Rolls-Royce Holdings plc – Annual report – 31 December 2022

Industry: aerospace

1 Accounting policies (extract)

Revisions to IFRS applicable in 2022

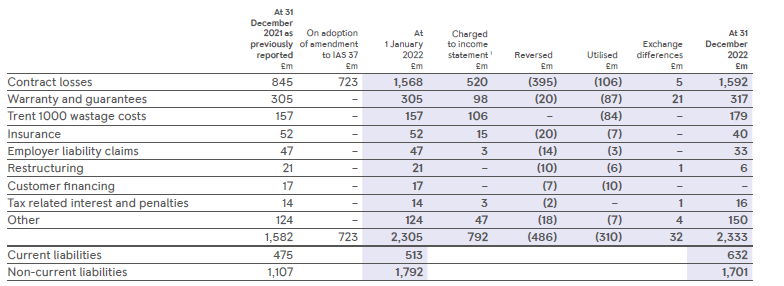

The Group adopted the amendment to IAS 37 Provisions, Contingent Liabilities and Contingent Assets for Onerous Contracts – Cost of Fulfilling a Contract on 1 January 2022. The amendment clarifies the meaning of ‘costs to fulfil a contract’, explaining that the direct cost of fulfilling a contract comprises the incremental costs of fulfilling that contract (for example, direct labour and materials) and also an allocation of other costs that relate directly to fulfilling contracts. As a result of the amendment, the Group now includes additional allocated costs when determining whether a contract is onerous and in the quantification of the provision recognised in the event of a contract being onerous. These additional allocated costs primarily relate to (a) fixed overheads in our operational areas that are incurred irrespective of manufacturing load, (b) fixed overheads of providing services, including engine health monitoring and IT costs, and (c) depreciation of spare engines that the Group owns are used to support the delivery of our contractual commitments to customers under LTSAs. The Group has assessed the impact of this amendment on its contracts and has included additional allocated costs that increased the total contract loss provision by £723m, as at 1 January 2022 (see note 21). All material elements impact Civil Aerospace contracts. Of this increase, £38m relates to current provisions and £685m to non-current provisions. A tax credit has not been recognised on the increase in the provision relating to the UK (see note 5 for details). As required by the transition arrangement in relation to the amendment, comparative information has not been restated. The cumulative effect of initially applying the amendment has been recognised as an adjustment to the opening balance of retained earnings as at 1 January 2022. It is estimated that the impact of the IAS 37 amendment has had a favourable immaterial impact on the 2022 income statement. Further information can be found in note 21.

There are no other new standards or interpretations issued by the IASB that had a significant impact on the Consolidated Financial Statements.

21 Provisions for liabilities and charges (extract)

1 The charge to the income statement includes £33m (2021: £32m) as a result of the unwinding of the discounting of provisions previously recognised

Contract losses

Provisions for contract losses are recorded when the direct costs to fulfil a contract are assessed as being greater than the expected revenue. As a result of the amendment to IAS 37 for Onerous Contracts, from 1 January 2022 provisions for contract losses have been measured on a fully costed basis resulting in a £723m increase of the total contract loss provision as at 1 January 2022 (see note 1 for details). During the year, additional contract losses for the Group of £520m have been recognised as a result of changes in future cost estimates, primarily in relation to LTSA shop visits, exchange rate movements and also includes £157m which arose from the sale of ITP Aero resulting in the recognition of additional costs which were previously eliminated on consolidation. Contract losses of £395m previously recognised have been reversed following improvements to cost estimates across various large engine programmes as a result of operational improvements and updates to the discount rate. The Group continues to monitor the contract loss provision for changes in the market and revises the provision as required. The value of the remaining contract loss provisions reflect, in each case, the single most likely outcome. The provisions are expected to be utilised over the term of the customer contracts, typically within 8 to 16 years.

5 Taxation (extract)

The Group has not recognised a deferred tax asset in respect of 2022 UK tax losses. This includes the impact of the IAS 37 amendment.