Swire Properties Limited – Annual report – 31 December 2022

Industry: real estate

1. Changes in Accounting Policies and Disclosures (extract)

(c) Change in accounting policy on lessor forgiveness of lease payments

In October 2022, the IASB finalised the agenda decision approved by the IFRS Interpretation Committee (‘IFRS IC’) on “Lessor Forgiveness of Lease Payments (IFRS 9 and IFRS 16)”. The agenda decision addresses the accounting from the perspective of the lessor, and in particular:

- how the expected credit loss (‘ECL’) model in IFRS 9 should be applied to the operating lease receivable when the lessor expects to forgive payments due from the lessee under the lease contract before the rent concession is granted; and

- whether to apply the derecognition requirements in IFRS 9 or the lease modification requirements in IFRS 16 when accounting for the rent concession.

The IFRS IC concluded that in reporting periods before the forgiveness of lease payments have been granted, the lessor should measure the ECL on operating lease receivables on a probability-weighted basis, by evaluating a range of possible outcomes, including its expectation of forgiving lease payments that have been recognised as an operating lease receivable. This is on the assumption that there is reasonable and supportable information, that is available without undue cost or effort, and that the expectation of forgiving the lease payments reflects a potential cash shortfall which should be taken into account in the ECL measurement.

In previous years, all the rent concession granted to tenants were treated as lease modifications under HKFRS 16 and were amortised over the remaining periods of the leases.

The Group has changed its accounting policy having regard to the IASB agenda decision. In applying the requirements in HKFRS 9, the Group re-measures the ECL on its operating lease receivables immediately prior to the date the lease payments are forgiven, with any changes being recognised as rental outgoings in the consolidated statement of profit or loss. Once the lease payments are forgiven, the Group derecognises the operating lease receivable, including any associated ECL allowance. Lease payment forgiven that are not associated with operating lease receivables are recognised as lease modifications under HKFRS 16.

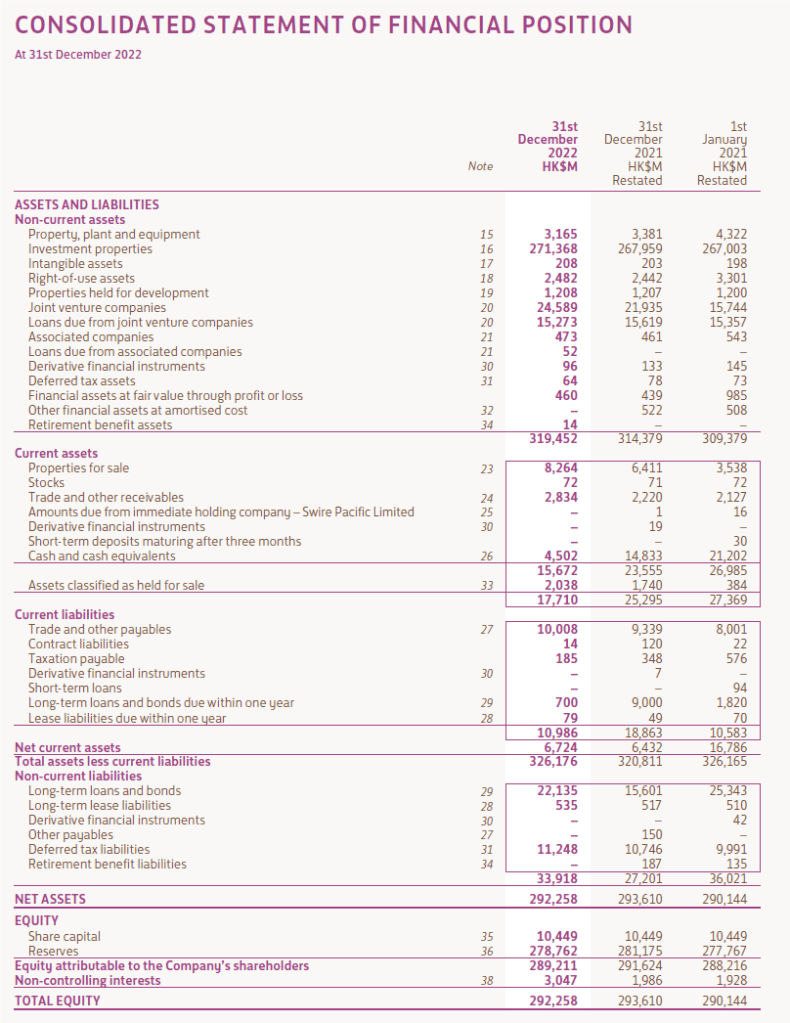

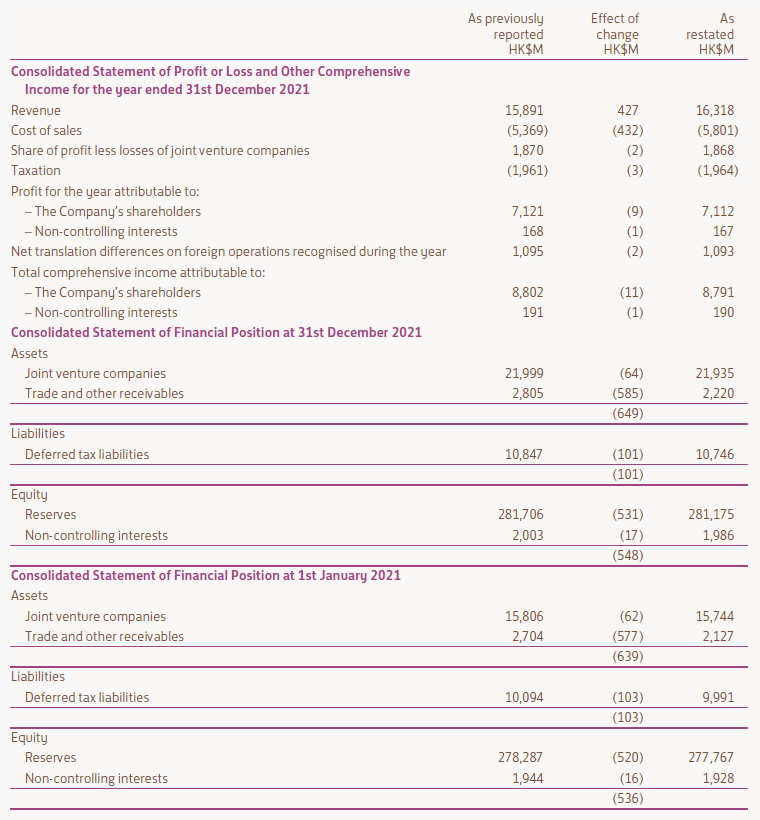

The change in accounting policy has been applied retrospectively by restating the balances at 31st December 2021 and 1st January 2021, and the results for the year ended 31st December 2021:

The change in accounting policy affected the following items in the consolidated statement of profit or loss and other comprehensive income for the year ended 31st December 2022 and the consolidated statement of financial position at 31st December 2022: