Auckland International Airport Limited – Annual report – 30 June 2025

Industry: transport

2. Summary of material accounting policies (extract)

(h) Investment properties

Investment properties are properties held by the group to earn rental income (including property being constructed or developed for future use as investment property). Land held for a currently undetermined future use is classified as investment property.

Investment properties are measured initially at cost and then, subsequent to that initial measurement, are stated at fair value. To determine fair value, the group commissions investment property valuations at least annually by independent valuers. Gains or losses arising from changes in the fair values of investment properties are recognised in the income statement.

If the fair value of investment property under construction cannot be reliably determined but it is expected that the fair value of the property can be reliably determined when construction is complete, then investment property under construction will be measured at cost until either its fair value can be reliably determined or construction is complete.

Transfers are made to investment property when there is a change in use. This may be evidenced by the ending of owner occupation, commencement of an operating lease to another party, or commencement of construction or development for future use as investment property.

A property transfer from investment property to property, plant and equipment or inventory has a deemed cost for subsequent accounting at its fair value at the date of change in use.

If an item of property, plant and equipment becomes an investment property, the group accounts for such property as an investment property only subsequent to the date of change in use.

Investment properties where the group acts as a lessor are leased to tenants under operating leases with rentals payable monthly. Lease payments for some contracts include CPI increases, sales-based concession fees and other adjustments to rentals, with any credit risk being managed in the same way as described for property, plant and equipment leased assets (refer to note 2(g)).

Lease incentives are initially recognised at the value of the incentive, and amortised over the term of the lease. Other lease receivables may arise when fixed future retail or rental revenue increases are recognised on a straight-line basis over the term of the lease (refer to note 2(m)). The group assesses lease incentives and receivables for impairment at each reporting date and recognises impairment losses as prescribed by NZ IFRS 9.

3. Significant accounting judgements, estimates and assumptions (extract)

(a) Fair value of investment property

Changes to market conditions or to assumptions made in the estimation of fair value may result in changes to the fair value of investment property. The carrying value of investment property and the valuation methodology are disclosed in note 12.

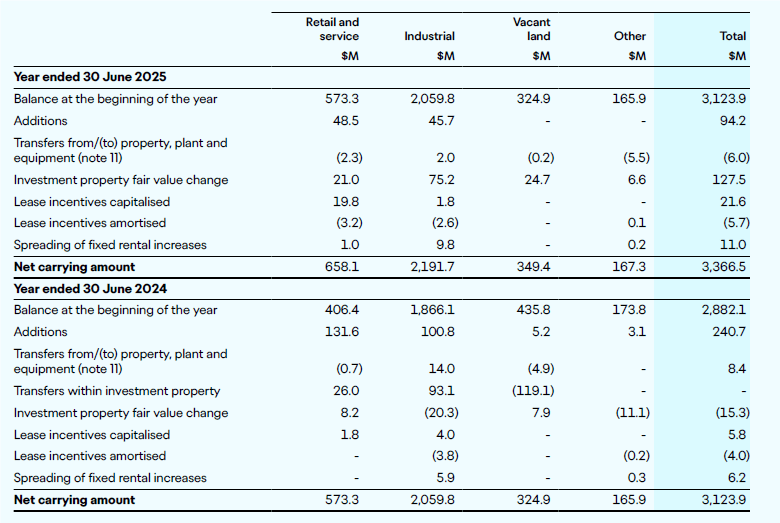

12. Investment properties

The table below summarises the movements in fair value of investment properties:

Additions for the year ended 30 June 2025 include capitalised interest of $4.4 million (2024: $9.7 million).

The group’s investment properties are all categorised as Level 3 in the fair value hierarchy, as described in note 2(e). During the year, there were no transfers of investment property between levels of the fair value hierarchy.

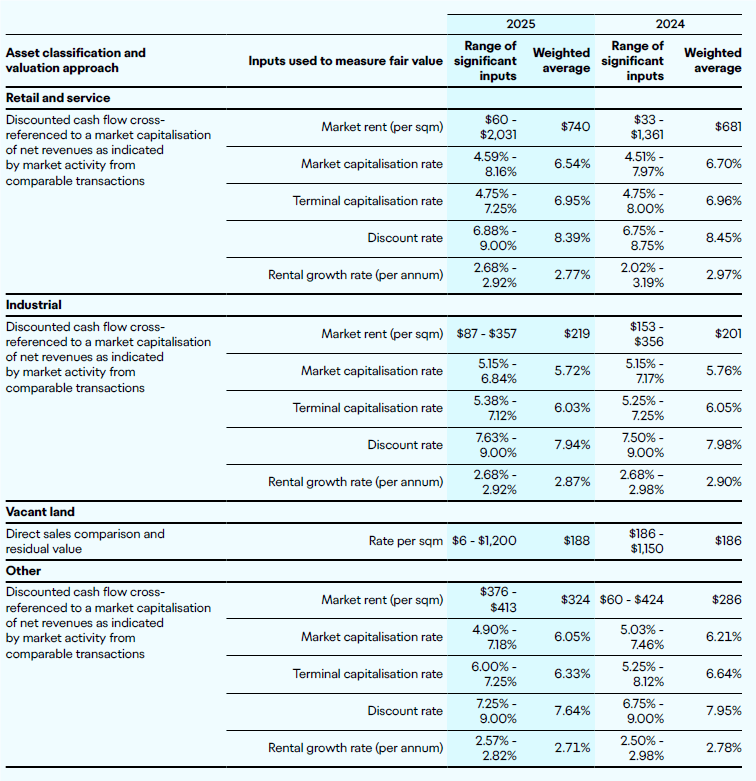

The basis of valuation is market value, based on each property’s highest and best use. The valuation methodologies used were a direct sales comparison or a direct capitalisation of rental income, using market comparisons of capitalisation rates, supported by a discounted cash flow approach. Investment property being constructed will be measured at cost until it is sufficiently advanced to be valued. Further details of the valuation methodologies and sensitivities are included in note 11(c). The valuation methodologies are consistent with prior years.

All valuations have been reviewed by management, which have determined the valuations to be appropriate as at 30 June 2025.

The principal assumptions used in establishing the valuations were as follows:

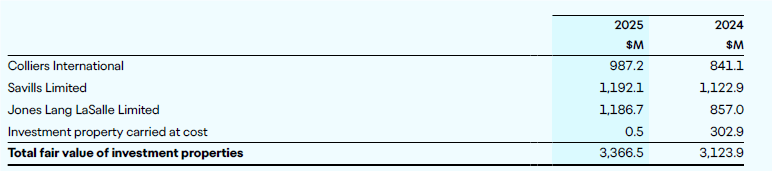

The fair value of investment properties valued by each independent registered valuer is outlined below:

The investment properties assigned to valuers are rotated across the portfolio every three years, with the most recent rotation occurring in June 2025. All valuers are registered valuers and industry specialists in valuing the above types of investment properties.

The table below summarises income and expenses related to investment properties:

The following categories of investment property are leased to tenants:

- Retail and service carried at $658.1 million (30 June 2024: $573.3 million);

- Industrial carried at $2,191.7 million (30 June 2024: $2,059.8 million); and

- Other investment property carried at $167.3 million (30 June 2024: $165.9 million).

The above values include the land associated with these properties.

21. Commitments

(a) Property, plant and equipment

The group had contractual obligations to purchase or develop property, plant and equipment for $1,113.4 million at 30 June 2025 (2024: $439.9 million). These include works associated with the runway, aprons, terminals and landside projects.

(b) Investment property

The group had contractual obligations to either purchase, develop, repair or maintain investment properties for $188.0 million at 30 June 2025 (2024: $120.9 million).

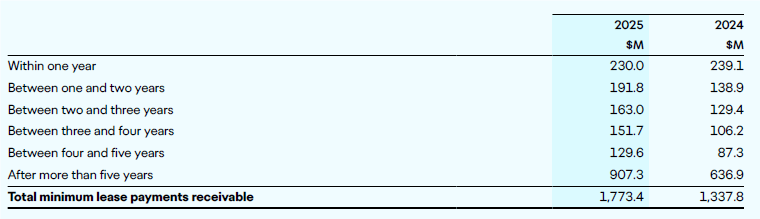

(c) Operating lease receivable – group as lessor

The group has commercial properties owned by the company that produce rental income and retail concession agreements that produce retail income.

These non-cancellable leases have remaining terms of between one month and 26 years (2024: one month and 27 years). Most leases with an initial period more than three years include a clause to enable upward revision of the rental charge on contractual rent review dates according to prevailing market conditions.

A very small minority can be revised downwards under normal trading conditions.

Future minimum rental and retail income receivable under non-cancellable operating leases as at 30 June are as follows:

2. Summary of material accounting policies (extract)

(m) Revenue recognition (extract)

Retail and rental income

Retail concession fees are recognised as revenue on an accrual basis based on the turnover of the concessionaires and in accordance with the related agreements. Rent abatements are recognised as an offset to revenue as negative variable lease payments when the group has an obligation to adjust fixed rent in response to significant reductions in passenger numbers or similar material adverse change.

Fixed retail and rental income increases are recognised as revenue on a straight-line basis over the term of the leases, which may result in lease receivable balances. The group assesses lease receivable balances for impairment at each reporting period (refer note 2(h)).

5. Profit for the year (extract)

1 The variable lease payments have been restated in the prior comparative year to reflect retail income that is dependent on passenger volumes.