MTN Group Limited – Annual report – 31 December 2024

Industry: telecoms

1.5 Critical accounting judgements, estimates and assumptions (extract)

1.5.2 IHS Group fair value through other comprehensive income (FVOCI)

Significant judgement – investment classification

The Group has an economic interest in IHS Group of 25.66% (2023: 25.66%) comprising of ordinary shares. An investor is presumed to have significant influence over an investee when it owns 20% of the investee, unless it can be clearly demonstrated that this is not the case. According to IHS Group’s articles of association, while the Group owns more than 20% of the issued shares, the Group’s voting rights are limited to 20%. The Group is not entitled to appoint a Board member. The Group does not have any special information rights or access to strategic, financial or operational information beyond that available to other public shareholders.

As a result of these restrictions, the Group’s rights do not constitute significant influence to participate in the financial and operating policy decisions of IHS Group. Consequently, the Group accounts for its investment in IHS Group as an equity instrument held at fair value through other comprehensive income (FVOCI) (refer to note 7.2).

7 FINANCIAL RISK (extract)

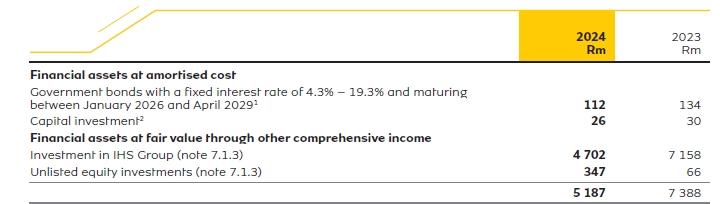

7.2 Investments

Investments consist of equity investments at FVOCI and financial assets at amortised cost, that are accounted for in accordance with the accounting policy disclosed in note 7.1.

1 Denominated in Nigerian naira.

2 Denominated in Ghanaian cedi.

7.1.3 Fair value estimation (extract)

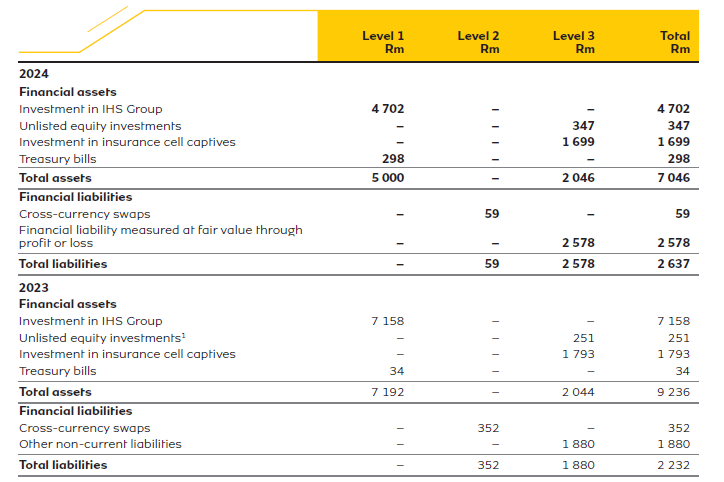

The following table presents the fair value measurement hierarchy of the Group’s assets and liabilities measured at fair value:

1 Includes assets directly associated with non-current assets held for sale, refer to note 9.4.2.

Valuation methods and assumptions (extract)

The following methods and assumptions were used to estimate the respective fair values:

IHS Group listed equity investment – The fair value of the investment is determined by reference to published price quotations on the New York Stock Exchange. The share price of IHS Group was US$2.92 (2023: US$4.60) on the last trading day of the year.

A fair value decrease (translated at average exchange rate) of R2 650 million (2023: R2 689 million) has been recognised for the year. On 13 March 2025, the IHS Group share price was US$3.71, equating to a increase in the fair value of R1 089 million subsequent to 31 December 2024.