AB Volvo (publ) – Annual report – 31 December 2024

Industry: automotive

7 Revenue

Accounting policies

The recognized net sales in Industrial Operations pertain to revenues from sales of vehicles and services. Revenue from vehicles and services are recognized when control has been transferred from Volvo Group to the customer. Control refers to the customersʼ ability to use vehicles or services in its operations and to obtain the associated cash flow related to the use. Vehicles and services are sold separately as well as in combination. In combined offers where the vehicle and services are separable from each other and the customer can benefit from the vehicle and the service independently, the transaction price is allocated between vehicles and services based on stand-alone selling price according to price lists.

The recognized net sales in Financial Services pertain to interest income related to finance leases and installment credits as well as income from operating lease contracts. Interest income is recognized during the underlying contract period and income from operating leasing is recognized over the leasing period.

Vehicles

Vehicles include sales of new trucks, buses, machines and engines as well as sales of used trucks, buses, machines, trailers, superstructures and special vehicles. A contractual warranty is included as part of the sales. The customer can pay for the vehicle at the point of sale or defer the payment by entering into agreements such as installment credits and finance lease.

Read more in Note 21 Other provisions, about product warranty.

Revenue is recognized at a specific point in time, when control of the vehicle has been transferred to the customer, normally when the vehicle has been delivered to the customer. The value of rebates, returns and variable sales price have been considered as part of the revenue recognition.

If the sale of the vehicle is combined with a residual value commitment (buybacks and tradebacks) the criterion of transferring control is based on if the customer has a significant economic incentive to exercise the option to return the vehicle or not. A significant economic incentive exists if the repurchase price is higher than the assessed fair market value i.e. net realizable value at the end of the residual value commitment period, or if the historical returns indicate that it is probable that the customer will return the vehicle at the end of the commitment period. Thus, the control has not been transferred and the sales transaction is recognized as an operating lease transaction. The revenue and expense are recognized over the residual value commitment period in the income statement. An asset under operating leases, a residual value liability, and a deferred lease income are recognized in the balance sheet. The asset is depreciated on a straight-line basis over the commitment period and the deferred lease income is recognized as revenue over the same period. The residual value liability amount remains unchanged until the end of the commitment period. If the vehicle is returned at the end of the commitment period, the residual value liability is paid to the customer and the vehicle is reclassified from assets under operating lease to inventory.

Read more in Note 14 Leasing, about lease income on assets under operating lease.

Read more in Sustainability statements and section EU Taxonomy regulation disclosures about taxonomy eligible turnover.

If the customer is not considered to have a significant economic incentive to return the vehicle, the sales transaction is recognized in accordance with the right of return model. Revenue corresponding to the sales amount less the buyback amount is recognized at the initial sale, as well as a proportionate share of cost of goods sold. The remaining revenue is recognized as a refund liability and the remaining cost of goods sold as a right of return asset during the commitment period. If the vehicle is not returned the refund liability is recognized as revenue and the right of return asset is recognized as cost of goods sold at the end of the commitment period.

Services

Services include sale of spare parts, maintenance services, repairs, extended coverage, connectivity solutions, services and solutions and other aftermarket products. Revenue is recognized when the control of the service has been transferred to the customer when the Volvo Group incurs the associated cost to deliver the service and the customer can benefit from the use of the delivered services. For spare parts, revenue is recognized at one point in time, normally when it is delivered to the customer. For maintenance services, connectivity solutions, services and solutions and other aftermarket products, revenue is recognized over time, i.e. normally during the contract period. When payment for service contracts is received in advance, the payment is recognized as a contract liability.

Services also include sales in Financial Services related to finance lease, installment credits and operating leases. During 2024, revenue from Financial Services amounted to SEK 26,982 M (24,012).

Read more in Note 6 Segment reporting regarding net sales by operating segment and geographical region.

Read more in Note 14 Leasing, about lease income on assets under operating lease and finance income on customer-financing receivables.

Source of estimation uncertainty and critical judgments

Sales with residual value commitments

When the Volvo Group enters into sales transactions of vehicles with residual value commitments (buybacks and tradebacks) the judgment whether control has been transferred from the Volvo Group to the customer and at what point in time revenue shall be recognized is critical. The judgment made is when a significant economic incentive exists or not for the customer to return the vehicle at the end of the commitment period. The assessment of significant economic incentive is performed at the inception of the contract and the outcome at the end of the commitment period can differ from the initial assessment. Factors that are considered and requires judgment is the assessed fair market value i.e. net realizable value at the end of the residual value commitment period and historical returns. The future mix of vehicles and services is driven by customer demand for products and solutions with lower environmental impact.

The gradual shift into battery electric and fuel cell electric products, as well as supply chain and production disturbances imply to some extent uncertainties in the assessment of fair market value.

Read more in Note 13 Tangible assets, for a description of residual value risks and the assessment of fair market value.

Variable sales price

In some sales transactions, the sales price is variable. In assessing the variable sales price the expected value method is used and revenue is recognized when it is highly probable that a reversal will not occur. Both the expected value method and the assessment of highly probable requires judgments to be able to make estimates. The estimates are made at the contract start with continuous assessment at each reporting period.

Contract assets are recognized within other receivables and include revenue that has been recognized but not yet invoiced for work performed.

Right of return assets and parts return assets represent the product cost for the assets that might be returned to the Volvo Group.

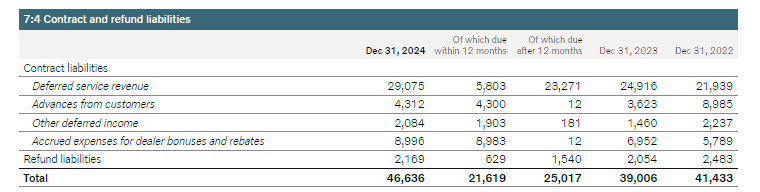

Contract liabilities are recognized within other liabilities and include advance payments received from customers, e.g. advance payments for service contracts and extended coverage, for which revenue is recognized when the service is provided. Refund liabilities related to the right to return products are included with an amount that is expected to be paid to the customer if the vehicle or spare part is returned. In service contracts, the revenue expected to be recognized over the remaining term of the contract for services not yet delivered amounted to SEK 38,873 M (34,262) as of December 31, 2024. Approximately 34% are expected to be recognized as revenue during 2025 and the remaining 66% as revenue during 2026–2028. The change in contract and refund liabilities are mainly due to increased deferred service revenue. During 2024, revenue has been recognized with SEK 26,205 M (26,023) that was included in the contract liabilities at the beginning of the period.

21 Other provisions

Accounting policies

Provisions are recognized in the balance sheet when a legal or constructive obligation exists as a result from a past event, it is probable that an outflow of resources will be required to settle the obligation and the amount can be reliably estimated. When these criteria are not met, a contingent liability may be recognized. Longterm provisions are mainly expected to be settled within 2 to 3 years.

Provisions for product warranty

Provisions for product warranty are recognized as cost of sales and include contractual warranty and campaign warranty. Provisions for contractual warranty are recognized when the products are sold. Provision for campaigns in connection with specific quality problems are recognized when the campaign is decided.

Provisions for extended coverage

An extended coverage is a product insurance sold to a customer to cover a product according to specific conditions for an agreed period as an additional insurance to the factory contractual warranty. The provision is intended to cover the risk that the expected cost of providing services under the extended coverage contract exceed the expected revenue.

Provisions in insurance operations

Volvo Group has a captive insurance company and the provisions in insurance operations are related to third party claims addressed to companies within the Volvo Group. The claims reserve also includes a provision for unreported losses based on past experience. The unearned premium reserve is reported within other current liabilities.

Provisions for restructuring costs

A provision for decided restructuring measures is recognized when a detailed plan for the implementation of the measures is complete and when this plan is communicated to those who are affected. A provision and costs for termination benefits as a result of a voluntary termination program is recognized when the employee accepts the offer. Normally restructuring costs are included in other operating income and expenses.

Provisions for residual value risks

Residual value risks are the risks that the Volvo Group in the future would have to dispose used vehicles at a loss if the price development of these products is worse than expected when the contracts were entered. The residual value risks pertain to operating lease contracts and sales transactions with residual value commitments (buybacks and tradebacks) where the Volvo Group has a residual value commitment. The majority of these contracts are recognized as assets under operating leases or as right of return assets in the balance sheet. The potential residual value risks related to these assets are not recognized as provisions, but are reflected as a reduction of the assets through accelerated depreciation and/or write-downs.

Read more in Note 13 Tangible assets about residual value risks.

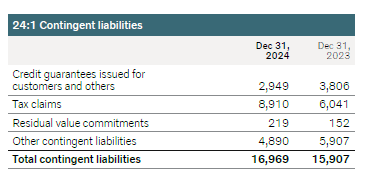

Residual value commitments that are independent from the sales transaction are not recognized as assets under operating leases or as right of return assets in the balance sheet, hence the potential residual value risks related to these contracts are recognized as provisions. To the extent the residual value exposure does not meet the definition of a provision, the gross exposure is reported as a contingent liability.

Read more in Note 24 Contingent liabilities and financial commitments.

Provisions for service contracts

Service contracts offer the customer preventive maintenance according to an agreed service plan. The provision is intended to cover the risk that the expected cost of providing services and repairs under the service contract exceeds the expected revenue.

Other provisions

Other provisions mainly include provisions for legal disputes, provisions for externally issued credit guarantees and other provisions, unless separately specified.

Source of estimation uncertainty and critical judgments

The uncertainties about the amount or timing of outflows vary for different kind of provisions. Regarding provisions for product warranty, extended coverage, residual value risks and service contracts, the provisions are based on historical statistics and estimated future costs, which is why the provided amount has a high correlation with the outflow of resources. Regarding provisions for disputes, like tax and legal disputes, the uncertainty is higher.

Provisions for product warranty

Warranty provisions are estimated with consideration of historical statistics with regard to known changes in warranty claims, warranty periods, the average time-lag between faults occurring until claims are received by the company and anticipated changes in quality indexes. The actual outcome of product warranties may deviate from the expected outcome and materially affect the warranty costs and provisions in future periods. Refunds from suppliers, that decrease the Volvo Groupʼs warranty costs, are recognized to the extent these are considered to be certain.

Other provisions

The Volvo Group works actively to ensure compliance with applicable environmental laws and regulations, which are often complex and uncertain. If the Volvo Group fails to meet climate related targets or regulatory requirements it could be subject to significant penalties and other sanctions which could materially affect the financial statements.

Provisions for legal proceedings

The Volvo Group regularly reviews the development of significant outstanding legal disputes in which the Volvo Group companies are parties, both regarding civil law and tax disputes, in order to assess the need for provisions and contingent liabilities in the financial statements. Among the factors that the Volvo Group considers in making decisions on provisions and contingent liabilities are the nature of the dispute, the amount claimed, the progress of the case, the opinions of legal and other advisers, experience in similar cases, and any decision of the Volvo Groupʼs management as to how the Volvo Group intends to handle the dispute. The actual outcome of a legal dispute may deviate from the expected outcome of the dispute. The difference between actual and expected outcome of a dispute might materially affect future financial statements, with an adverse impact upon the Volvo Groupʼs operating income, financial position and liquidity. Provisions for legal disputes are included within other provisions in Table 21:1.

Read more in Note 24 Contingent liabilities and financial commitments.

1 Includes a provision for emission control component, for more information see below.

2 Read more in Note 3 Acquisitions and divestments of operations, for a description of acquired and divested operations as well as assets and liabilities held for sale.

3 Includes provisions for restructuring costs in Volvo Buses and Nova Bus, for more information see below.

4 Includes a provision for claims arising from the European Commissionʼs 2016 antitrust settlement decision. Read more in Note 24 Contingent liabilities and financial commitments about the European Commissionʼs 2016 antitrust settlement decision.

The Volvo Group has detected that an emissions control component used in certain markets and models, may degrade more quickly than expected, affecting the vehicles emission performance negatively. The Volvo Group made a provision of SEK 7 billion impacting the operating income in 2018, relating to the estimated costs to address the issue. Negative cash flow effects started in 2019 and will continue in the coming years. As of year-end 2024, approximately half of the initial provision had been utilized. The Volvo Group will continuously assess the size of the provision as the matter develops.

Volvo Buses closed its bodybuilding factory in Wroclaw, Poland, during 2024. Restructuring costs of SEK 1.3 billion impacted operating income negatively in 2023 whereof restructuring provision SEK 1.2 billion and write down of assets SEK 0.1 billion. During 2024, SEK 0.4 billion was reversed from the provision.

Nova Bus is exiting bus production in the US market. Consequently, the company has decided to close its Plattsburgh manufacturing and delivery facility by 2025. Restructuring costs of SEK 1.3 billion impacted the Volvo Groupʼs operating income negatively in 2023, whereof restructuring provision SEK 1.0 billion, disposal of goodwill SEK 0.1 billion and write down of assets SEK 0.2 billion. During 2024, SEK 0.2 billion was reversed from the provision.

24 Contingent liabilities and financial commitment (extract)

Accounting policies

A contingent liability is recognized for a possible obligation, for which it is not yet confirmed that a present obligation exists that could lead to an outflow of resources. Alternatively, there is a present obligation that does not meet the definitions of a provision or a liability as it is not probable that an outflow of resources will be required to settle the obligation or a sufficiently reliable estimate of the amount of the obligation cannot be made.

Financial commitments are contractual commitments to a possible expense at a future date and is not reported as liabilities on the balance sheet date.

Residual value commitments amounted to SEK 219 M (152) and are attributable to sales transactions with residual value commitments (buybacks and tradebacks) that are independent from the sales transaction and therefore not recognized as assets under operating lease or as right of return assets in the balance sheet. The amount corresponds to the gross exposure of the potential residual value risk and has not been reduced by the estimated net selling price of used products taken as collaterals. To the extent the used products pertaining to those transactions are expected to be disposed at a loss, a provision for residual value risk is recognized if the residual value exposure meet the definition of a provision.

Read more in Note 7 Revenue about sales with residual value commitments.

Read more in Note 21 Other provisions about provisions for residual value risks.