Roche Holding Ltd – Annual report – 31 December 2025

Industry: pharmaceuticals

5. Income taxes (extract)

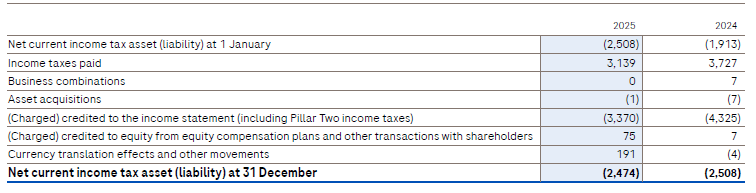

Current income taxes: movements in recognised net assets (liabilities) in millions of CHF

Roche Holding Ltd – Annual report – 31 December 2025

Industry: pharmaceuticals

5. Income taxes (extract)

Current income taxes: movements in recognised net assets (liabilities) in millions of CHF