Hays plc – Annual report – 30 June 2024

Industry: support services

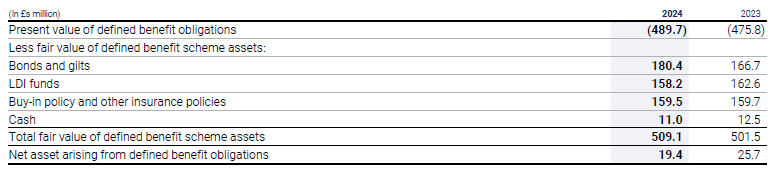

23 Retirement benefit surplus (extract)

The net amount included in the Consolidated Balance Sheet arising from the Group’s obligations in respect of its defined benefit pension schemes is as follows:

The Trustee Board is responsible for determining the Hays Pension Scheme’s investment strategy, after taking advice from the Scheme’s investment advisor Mercer Limited. The investment objective for the Trustee of the Scheme is to maintain a portfolio of suitable assets of appropriate liquidity which will generate investment returns to meet, together with future contributions, the benefits of the defined benefit scheme as they fall due. The current strategy is to hold investments that share characteristics with the long-term liabilities of the Scheme. The majority of assets are invested in a Liability Driven Investments (LDI) portfolio and corporate bonds and gilts. The Scheme also holds a bulk purchasing annuity policy (buy-in) contract with Canada Life Limited in respect of ensuring all future payments to existing pensioners of the Hays defined benefit Scheme as at 31 December 2017. The Scheme assets do not include any directly held shares issued by the Company or property occupied by the Company.

The fair value of financial instruments has been determined using the fair value hierarchy. Where such quoted prices are unavailable, the price of a recent transaction for an identical asset, adjusted if necessary, is used. Where quoted prices are not available and recent transactions of an identical asset on their own are either unavailable or not a good estimate of fair value, valuation techniques are employed using both observable market data and non-observable data.

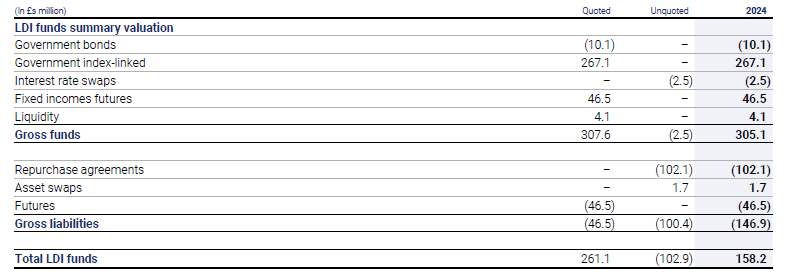

In relation to the LDI funds the valuations have been determined as follows:

- Repurchase agreements (where the Scheme has sold assets with the agreement to repurchase at a fixed date and price) are included in the Consolidated Financial Statements at the fair value of the repurchase price as a liability. The assets sold are reported at their fair value reflecting that the Scheme retains the risks and rewards of ownership of those assets;

- The fair value of the forward currency contracts is based on market forward exchange rates at the year-end and determined as the gain or loss that would arise if the outstanding contract was matched at the year-end with an equal and opposite contract; and

- Swaps represent current value of future cash flows arising from the swap determined using discounted cash flow models and market data at the reporting date.

The analysis of the LDI funds included within the pension scheme assets is as follows:

The LDI portfolio is managed by Insight (a Bank of New York Melon company) under an active mandate and uses government bonds and derivative instruments (such as interest rate swaps, inflation swaps and gilt repurchase transactions) to hedge the impact of interest rate and inflation movements in relation to the long-term liabilities.

Under the Schemes’ LDI strategy, if interest rates fall, the value of LDI investments will rise to help match the increase in actuarial liabilities arising from the fall in discount rate. Similarly if interest rates rise, the LDI investments will fall in value, as will the liabilities because of the increase in the discount rate. The extent to which the liability interest rate and inflation risk is not fully matched by the LDI funds, represents the residual interest rate and inflation risk the Scheme remains exposed to.

In addition to the above risk, the LDI portfolio forms part of a diversified investment portfolio for the Scheme, with this diversification seeking to reduce investment risk.

The Scheme is subject to direct credit risk because it invests in segregated mandates with the LDI portfolio. Credit risk arising on bonds held directly within the LDI portfolio is mitigated by investing mostly in government bonds where the credit risk is minimal.

Credit risk arising on the derivatives held in the LDI mandate depends on whether the derivative is exchange traded or over the counter (OTC). OTC derivative contracts are not guaranteed by any regulated exchange and therefore the Scheme is subject to risk of failure of the counterparty. The credit risk for OTC swaps held in the LDI portfolio is reduced by collateral arrangements.