ASML Holdings N.V. – Half year report – 1 July 2018

Industry: technology, computers

- Summary of Significant Accounting Policies (extract 1)

The accounting policies adopted in the preparation of the Consolidated Condensed Interim Financial Statements are consistent with those applied in the preparation of the Consolidated Financial Statements 2017, except for income tax expense which is recognized based on management’s best estimate of the annual income tax rate for the full financial year.

A number of new standards became applicable for the current reporting period and we had to change our accounting policies and make (retrospective) adjustments as a result of adopting the following standards:

- IFRS 9 “Financial Instruments”;

- IFRS 15 “Revenue from Contracts with Customers”; and

- IFRS 16 “Leases”.

The impact of the adoption of these standards and the new accounting policies is disclosed below. We believe that the effect of all other standards (not yet) effective and (not yet) adopted by the EU is not expected to be material.

- Summary of Significant Accounting Policies (extract 2)

Revenue from Contracts with Customers

IFRS 15 “Revenue from Contracts with Customers” was issued in May 2014 and has been endorsed by the EU on September 22, 2016. The standard is a joint project of the FASB and the IASB, to clarify the principles for recognizing revenue and to develop a common revenue standard for US GAAP and IFRS that would:

- Remove inconsistencies and weaknesses in previous revenue requirements;

- Provide a more robust framework for addressing revenue issues;

- Improve comparability of revenue recognition practices across entities, industries, jurisdictions and capital markets;

- Provide more useful information to users of financial statements through improved disclosure requirements; and

- Simplify the preparation of financial statements by reducing the number of requirements to which an entity must refer.

We have closely assessed the impact of adopting IFRS 15 on our Consolidated Condensed Interim Financial Statements by assessing all contracts that have an impact on net system sales and net service and field option sales over 2017. We have finalized our assessment of all contracts based on which we have adopted IFRS 15 “Revenue from Contracts with Customers” with a date of the initial application of January 1, 2018. We have selected full retrospective adoption and therefore restate all years presented in our Consolidated Financial Statements upon adoption. As a result, we have changed our accounting policy for revenue recognition as detailed below.

We applied IFRS 15 for the years ended December 31, 2017 retrospectively using the practical expedients in paragraph IFRS 15.C5, under which we:

- Do not restate contracts that begin and are completed in the same annual or semi-annual reporting period;

- Used the transaction price at the date the contract was completed rather than estimating variable consideration amounts in the comparative reporting periods;

- Do not disclose the amount of consideration allocated to the remaining performance obligations or an explanation of when we expect to recognize that amount as revenue for all reporting periods presented before the date of the initial application – i.e. January 1, 2018; and

- Reflect the aggregate effect of all modifications that occurred before January 1, 2017 when identifying the performance obligations, determining the transaction price and allocating the transaction price to the satisfied and unsatisfied performance obligations.

Applying these practical expedients is not expected to have a significant impact on our adjusted semi-annual financial results as our expectation of the impact would be limited to certain shifts of revenue recognition between periods due to not using the hindsight allowed by these practical expedients.

The details of the significant changes and quantitative impact of the changes are disclosed below:

A. Allocation of consideration based on stand-alone selling price

We changed from allocating the consideration of a contract to the elements of the contract using the relative selling price of these elements in accordance with IAS 18 to allocating the consideration of a contract based on stand-alone selling prices determined using the adjusted market assessment approach in accordance with IFRS 15. As a result, we consider customer discounts and cash credits, within volume purchase agreements, a reduction of the transaction price. Consequently, we allocate these customer discounts and cash credits ratably to the performance obligations based on the stand-alone selling price.

As we have very limited sales on a stand-alone basis we have to make estimates to determine our stand-alone selling prices. For this we selected the adjusted market assessment approach. This estimate requires our judgment as we mainly enter into bundled arrangements and we sell specialized goods and services. Furthermore, we have no insight into the stand-alone selling prices of our competitors for comparable products and services. Therefore, we considered our pricing policies and practices, which are based on the value we provide to our customers. Our internal pricing policies result in a list price, which is for the majority of products only determined and set when the products or services are introduced. We conclude that these list prices generally do not reflect the stand-alone selling prices over the lifetime of the related product or services.

To determine the stand-alone selling prices for our products and services we used data of bundled arrangements over the last one to three years and derived the price for which each system model would be sold, on a stand-alone basis, from this data. We used the same relative step-down from the list price for options and services that are sold together with the system. For other services we used list prices, as these contracts typically have duration of one year and prices are updated periodically. For options that are not sold as part of a system for systems already installed at the customer, we used the contract data over the last three years and derived the price for which these options would be sold, on a stand-alone basis, from this data.

B. Field upgrades

Transfer of control of field upgrades and options, that require significant installation efforts, was previously upon customer acceptance of the upgraded system. The new over-time revenue recognition requirement, in IFRS 15.35(b) performance that enhances an asset the customer controls, results in revenue for these field upgrades and options to be recognized over time during the period of installation.

C. Installation

Installation revenue was previously recognized upon completion and customer acceptance. It has been determined, in accordance with IFRS 15.35, that the customer simultaneously consumes and receives the benefits provided by the performance of the installation. As a result, transfer of control takes place over the period of installation from delivery through customer acceptance, measured on a straight-line basis, as our performance is satisfied evenly over this period of time.

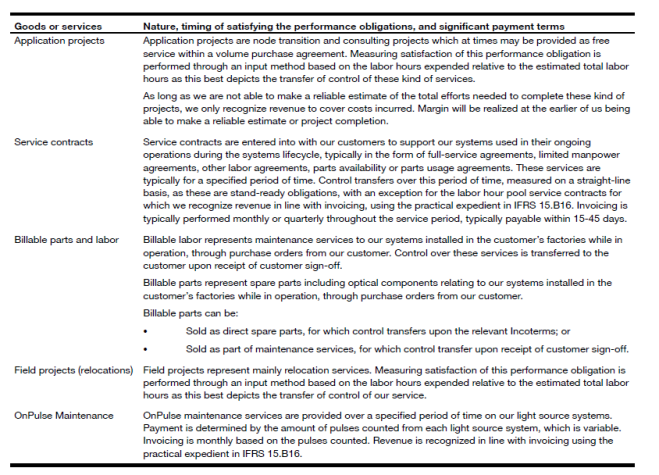

D. Applications projects and Field projects (relocations)

Applications and Field project revenue was previously recognized upon completion and customer acceptance. It has been determined in accordance with IFRS 15.35, that the customer simultaneously consumes and receives the benefits provided by the performance of our services. As a result, the transfer of control occurs throughout the service period.

E. Bill-and-hold transactions

Previously, in order to recognize revenue for a bill-and-hold transaction, our policy included a requirement for a fixed schedule of delivery, as well as the requirement that the buyer must have had a substantial business purpose for requesting the bill-and-hold transaction. Whereas IAS 18 did not contain specific guidance on bill-and-hold arrangements, IFRS 15 does contain specific application guidance on the accounting for bill-and-hold arrangements. In accordance with IFRS 15.B81, we no longer require a fixed scheduled delivery and a customer’s explicit request is no longer required.

F. Options to buy as a material right

Options to buy goods or services in addition to the purchase commitment were previously not assessed as a separate element, but are now assessed in order to determine if these options provide a material right to the customer they would not have received if they had not entered into the contract. Each option to buy additional goods or services provided at a discount from the stand-alone selling price is considered a material right and will be recognized as revenues in accordance with IFRS 15.B40.

G. Contract assets and liabilities

The contract assets primarily relate to our rights to a consideration for goods or services delivered but not invoiced at the reporting date. The contract assets are transferred to the receivables when invoiced and the rights become unconditional. The contract liabilities primarily relate to down payments, received for systems to be delivered, as well as deferred revenue from system shipments, based on the allocation of the consideration to the related performance obligations in the contract. This balance is mainly consisting of extended warranties, installation and other free goods or services provided as part of a volume purchase agreement.

The majority of our customer contracts contain both asset and liability positions. At the end of each reporting period, these positions are netted on a contract basis and presented as either an asset or a liability in the financial statements. Consequently, a contract balance can change between periods from a net contract asset balance to a net contract liability balance in the balance sheet.

The following tables summarize the impacts of the adoption of IFRS 15 on our Consolidated Statements of Operations and Comprehensive Income for the six-month period ended July 2, 2017:

- The calculation of diluted net income per ordinary share assumes the exercise of options issued under our stock option plans and the issuance of shares under our share plans for periods in which exercises or issuances would have a dilutive effect. The calculation of diluted net income per ordinary share does not assume exercise of such options or issuance of shares when such exercises or issuance would be anti-dilutive.

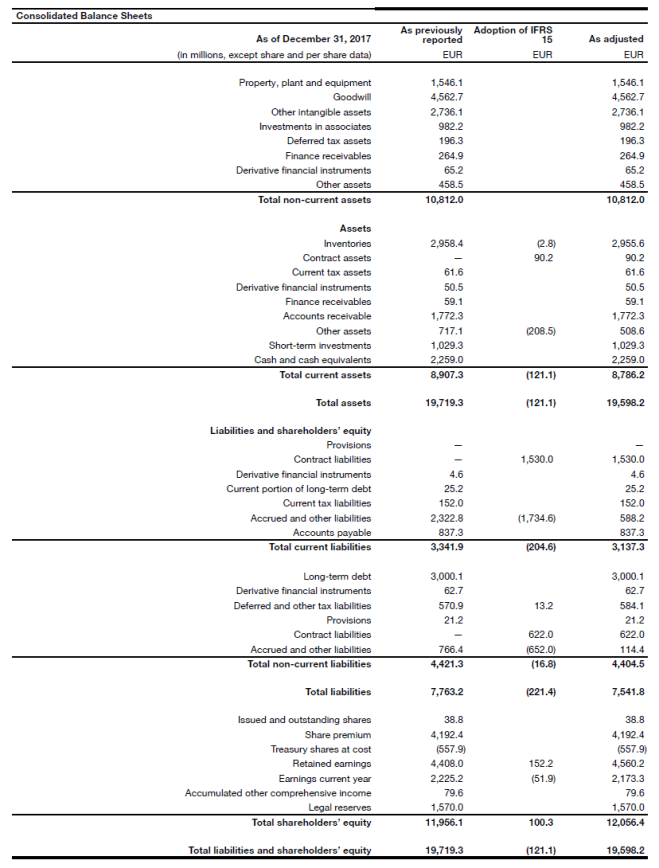

The following table summarizes the impacts of the adoption of IFRS 15 on our Consolidated Balance Sheets as of December 31, 2017:

The following tables summarize the impacts of the adoption of IFRS 15 on our Consolidated Statements of Cash flows for the six-month period ended July 2, 2017:

- For the six-month period ended July 2, 2017, depreciation and amortization includes EUR 159.4 million of depreciation of property, plant and equipment, EUR 196.8 million of amortization of intangible assets and EUR 2.1 million of amortization of underwriting commissions and discount related to the bonds and credit facility.

- For the six-month period ended July 2, 2017, an amount of EUR 19.1 million of the disposal of property, plant and equipment relates to noncash transfers to inventory. Since the transfers between inventory and property, plant and equipment are non-cash events, these are not reflected in this Consolidated Condensed Statement of Cash Flows.

- For the six-month period ended July 2, 2017, an amount of EUR 3.1 million of the additions in property, plant and equipment relates to non-cash transfers from inventory. Since the transfers between inventory and property, plant and equipment are non-cash events, these are not reflected in this Consolidated Condensed Statement of Cash Flows.

Accounting policy – Revenue From Contracts With Customers

We measure revenue based on the consideration specified in the contracts with our customers, adjusted for any significant financing components, and excluding any tax amounts collected on behalf of third parties. We recognize revenue when we satisfy a performance obligation by transferring control over a good or service to our customer. Taxes assessed by a governmental authority that are imposed on a specific revenue-producing transaction, that are collected by us from our customers, are excluded from revenue.

We bill our customers for, and recognize as net sales, any charges for shipping and handling costs. The related costs are recognized as cost of sales. For certain contracts and constructive obligations resulting from these arrangements, for which a loss is evident, we recognize the anticipated loss to the extent the costs of completing these contracts and constructive obligations exceed the amount of the contract price. When we satisfy these obligations, we utilize the related liability.

We generate revenue from the sale of integrated patterning solutions for the semiconductor industry, which mainly consist of systems, system related options and upgrades, holistic lithography solutions and customer services. The main portion of our net sales is derived from contractual arrangements with our customers that have multiple deliverables (performance obligations), which mainly include the sale of our systems, system related options, installation, training and extended and enhanced (optic) warranty.

The main portion of our system sales results from volume purchase agreements, in which we offer customers discounts in the normal course of sales negotiations. As part of these volume purchases agreements, we may also offer free goods or services and credits that can be used towards future purchases. Occasionally, systems, with the related extended and enhanced (optic) warranties, installation and training services, are ordered individually. Our system sales agreements do not include a general right of return.

For bundled packages, we account for individual goods and services, including the free or discounted goods or services, separately if they are distinct – i.e. if a product or service is separately identifiable from other items in the bundled package and if a customer can benefit from it on its own or with other resources that are readily available to the customer. The consideration paid for our performance obligations is typically fixed, unless specifically noted in the nature of the performance obligations. At times the total consideration of the contract can be dependent on the final volume of systems ordered by the customer. Payment is typically due 15-45 days after shipment or completion of the service unless described otherwise. The total consideration of the contract is allocated between all distinct performance obligations in the contract based on their stand-alone selling prices. The stand-alone selling prices are determined based on other stand-alone sales that are directly observable, when possible. However, for the majority of our performance obligations these are not available. If no directly observable evidence is available, the stand-alone selling price is estimated using the adjusted market assessment approach. These estimates are considered significant judgments.

Variable consideration is estimated at contract inception for each performance obligation, and subsequently updated each quarter, using either the expected value method or most likely amount method, whichever is determined to best predict the consideration to be collected from the customer. Variable consideration is only included in the transaction price if it is considered probable that a significant revenue reversal will not occur.

In certain scenarios when entering into a volume purchase agreement, free goods or services are provided directly or through a voucher that can be used on future contracts. Consideration from the contract will be allocated to these performance obligations and revenue recognized when control transfers based on the nature of the goods or service provided.

Options to buy goods or services in addition to the purchase commitment are assessed to determine if they provide a material right to the customer that they would not have received if they had not entered into this contract. Each option to buy additional goods or services provided at a discount from the stand-alone selling price is considered a material right. The discount offered from the stand-alone selling price will be allocated from the consideration of the other goods and services in the contract if it is determined the customer will exercise the option to buy, adjusted for the likelihood. Revenue will be recognized in line with the nature of the related goods or services. If it is subsequently determined the customer will not exercise the option to buy, or the option expires, revenue will be recognized.

Occasionally we may enter into a bill-and-hold transaction where we invoice a customer for a system that is ready for delivery but not shipped to the customer until a later date, based on customer’s request. Transfer of control is determined to have occurred only when there is a substantive reason for the arrangement, the system is separately identified as belonging to the customer, the good has been accepted by the customer and is ready for delivery, and we do not have the ability to direct the use of the system.