Associated British Foods plc – Annual report – 13 September 2025

Industry: food and drink, retail

RESPONSIBILITY (extract)

Carbon and climate

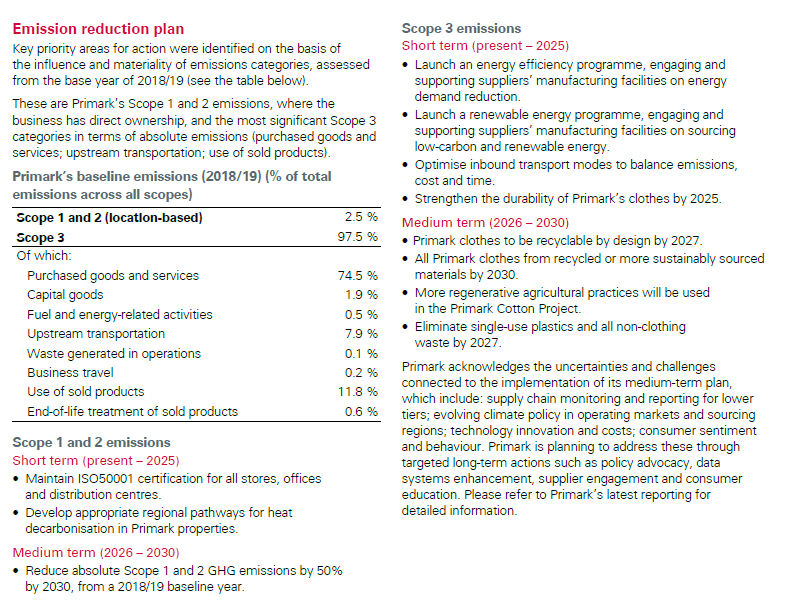

As a Group, we have an ambition to achieve net zero by 2050 or sooner. Beyond that broad ambition, we do not set groupwide climate-related plans or commitments. In line with our devolved business model, our businesses set plans and commitments appropriate to their operations and supply chains. Several of our businesses have set their own GHG emission reduction commitments.

ABF Sugar, Primark and Twinings Ovaltine each have specific public commitments for reducing their GHG emissions. The reduction targets for these businesses have been validated by the Science Based Targets initiative (SBTi), ensuring they align with the latest climate science. ABF Sugar, Primark and Twinings Ovaltine have published transition plans detailing their strategies for achieving these goals. Achieving our ambition of net zero across the Group will depend on a number of factors that are beyond our control, however, we will aim to deliver on this objective in our businesses while balancing environmental and financial impacts.

As climate-related disclosure expectations continue to evolve, our businesses are also preparing to meet emerging regulatory requirements alongside our Group-level TCFD statement. This includes mandatory reporting under Australia’s new Climate-Related Financial Disclosure regime, which came into effect on 1 January 2025.

Energy and renewables

We remain focused on energy efficiency and transitioning to renewable energy where viable. This year our businesses consumed 18,459△ gigawatt hours (GWh) of energy in our operations, which is an 11% decrease compared with last year, largely due to lower production volumes in Sugar and increased efficiencies in our factories.

Of this total energy, 54%△ was derived from renewable sources, predominantly biomass fuels from by-products generated from production processes. Of the renewable energy we generate, 84% comes from bagasse, the plant-based fibre that remains after the extraction of juice from the crushed stalks of sugar cane. Some renewable energy is also derived from the anaerobic digestion of a range of waste materials.

This year 37% of the electricity we bought came from renewable sources, up from 31% last year, with the majority coming from the UK and European renewable energy markets. Some of our businesses also generate and use renewable electricity from site-based solar panels.

Several of our businesses export surplus energy back into national grids. During 2025, 795GWh of energy generated by our sites was exported, with ABF Sugar contributing 95%.

For more examples of energy efficiency actions, see our website.

Scope 1 and 2 GHG emissions

Our Scope 1 and 2 (market-based) GHG emissions decreased by 8% this year, from 2,627kt to 2,410kt△ of CO2e.

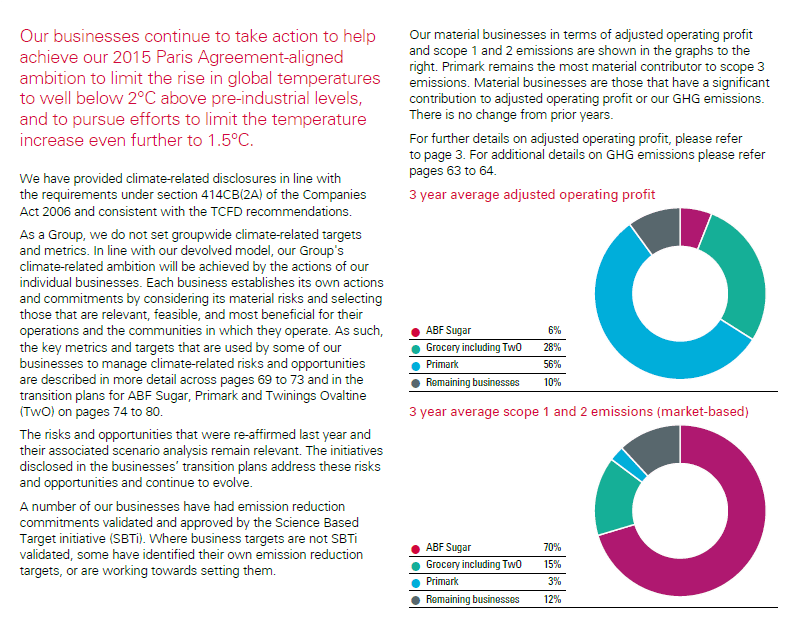

Our Sugar segment is the most significant contributor of Scope 1 and 2 (market-based) GHG emissions within the Group, at 72%. As a result, decreasing the carbon emissions from our Sugar businesses continues to be a priority for the Group.

In 2025, Sugar’s Scope 1 and 2 (market-based) GHG emissions decreased by 9% compared to the previous year and by 23% against their 2018 baseline by continuously improving how efficiently it produces sugar, investing in new technology, innovating to use less energy and fuel-switching to lower-emission sources.

Our Retail and Grocery segments have also reduced their Scope 1 and 2 (market-based) emissions compared with last year, by 39% and 9% respectively. These reductions were driven by reduced energy consumption and increased use of renewable energy sources.

* Prior year numbers have been restated to reflect the disposal of AB Sugar China, disposed of in 2024. The adjustment ensures comparability and accuracy in reporting the groups continuing operations.

Group priority

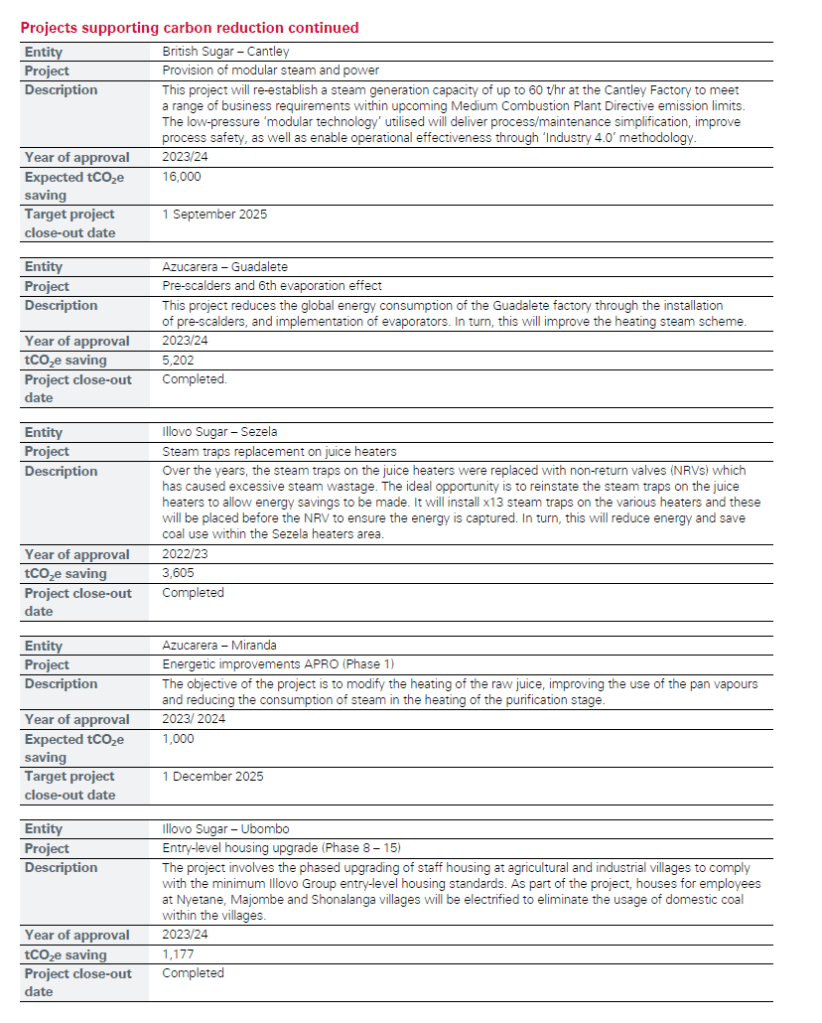

British Sugar decarbonising its operations

British Sugar, the largest contributor to the Group’s Scope 1 GHG emissions at 38%, has made significant investment across its sites to reduce GHG emissions. From its 2018 baseline year through to 2025, British Sugar has invested approximately £134m in various initiatives, resulting in a cumulative reduction of above 160kt of CO2e.

Key initiatives include the energy reduction scheme at its Wissington site, which reduced its annual steam usage by 25%, the recent installation of the Cantley site’s new combined heat and power (CHP) plant, and ongoing improvements in pulp pressing processes across multiple sites. Additionally, British Sugar is improving factory performance and efficiency by upgrading heaters, evaporators and dryers to save energy and reduce coal and gas consumption. In 2025, British Sugar eliminated coal usage in its CHP plants and animal feed combustion operations through fuel switching investments. These efforts have contributed substantially to reducing Scope 1 emissions.

Looking ahead, British Sugar plans to continue its decarbonisation strategy through projects which include a new diffusion heating configuration and evaporator station optimisation at Newark, an animal feed steam drying plant at Wissington and resin separation plant improvements.

Group priority

Scope 3 GHG emissions

Understanding our Group GHG emissions will be an important step towards achieving our ambition to meet net zero by 2050. At a Group level, we are supporting the divisions in the process of calculating their material Scope 3 GHG emissions, which will help us identify where to focus our priorities. Most of our divisions have either published or are in the process of calculating their Scope 3 GHG emissions from across their value chains.

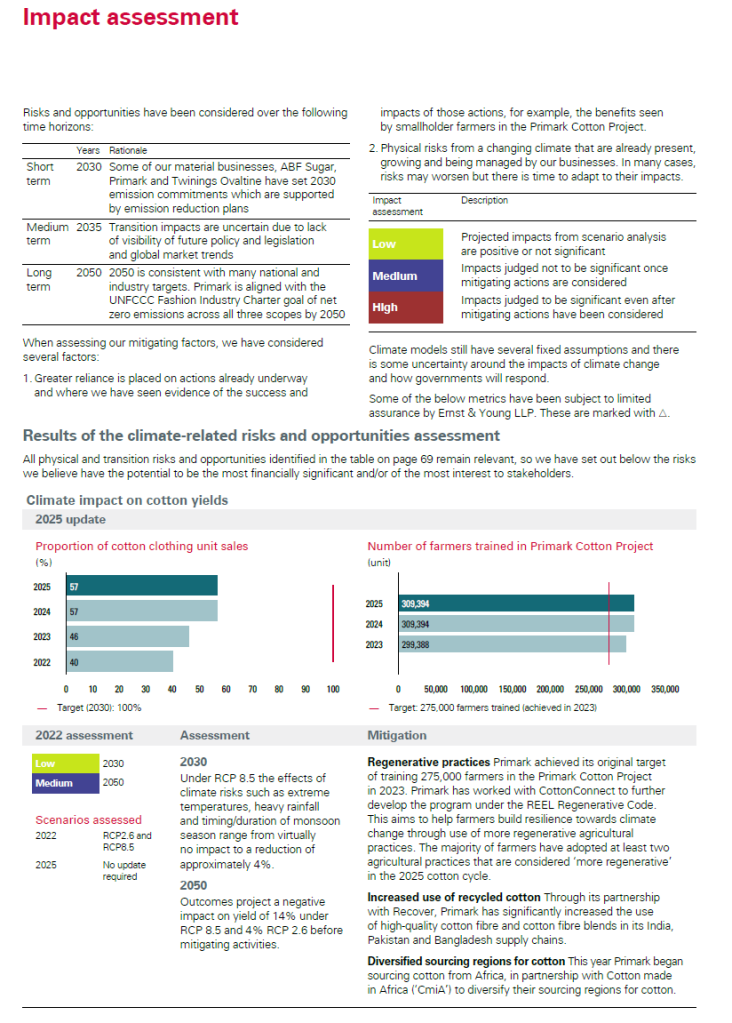

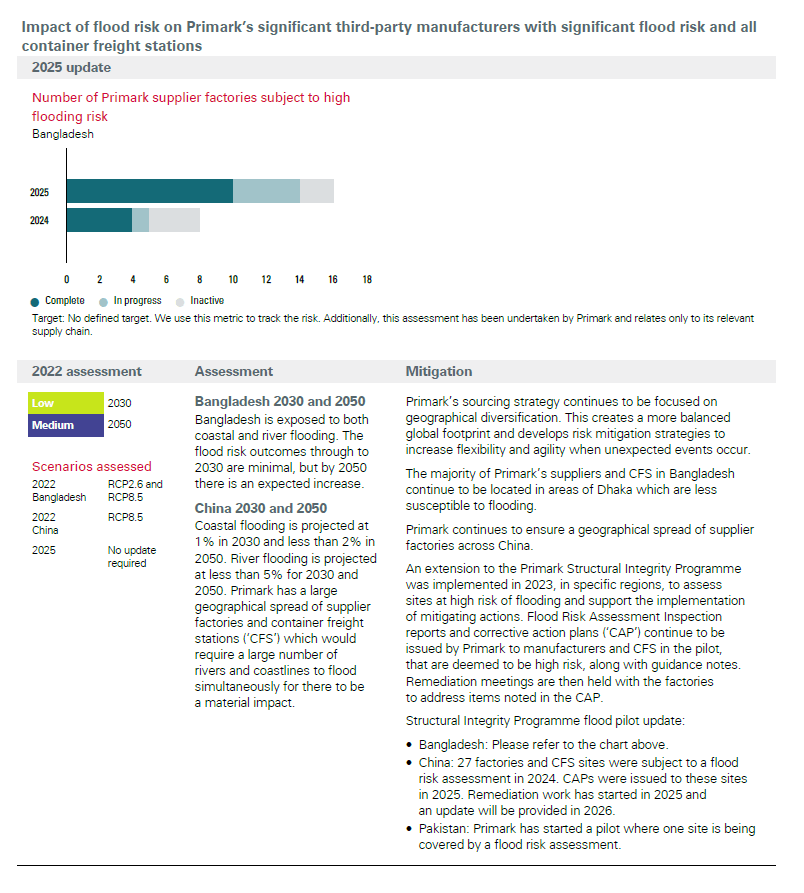

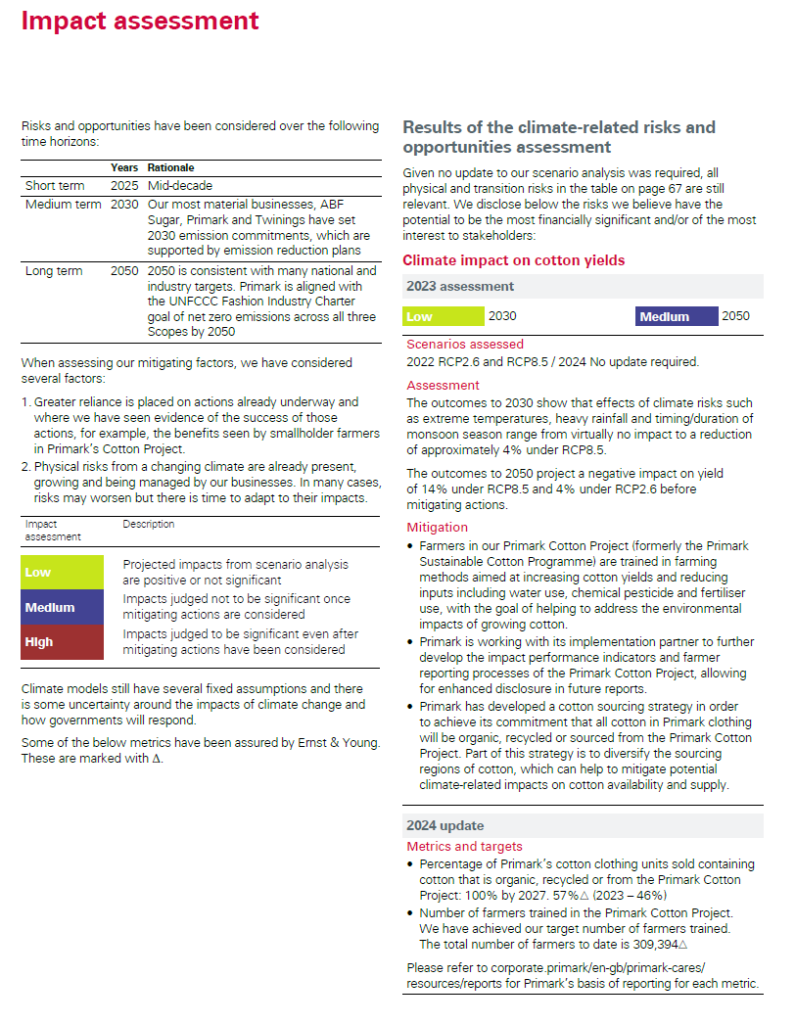

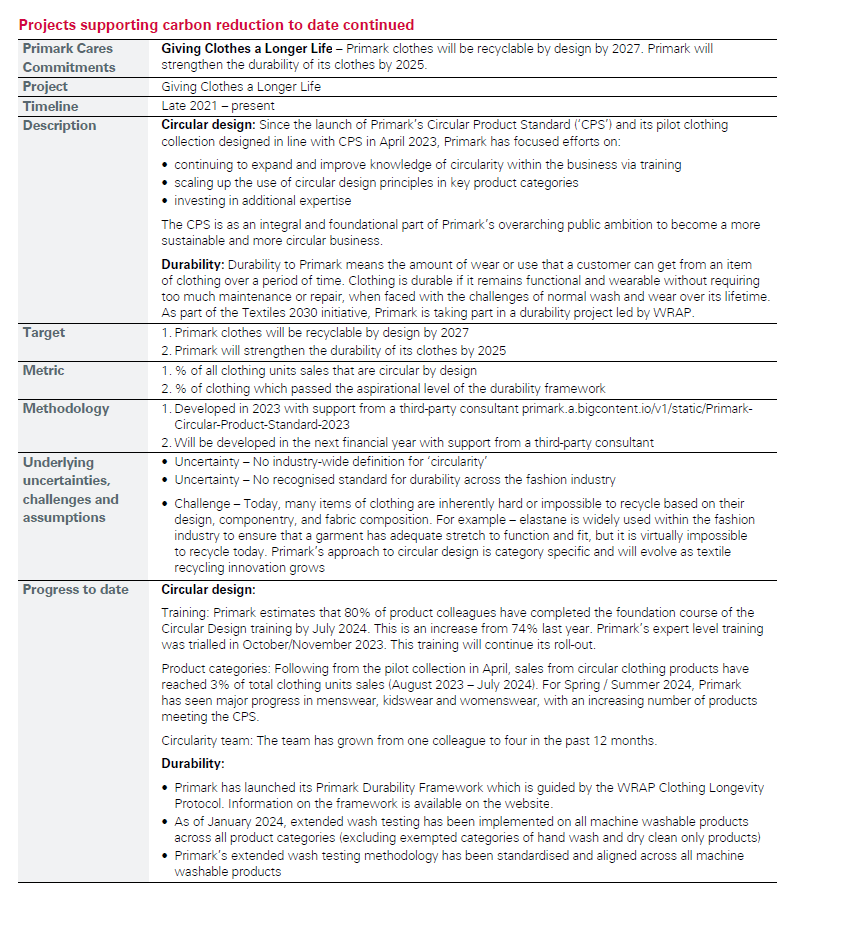

Primark first completed this process in 2021 and this year reported 5,993kt of CO2e for its Scope 3 emissions, which is a 3% decrease compared with 2024. This represents a 4% decrease against its 2019 baseline. These reductions were achieved through investments in its Environmental Sustainability team, in supplier factory efficiency programmes aimed at supporting GHG emission reductions through targeted training, upskilling, and energy-saving projects and the increased use of primary data. Primark also supports suppliers in switching to renewable energy and requires its key suppliers to set their own carbon reduction targets.

For more information on this topic see our website.

We calculate and disclose our Scope 1 and 2 GHG emissions based on the WRI/WBCSD GHG Protocol Corporate Accounting and Reporting Standard Revised Edition. We use carbon emission

factors published by the UK Government in July 2024, other internationally recognised sources and bespoke factors based on laboratory calculations at selected locations. Scope 2 market-based emissions have been calculated in accordance with the GHG Protocol Scope 2 Guidance on procured renewable energy. Our energy consumption is calculated using country-specific conversion factors from physical quantities to kWh to provide an accurate representation of our energy consumption.

The Group data in this report on our environmental and safety KPIs covers the period, 1 August 2024 to 31 July 2025, except for Primark selling space, number of countries of operation and employee numbers, which is disclosed in respect of the financial year.

This is different from the period in respect of which the Directors’ Report is prepared. Where indicated the information for this period is externally assured and allows for like-for-like comparison with previous years.

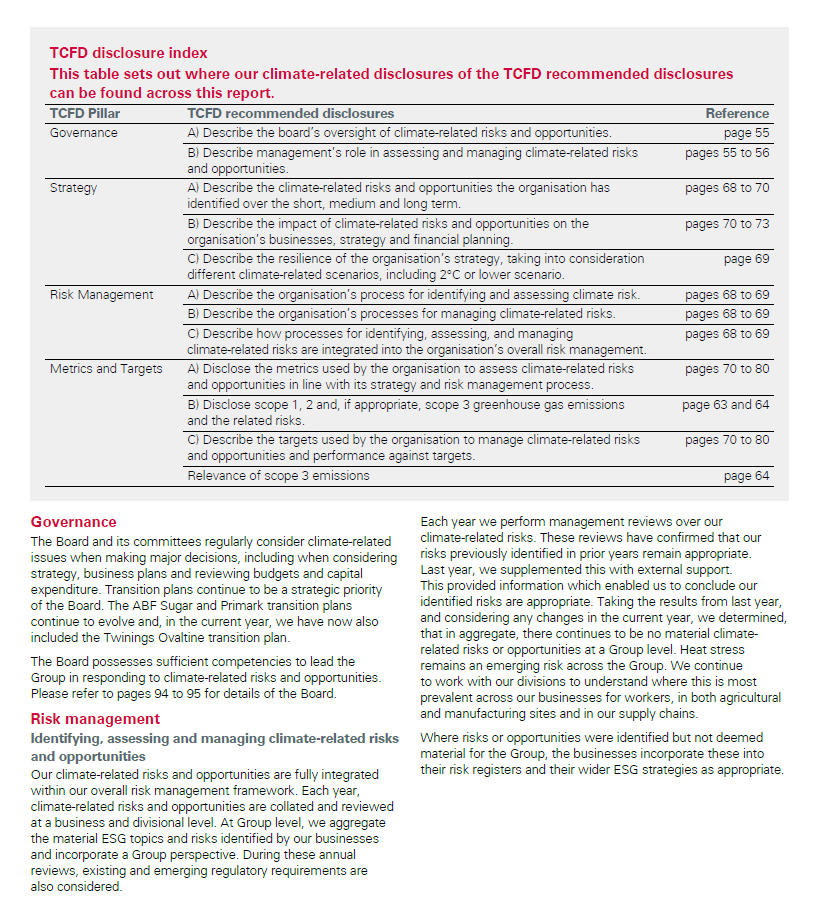

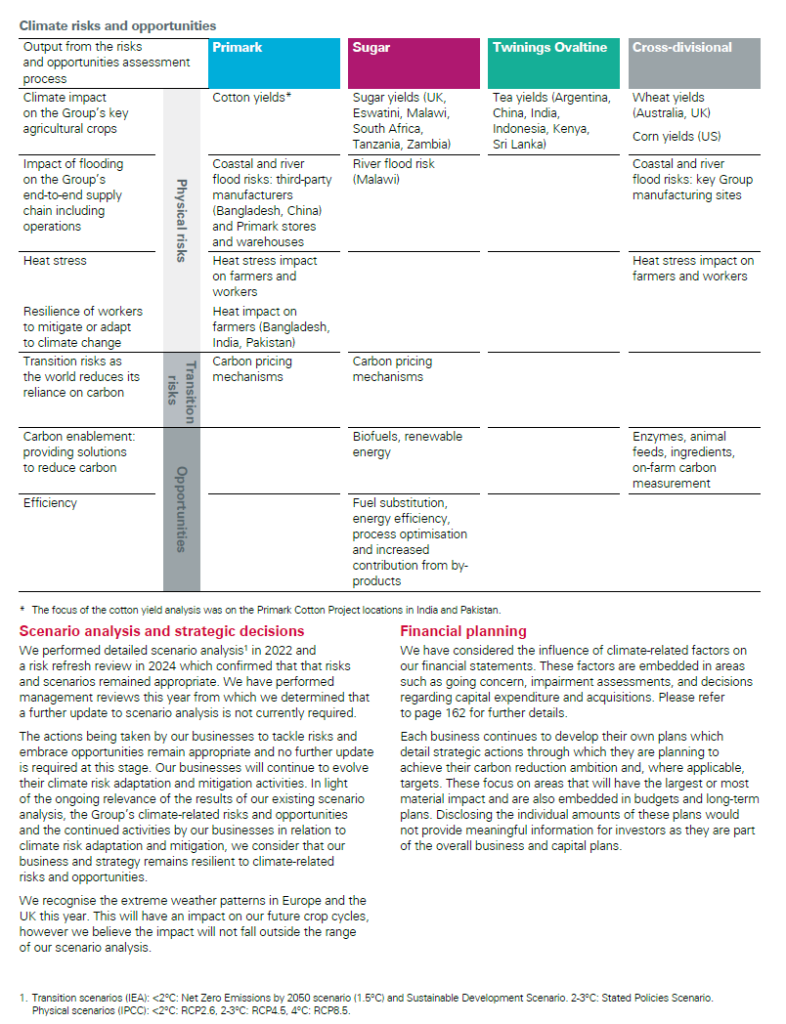

Climate-related Financial Disclosures (‘TCFD’) (page 67)

Extracts pages 55-56