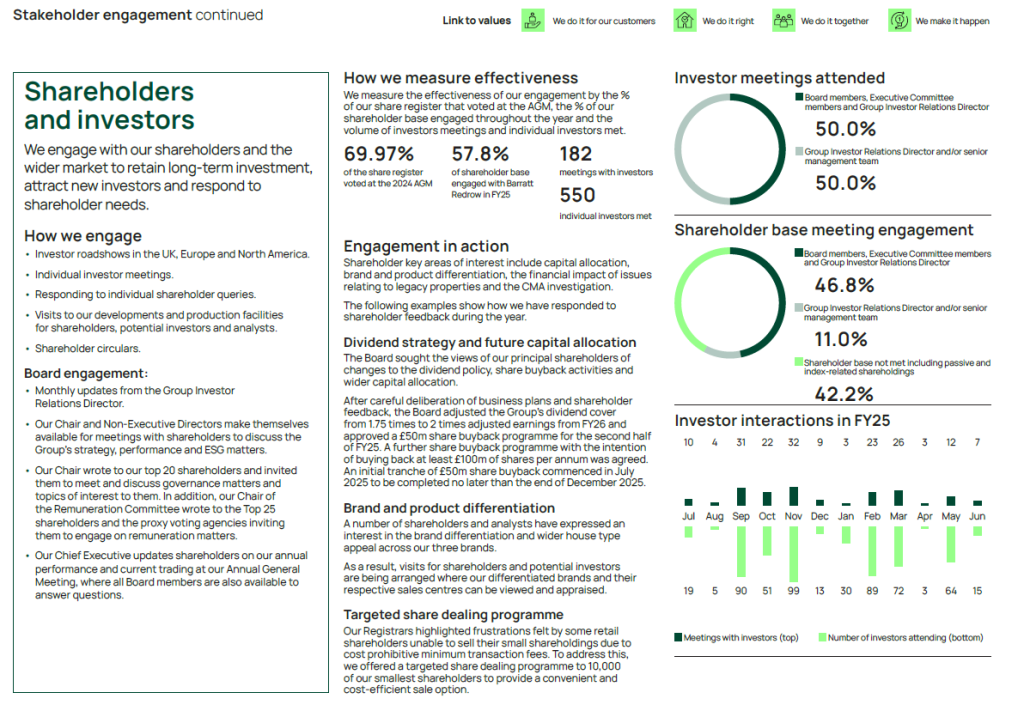

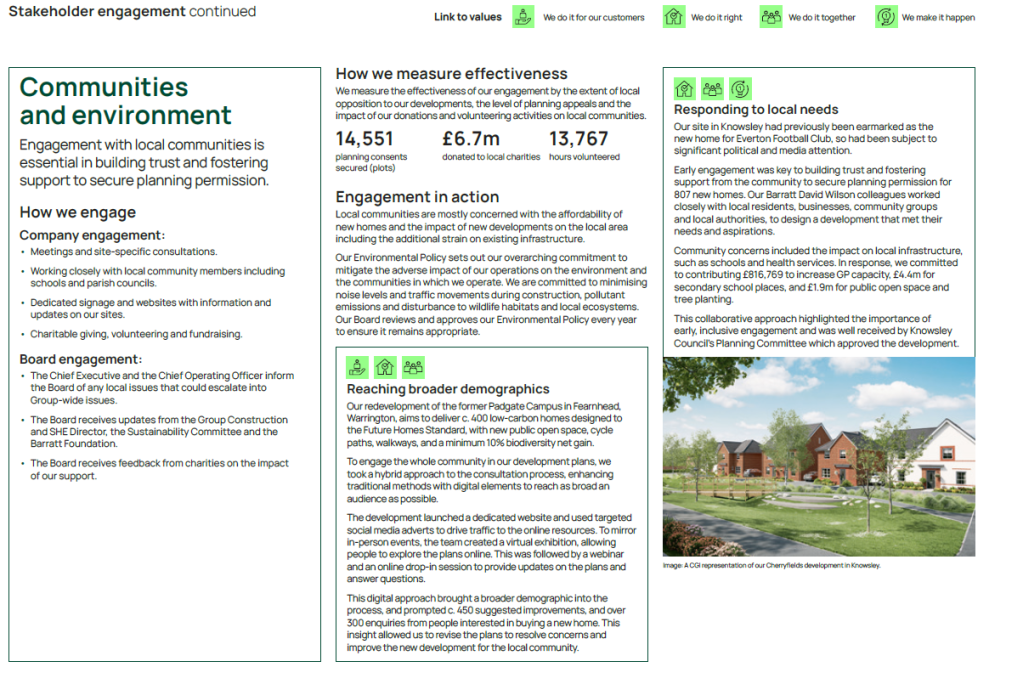

Stakeholder engagement plays a key role in the development and execution of our strategy and is critical to achieving long‑term sustainable success. We are committed to high standards of corporate governance and making sure that the principles set out in Section 172 of the Companies Act 2006 are embedded in our culture and all that we do as a Company. On the following pages we set out how we as a Board engage with our stakeholders and ensure that all stakeholder views, whether positive or negative, are understood and embedded into our discussions and decision‑making process.

You can read about how we have paid due regard to the Section 172 principles on pages 49 and 50

As a Board we review the Company’s key stakeholders on an annual basis to ensure that they remain appropriate and consider whether there are other stakeholder groups whose views should form part of our discussions. To ensure that engagement remains effective, we also review key metrics and performance indicators for various engagement activities. During the year, we considered stakeholder engagement as part of the Board evaluation process and, whilst satisfied that engagement remains effective for fostering business relationships, agreed actions to further enhance direct engagement between Board members and the Company’s key stakeholder groups.

Most day‑to‑day decisions and stakeholder engagement activities are carried out by members of our Executive Committee and senior management team. Our values, as set out on page 1, are closely aligned to the Section 172 principles and are embedded in our culture, ensuring that our key stakeholders and the Section 172 principles are considered during the decision‑making process at all levels of the business.

We appreciate that there may be times when conflicts arise between different stakeholder groups and that it is not always possible to provide positive outcomes for all. In such circumstances, we seek to understand the needs and priorities of each stakeholder group and make the decision from the perspective of the long‑term sustainable success of the business.

Section 172 principles

How we applied the principles in FY25

Decision making in practice

Entering into the MADE Partnership.

Significant decisions

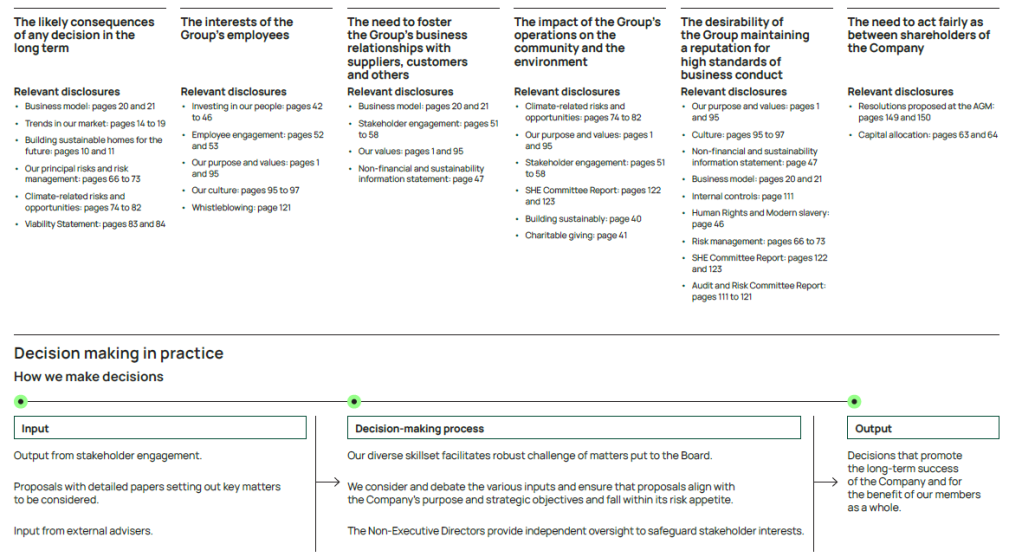

The main activities and decisions of the Board during the year are set out on page 94. Below is an example of a significant decision taken by the Board during the year, including the key inputs that informed discussions, stakeholder considerations and the outcome of that decision.

Decision

On 9 September 2024, the Board agreed to enter into a joint venture with Homes England and Lloyds Banking Group to create the MADE Partnership, an entity that will focus on the master development of large sites, to deliver thousands of much needed new homes across the country.

Key inputs:

- Detailed Board papers setting out the strategic rationale, current market conditions and appetite for master developers, risk analysis and stakeholder considerations.

- Counsel from external advisers on tax and legal matters.

Stakeholder considerations

The Board discussed entering into the joint venture on a number of occasions prior to giving their approval, with due regard given to the following stakeholder considerations.

Government, opposition and regulators:

- The Government and opposition’s commitment to ramp up housing supply and boost economic growth.

- The increasing preference of local planning authorities to allocate very large sites to meet their housing requirements.

- Homes England’s strategic plan to grow the master developer sector, and use its land, funding and powers to deliver ambitious development and regeneration projects.

- The need for ministerial approval to ensure that the deal protects Homes England’s long‑term interests as a public body.

Local communities and environment:

- The need for residential‑led developments with a variety of community facilities and employment uses.

- The preference to develop large brownfield sites, as well as new garden village style communities, to minimise impact on existing infrastructure.

- The guiding principles that would govern the way the Partnership would operate, with focus on affordable housing, sustainability, quality of design, placemaking, promoting modern methods of construction, social value, community engagement and supporting SME housebuilders.

Customers:

- Providing greater customer choice by enabling both major and SME homebuilders to build the new homes and communities.

Banks:

- The role of the Lloyds Banking Group as a major investor in UK housing including traditional loan funding for housebuilders/developers, its SME residential developer focused equity investment platform (Housing Growth Partnership in joint venture with Homes England), its ambitious in‑house private rental sector business (Lloyds Living) and its investment in housing via its position as the largest UK mortgage lender.

Shareholders:

- The need to create value for shareholders.

Outcome

Following its incorporation, MADE Partnership LLP has:

- been selected to support Cheshire East Council to deliver its vision for the 1,500‑home Handforth Garden Village;

- started work with Tameside MBC to deliver Godley Green Garden Village, with the potential to bring 2,150 much needed homes to the area; and

- won Deal of the Year in the 2025 RESI Awards.