ArcelorMittal S.A. – Annual report – 31 December 2025

Industry: manufacturing

(millions of U.S. dollar, except share and per share data)

NOTE 1: ACCOUNTING PRINCIPLES (extract)

1.3 Use of judgment and estimates (extract)

Judgments and estimates made in assessing the impact of climate change and the transition to a low carbon economy

Assumptions in respect of climate change and the transition to a low carbon economy may impact the Company’s significant judgments and key estimates and result in material changes to financial results and the carrying values of certain assets and liabilities in future reporting periods. The main judgments and estimates made by ArcelorMittal when preparing the 2025 consolidated financial statements with respect to the expected effects of climate change and the transition to a low carbon economy are described below.

- Impairment of tangible and intangible assets, including goodwill: Value in use calculations for operations which apply the BF-BOF route include the impact of decarbonization at the level of cash flow projections when decarbonization is necessary to maintain the level of economic benefits expected to arise from the assets in their current condition considering the legal obligation of net zero for such operations. Accordingly the Company developed assumptions in determining related capital expenditures which reflect announced commitments and initiatives in place, costs associated with operating the new technologies which are expected to be deployed in the short to medium term, commodity prices and carbon emission costs on the basis of historical experience and expectations of future changes. This requires to assess the future development in supply, technology change, production changes and other important factors. For other operations, discount rates are increased to include a risk premium relative to the future estimated decarbonization cost. Due to economic developments, uncertainties over the pace of transition to low-emission technologies, political and environmental actions that will be taken to meet the carbon reduction goals, regulatory changes and emissions activity arising from climate-related matters, the Company’s assumptions used in the recoverable amount calculations, such as capital expenditure, carbon emission costs, level of public funding and other assumptions are inherently uncertain, which could result in significant changes to value in use calculations in future periods and affect impairment assessments.

- Decommissioning costs: Over the next ten years, the retirement of certain above-mentioned assets in the context of the transition to low-carbon steelmaking infrastructures may lead to certain decommissioning costs. The Company considered such costs in its value in use calculations but it has not recognized decommissioning provisions related to decarbonization as the obligating event has not occurred yet. Decommissioning cost estimates are based on the known regulatory and external environment. These cost estimates may change in the future including as a result of the transition to a lower carbon economy.

- Renewable power purchase agreements: The Company enters into power purchase agreements (“PPAs”), which provide for the physical delivery of renewable energy and enable ArcelorMittal to reduce its indirect emissions (Scope 2) related to energy purchases. The Company analyzes the accounting treatment for such contracts based on their relevant terms. When they do not comply either with the requirements of IFRS 10 for the existence of control or IFRS 11 for joint control over a company or regarding the existence of joint operation over an asset, IFRS 16 for the recognition of a lease, or with the definition of a derivative under IFRS 9, they are accounted for as an executory contract on the basis of the own use exemption when the relevant conditions are met (see note 9.4). Virtual PPAs including a cash settlement based on the difference between the contract price and the market price are recognized as financial instruments in accordance with IFRS 9.

Situation in Ukraine and collateral consequences

The Company’s operations in Ukraine consist of a steel plant, which produced 1.7 million tonnes of steel (mainly billets, rebars, wire rods, light sections and merchant bars) in 2025 (1.6 million tonnes in 2024), and captive mines that produced 7.6 million tonnes of iron ore in 2025 (7.8 million tonnes in 2024); the related carrying amount of property, plant and equipment remained unchanged at 0.7 billion on the Company’s statement of financial position at December 31, 2025 as compared to December 31, 2024. In 2025, the Company’s Ukrainian operations (and in particular its Kryvyi Rih steel plant) recorded 1.5 million of steel shipments (1.5 million tonnes in 2024), generating 1.7 billion of sales (1.6 billion in 2024) including 0.5 billion of sales (0.5 billion in 2024) to customers located in Ukraine.

Since the war outbreak in February 2022, ArcelorMittal Kryvyi Rih (“AMKR”) has reduced steel and mining production levels and experienced a combination of periods of suspension and ramp up of activity. In July 2023, AMKR completed the construction of a new pumping station and 5 kilometers pipeline to supply water to the city and to ensure full coverage of its production needs following the destruction of the Nova Kakhovka reservoir’s dam. AMKR is currently operating its open pit mining and steel facilities at 73% and 35%, respectively. ArcelorMittal continued to exercise control over its Ukrainian operations and key production assets have not been seriously damaged at the date of this report. In addition, despite the lower level of activity, none of the assets are held for sale or were discontinued.

In the context of the annual impairment test of intangible assets, including goodwill and tangible assets, the Company applied in its value in use calculation separate discount rates over the discrete projections period, including a higher country risk premium for the cash flow projections until the end of 2026 and a return to a pre-war country risk premium after 2026 and for the terminal value calculation as value in use is sensitive to a difference in country risk for different periods. It concluded that the recoverable amount remains in excess of the carrying amount. Conversely, if the ongoing conflict between Russia and Ukraine persists, it could continue to have a material effect on the overall macroeconomic environment potentially affecting steel and iron ore demand and prices as well as energy costs. It could also result in further reduced production, sales and income with respect to the Company’s Ukrainian operations thus increasing the risk that the Company may need to record an additional impairment charge with respect to such operations in the future.

In 2025, heightened uncertainty, particularly trade-related, negatively impacted the global economy. U.S. tariff policy uncertainty impacted the global economy and steel market, with frequent changes in the timing and the extent of such tariffs adding downside risk to steel demand due to its negative impact on business investment. However, despite subdued growth in real steel demand in core developed markets, steel prices were supported by improved trade protection, most notably in the U.S., followed by the EU toward the end of the year. As of October 1, 2025, when goodwill was tested for impairment, discount rates applied for value in use calculations included lower country risk premiums, in particular in Ukraine, as risk-free rates increased while governmental bond yields remained relatively stable as compared to October 1, 2024. The Company expects demand to increase in 2026 subject to macroeconomic uncertainties. The Company’s European steel shipments are expected to increase as domestic mills begin to recapture market share from imports reflecting the combined effect of CBAM and the new tariff-rate quota trade tool which should strengthen progressively over the course of the year.

NOTE 5: GOODWILL, INTANGIBLE AND TANGIBLE ASSETS (extract 1)

5.1 Goodwill and intangible assets

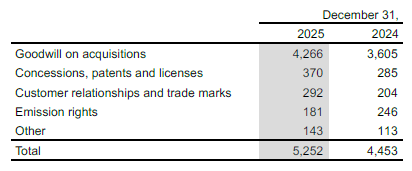

The carrying amounts of goodwill and intangible assets are summarized as follows:

Goodwill

Goodwill arising on an acquisition is recognized as previously described within the business combinations section in note 2.2.3. Goodwill is allocated to those groups of cash-generating

units (“GCGUs”) that are expected to benefit from the business combination in which the goodwill arose and in all cases is at the operating segment level, which represents the lowest level at which goodwill is monitored for internal management purposes except for goodwill allocated to AMKR cash-generating unit (“CGU”) in Ukraine and AMSA GCGU in South Africa (see below).

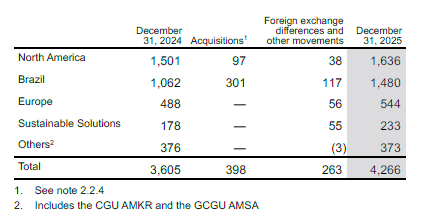

Goodwill acquired in business combinations for each of the Company’s operating segments and certain other CGUs and GCGUs is as follows:

Intangible assets are recognized only when it is probable that the expected future economic benefits attributable to the assets will accrue to the Company and the cost can be reliably measured. Intangible assets acquired separately by ArcelorMittal are initially recorded at cost and those acquired in a business combination are initially recorded at fair value at the date of the business combination. These primarily include customer relationships and trade marks as well as emission rights, and the cost of technology and licenses purchased from third parties and operating authorizations granted by governments or other public bodies (concessions). Intangible assets are amortized on a straight-line basis over their estimated economic useful lives, which typically do not exceed five years. Amortization is included in the consolidated statements of operations as part of cost of sales.

ArcelorMittal’s industrial sites which are regulated by the European Directive 2003/87/EC of October 13, 2003 on carbon dioxide (“CO2”) emission rights, effective as of January 1, 2005, are located primarily in Belgium, France, Germany, Luxembourg, Poland and Spain. In Ontario, Canada, ArcelorMittal’s operations have been subject to output based pricing system regulations since January 1, 2019 but effective January 1, 2022, they are regulated on carbon pricing under the Ontario Emissions Performance System (“OEPS”). In South Africa, a CO2 tax system was introduced in 2019.

Emission rights allocated to the Company on a no-charge basis pursuant to the annual national allocation plan are recorded at nil value and purchased emission rights are recorded at cost.

NOTE 5: GOODWILL, INTANGIBLE AND TANGIBLE ASSETS (extract 2)

5.3 Impairment of intangible assets, including goodwill, and tangible assets Impairment charges were as follows:

Impairment test of goodwill

Goodwill is tested for impairment annually, as of October 1 or whenever changes in circumstances indicate that the carrying amount may not be recoverable at the level of the CGU (in the case of AMKR) or GCGU which corresponds either to AMSA or the operating segments representing the lowest level at which goodwill is monitored for internal management purposes. Whenever the CGUs comprising the operating segments or AMSA are tested for impairment at the same time as goodwill, the cash-generating units are tested first and any impairment of the assets is recorded prior to the testing of goodwill.

The recoverable amounts of the GCGUs are mainly determined based on their value in use. The value in use of each GCGU is determined by estimating future cash flows. The 2025 impairment test of goodwill did not include the GCGU corresponding to the Mining segment as goodwill allocated to this GCGU was fully impaired in 2015. The key assumptions for the value in use calculations are primarily the discount rates, growth rates, expected changes to average selling prices, shipments and direct costs during the period. Assumptions for average selling prices and shipments are based on historical experience and expectations of future changes in the market. In addition, with respect to raw material price assumptions, the Company applied a range of $80 per tonne to $97 per tonne for iron ore ($80 per tonne to $98 per tonne in 2024) and $183 per tonne to $210 per tonne ($190 per tonne to $210 per tonne in 2024) for coking coal. Cash flow forecasts adjusted for the risks specific to the tested assets are derived from the most recent financial plans approved by management for the next 5 years. Beyond the specifically forecasted period, the Company extrapolates cash flows for the remaining years based on an estimated growth rate of 2%. This rate does not exceed the average long-term growth rate for the relevant markets.

The Company considered its exposure to certain climate-related risks which could affect its estimates of future cash flow projections applied for the determination of the recoverable amount of its GCGUs and CGUs. With the switch to electric vehicles and the move to wind and solar power generation, the Company sees also additional opportunities as customers deepen their understanding of embedded and lifecycle emissions of the materials where steel compares favorably.

The Company is committed to achieve group-wide net zero by 2050. These announced goals will require significant long-term investments which require global level playing field, access to abundant and affordable clean energy, facilitating necessary energy infrastructure, access to sustainable finance for low-emissions steelmaking and accelerated transition to a circular economy. In addition, the Company considered whether there was a net zero legal obligation in the jurisdictions in which it operates and in such cases ArcelorMittal concluded that future decarbonization capital expenditures are necessary to maintain the level of economic benefits expected to arise from the assets in their current condition and should therefore be included in the Company’s assumptions for cash flow projections to determine the recoverable amount of the respective GCGUs and CGUs. At the same time, the Company is engaged in developing in the near to medium term a range of innovative low-emission technologies for the transition to decarbonized steel and required investments are considered in the Company’s future cash flow projections. ArcelorMittal acknowledges that CGUs and GCGUs applying the BF-BOF route in jurisdictions not yet subject to a net zero legal obligation will apply decarbonization at a lower pace, as a result of which the future estimated decarbonization cost for such operations is reflected through an additional risk premium embedded in discount rates until they are able to accelerate their decarbonization strategy to meet the 2050 net zero objective and a legal obligation arises in the relevant jurisdiction.

ArcelorMittal’s most substantial climate-related policy risk is the EU Emissions Trading scheme (“‘EU-ETS”), which applies to all its European plants. The risk concerns the Company’s primary steelmaking plants which are exposed to this regulation. In addition, on January 1, 2026, the carbon border adjustment mechanism (“CBAM”) entered into force. The EUETS and CBAM regulations will impact the carbon emissions allowances from the second trading period of Phase IV (2026-2030) onwards as they will be gradually phased out (2.5% by 2026, 5% by 2027, 10% by 2028, 22.5% by 2029, 48.5% by 2030, 61% by 2031, 73.5% by 2032, 86% by 2033 and 100% by 2034). The Company’s assumptions for future cash flows include an estimate for costs that the Company expects to incur to acquire emission allowances, which primarily impacts the flat steel operations in the EU. The assumption for carbon emission cost is based on historical experience, implementation of decarbonization strategies to mitigate or otherwise offset such future costs and information available of future regulatory or operational changes. With respect to the EU-ETS scheme, the assumption for carbon emission cost includes also the gradual phasing out of free emission allowances and the forecast market price of emission rights, for which the Company considered in its five-year cash flow projections internal estimates of 77€/t, 80€/t, 80€/t, 85€/t and 100€/t for 2026, 2027, 2028, 2029 and 2030, respectively.

The assumptions used in the value in use calculations are inherently uncertain and require management judgment as described in note 1.3. The Company’s process includes specific consideration given to the most recent short, medium and long-term price forecasts and discount rates consistent with external information, expected production and shipment volumes and updated development plans, operating costs and capital expenditure plans. In 2025, heightened uncertainty, particularly trade-related, negatively impacted the global economy and steel market. However, despite subdued growth in real steel demand in core developed markets, steel prices were supported by improved trade protection, most notably in the U.S., followed by the EU toward the end of the year. The Company forecasts steel demand to increase in 2026 subject to macroeconomic uncertainties and improved outlook in Europe in connection with the combined effect of CBAM and tariff rate quota mechanism strengthening throughout the year.

Management estimates discount rates using pre-tax rates that reflect current market rates for investments of similar risk. The rate for each CGU, including beta, cost of debt and capital structure was estimated from the weighted average cost of capital of producers, which operate a portfolio of assets similar to those of the Company’s assets and CGU specific country risk premiums were applied. The weighted average pre-tax discount rates used in connection with the historical goodwill impairment testing in 2025 and 2024 are set forth below:

Once recognized, impairment losses for goodwill are not reversed.

There were no impairment charges recognized with respect to goodwill following the Company’s impairment tests as of October 1, 2025 and October 1, 2024. The total value in use calculated for all GCGUs increased overall in 2025 as compared to 2024 primarily as a result of higher cash flow projections in Europe due to above-mentioned improved outlook following CBAM and tariff rate quota implementation.

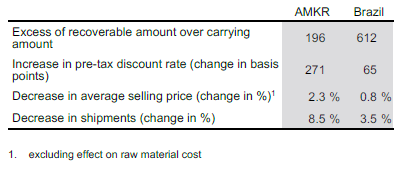

In validating the value in use determined for the GCGUs, the Company performed a sensitivity analysis of key assumptions used in the discounted cash-flow model (such as discount rates, average selling prices and shipments) and believes that reasonably possible changes in key assumptions could cause an impairment loss to be recognized in respect of AMKR and the Brazil segment.

The Brazil segment includes the flat operations of Brazil, the long and tubular operations of Brazil and neighboring countries including Argentina, Costa Rica and Venezuela. The raw material supply of the Brazil operations includes sourcing from iron ore captive mines in Brazil. Sales are mainly domestic with some export sales primarily related to flat products. The AMKR CGU consists of a long steel plant (see also note 1.3) serving mainly the domestic market and includes captive iron ore mines. The Brazil segment and AMKR operations are exposed to international steel prices which are volatile reflecting the cyclical nature of the global steel industry, developments in particular steel consuming industries and macroeconomic trends in the respective domestic markets. The Company believes that sales volumes, prices and discount rates are the key assumptions most sensitive to change. The Brazil segment value in use model anticipate higher steel shipments in 2026 (15.4 million tonnes) as compared to 2025 (13.9 million tonnes) followed by a subsequent overall upward trend. Average selling prices are expected to remain relatively stable between the beginning and the end of the 5-year forecast period with some intermediate volatility. The AMKR model anticipates slightly higher sales volumes in 2026 (1.7 million tonnes) as compared to 2025 (1.5 million tonnes) and a further subsequent increase in 2027 to a stable level. Average selling prices are expected to decrease marginally over time.

The following changes in key assumptions in projected earnings in every year of the initial 5-year period and perpetuity of the Brazil segment and AMKR operations, assuming unchanged values for the other assumptions, would cause the recoverable amount to equal the carrying amount:

Impairment test of property, plant and equipment and intangibles (excluding goodwill)

At each reporting date, ArcelorMittal reviews the carrying amounts of its intangible assets (excluding goodwill) and tangible assets to determine whether there is any indication that the carrying amount of those assets may not be recoverable through continuing use, or that a reversal of previous periods’ impairment charges may be required. If any such indication exists, the recoverable amount of the asset (or CGU) is reviewed in order to determine the amount of the impairment (or reversal of prior periods’ impairment charges), if any. The recoverable amount is the higher of its fair value less cost of disposal and its value in use.

In estimating its value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset (or cash-generating unit). For an asset that does not generate cash inflows largely independent of those from other assets, the recoverable amount is determined for the CGU to which the asset belongs. The CGU is the smallest identifiable group of assets corresponding to operating units that generate cash inflows. If the recoverable amount of an asset (or CGU) is estimated to be less than its carrying amount, an impairment loss is recognized. An impairment loss is recognized as an expense immediately as part of cost of sales (see note 4.2) in the consolidated statements of operations.

In the case of permanently idled assets, the impairment is measured at the individual asset level. Otherwise, the Company’s assets are measured for impairment at the CGU level. In certain instances, the CGU is an integrated manufacturing facility which may also be an operating subsidiary. Further, a manufacturing facility may be operated in concert with another facility with neither facility generating cash inflows that are largely independent from the cash inflows of the other. In this instance, the two facilities are combined for purposes of testing for impairment. As of December 31, 2025 and December 31, 2024, the Company determined it has 46 and 45 cash-generating units, respectively.

An impairment loss, related to intangible assets other than goodwill and tangible assets recognized in prior years is reversed if, and only if, there has been a change in the estimates used to determine the asset’s recoverable amount since the last impairment loss was recognized. However, the increased carrying amount of an asset due to a reversal of an impairment loss will not exceed the carrying amount that would have been determined (net of amortization or depreciation) had no impairment loss been recognized for the asset in prior years. A reversal of an impairment loss is recognized immediately as part of operating income in the consolidated statements of operations.

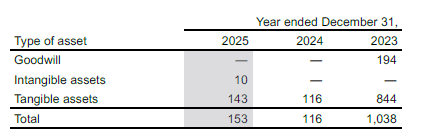

Impairment charges and reversals relating to property, plant and equipment and intangibles (excluding goodwill) were as follows for the years ended December 31, 2025, 2024 and 2023:

2025

In 2025, the Company recognized a 143 impairment charge of property, plant and equipment in the context of the measurement of the recoverable amount of the Company’s steel and mining operations in Bosnia (ArcelorMittal Zenica and ArcelorMittal Prijedor) at fair value less cost of disposal following their classification as held for sale prior to their disposal on October 30, 2025 (see note 2.3).

2024

In 2024, the Company recognized a 37 impairment charge of property, plant and equipment with respect to its Longs Business in South Africa. The wind-down, which was announced initially on January 6, 2025, was finally postponed to September 1, 2025 ahead of the end of a six-month deferral period ending on September 30, 2025. Continuation of operations during this period had been enabled by a facility provided by the Industrial Development Corporation of South Africa SOC Limited.

ArcelorMittal also recognized a 43 impairment charge of property, plant and equipment for assets measured at fair value less cost of disposal following the termination of the Monlevade expansion project in Brazil.

In addition, the Company recognized a 36 impairment charge of property, plant and equipment in connection with the definitive closure of the Kraków coke plant in Poland which was announced on July 19, 2024.

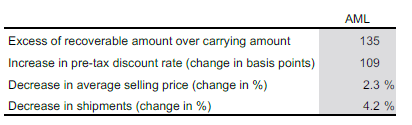

The Company reviewed impairment reversal indicators on assets previously impaired. It concluded that there was a significant change with a positive effect resulting in an impairment reversal indicator with respect to its iron ore expansion project in Liberia, which was restarted in 2021 and for which the first concentrate was produced in the fourth quarter of 2024 with full 20 million tonnes capacity expected by the end of 2025. The Company performed a value in use calculation as well as a sensitivity analysis and, in addition to the fact that the project was not yet fully operational, it concluded that no impairment reversal should be recognized in relation to the 1,426 impairment charge of property, plant and equipment and intangible assets recognized in 2015. The Company did not identify an indicator of impairment reversal for any other assets. The following changes in key assumptions in projected earnings of AML throughout the life of mine, assuming unchanged values for the other assumptions, would cause the recoverable amount to equal the carrying amount at December 31, 2024:

2023

In 2023, ArcelorMittal recognized a 732 impairment charge related to property, plant and equipment with respect to the sale on December 7, 2023 of its Kazakhstan operations in the former ACIS segment to Qazaqstan Investment Corporation, a state-controlled direct investment fund. The impairment loss resulted from the adjustment of the carrying amount of the disposal group to the net sales proceeds of 278 (see note 2.3). On November 28, 2023, AMSA announced that it contemplates the wind down of its Longs Business subject to a due diligence and a consultative process involving key customers, suppliers, organized labour, and other stakeholders. The Company assessed the recoverable amount of its Longs Business in South Africa based on a value in use calculation and recognized accordingly a 112 impairment charge of property, plant and equipment.