Finnair Oyj – Annual report – 31 December 2023

Industry: airline

3.8 Derivatives

Derivative contracts and hedge accounting

According to its risk management policy, Finnair Group uses foreign currency, interest rate and commodity derivatives to reduce the exchange rate, interest rate and commodity risks which arise from the Group’s balance sheet items, foreign currency denominated purchase agreements, anticipated foreign currency denominated purchases and sales as well as future jet fuel purchases. It is the Group’s policy not to enter into derivative financial contracts for speculative purposes.

The derivatives are initially recognised as well as subsequently valued at fair value in each financial statement and interim report. The fair values of the derivatives are based on the value at which the instrument could be exchanged between knowledgeable, willing and independent parties, with no compulsion to sell or buy in the sales situation. The fair values of derivatives are determined as follows:

The fair values of all derivatives are calculated using the exchange rates, interest rates, volatilities and commodity price quotations on the closing date. The fair values of currency forward contracts are calculated as the present value of future cash flows. The fair values of currency options are calculated using the Black-Scholes option pricing model. The fair values of interest rate swap contracts are calculated as the present value of future cash flows. The fair values of cross-currency interest rate swap contracts are calculated as the present value of future cash flows. The fair values of interest rate options are calculated using generally accepted option valuation models. The fair values of commodity forward contracts are calculated as the present value of future cash flows. The fair values of commodity options are calculated using generally accepted option valuation models.

The Group uses credit valuation adjustment for cross-currency interest rate swaps as the maturities of these derivatives are long. The credit valuation adjustment is not done for the rest of the derivatives as the maturities for these are short and the impact would not be material. Credit risk management is described in more detail in note 3.5.

Gains and losses arising from changes in the fair value are presented in the financial statements according to the original classification of the derivative. Gains and losses on derivatives qualifying for hedge accounting are recognised in accordance with the nature of the risk being hedged. At inception, derivative contracts are designated as hedges of future cash flows, hedges of the fair value of recognised assets or liabilities and binding purchase contracts (cash flow hedges or fair value hedges) or as derivatives not meeting the hedge accounting criteria or to which hedge accounting is not applied (economic hedges). Hedging of the fair value of net investments of foreign units or embedded derivatives have not been used.

At the inception of hedge accounting, Finnair Group documents the economic relationship and the hedge ratio between the hedged item and the hedging instrument, as well as the Group’s risk management objectives and the strategy for the inception of hedging. At the inception of hedging, and at least at the time of each financial statement, the Group documents and assesses the effectiveness of hedge relationships by examining the past and prospective capacity of the hedging instrument to offset changes in the fair value of the hedged item or changes in cash flows. The values of derivatives in a hedging relationship are presented in the balance sheet item Short–term financial asset and liabilities.

Finnair Group implements the IFRS hedge accounting principles in the hedging of future cash flows (cash flow hedging). The principles are applied to the price and foreign currency risk of jet fuel, the foreign currency risk of lease payments and the foreign currency risk of highly probable future sales and costs denominated in foreign currencies. The IFRS fair value hedge accounting principles are applied to the hedging of foreign exchange and interest rate risk of aircraft.

The change in the fair value of the effective portion of derivative instruments that have been designated and qualify as cash flow hedges are recognised in comprehensive income and presented within equity in the fair value reserve, to the extent that the requirements for the application of hedge accounting have been fulfilled and the hedge is effective. The gains and losses, recognised in the fair value reserve, are transferred to the income statement in the period in which the hedged item is recognised in the income statement. When a hedging instrument expires or is sold, terminated or exercised, or the criteria for cash flow hedge accounting are no longer fulfilled, but the hedged forecast transaction is still expected to occur, the cumulative gain or loss at that point remains in the hedge reserve and is recognised in accordance with the above policy when the transaction occurs. If the underlying hedged transaction is no longer expected to take place, the cumulative unrealised gain or loss recognised in the hedge reserve with respect to the hedging instrument is recognised immediately in the consolidated income statement.

The effectiveness of hedging is tested on a quarterly basis. The effective portion of the hedges is recognised in the fair value reserve of other comprehensive income, from which it is transferred to the income statement when the hedged item is realised or, in terms of investments, as an acquisition cost adjustment.

Fair value hedging is implemented on firm orders of new aircraft, and in order to hedge the fixed interest rate bond. The binding purchase agreements for new aircraft are treated as firm commitments under IFRS, and therefore, the fair value changes of the hedged part arising from foreign currency movements are recognised in the balance sheet as an asset item, and corresponding gains or losses recognised through profit and loss. Similarly, the fair value of instruments hedging these purchases is presented in the balance sheet as a liability or receivable, and the change in fair value is recognised in profit and loss.

The gain or loss related to the effective portion of the interest rate swap, which hedges the fixed interest rate bond, is recognised as financial income or expenses in the income statement. The gain or loss related to the ineffective portion is recognised within other operating income and expenses in the income statement. The change in the fair value attributable to the interest rate risk of the hedged fixed interest rate loans is recognised in the financial expenses in the income statement.

If the hedge no longer meets the criteria for hedge accounting, the adjustment to the carrying amount of a hedged item, for which the effective interest method is used, is amortized to profit or loss over the period to maturity.

Finnair Group uses cross-currency interest rate swaps in the hedging of the interest rate and foreign exchange risks of foreign currency denominated loans. Cross-currency interest rate swaps are excluded from hedge accounting, and therefore the fair value changes are recognised in derivative assets and liabilities in the balance sheet, as well as in the financial income and expenses in the income statement. The fair value changes of the loans are simultaneously recognised in the financial income and expenses. Realised foreign exchange rate differences, as well as interest income and expenses, are recognised in the financial income and expenses against the exchange rate differences and interest income and expenses of the loan

Finnair Group uses jet fuel swaps (forward contracts) and options in the hedging of jet fuel price risk. Unrealised gains and losses on derivatives hedging jet fuel, which are designated as cash flow hedges and fulfil the requirements of IFRS hedge accounting, are recognised in the hedging reserve within other comprehensive income. Accrued derivative gains and losses, recognised in shareholders’ equity, are recognised as income or expense in the income statement in the same financial period as the hedged item is recognised in the income statement. If a forecasted cash flow is no longer expected to occur, and as a result the IFRS hedge accounting criteria are not fulfilled, the fair value changes and the accrued gains and losses reported in shareholders’ equity are transferred to the items affecting comparability in the income statement. Changes in the fair value of jet fuel swaps and options excluded from hedge accounting are recognised in fair value changes in derivatives in the income statement, while the realised result is presented in fuel costs.

For forward and option contracts, an economic relationship exists between the hedged item and the hedging instrument as the hedging instrument and the hedged item are expected to move in opposite directions because of the same underlying exposure. This is true for all hedge relationships except for the SING consumption hedged with NWE hedges (as described in section 3.5). In that case, the underlying is different, but the underlying hedged item (SING) and the hedge (NWE) have a historical correlation of 0.99. Therefore, it can be classified as a relationship where the underlying and the hedge are economically closely related. Ineffectiveness on fuel derivatives can also arise from timing differences on the notional amount between the hedged instrument and hedged item, significant changes in credit risk of parties to the hedging relationship and changes in the total amount of the hedged item, for instance if the underlying fuel consumption forecast is not accurate enough, that can result in overhedging. However, as Finnair usually hedges less than 100% of its exposure, the risk of overhedging is insignificant. Finnair has established a hedge ratio of 1:1 for hedging relationships.

Finnair uses forward contracts and options to hedge its exposure to foreign currency denominated cash flows. The hedges of cash flows denominated in foreign currencies are treated as cash flow hedges in accounting, in accordance with the hedge accounting principles of IFRS 9. Unrealised gains and losses on hedges of forecasted cash flows qualifying for hedge accounting are recognised in the hedging reserve in OCI, while the change in the fair value of such hedges not qualifying for hedge accounting is recognised in Fair value changes in derivatives and changes in exchange rates of fleet overhauls in the income statement. The change in fair value recognised in the hedging reserve in equity is transferred to the income statement when the hedged transaction is realised. Forward points are included in the hedging instrument and in the hedge relationship. Potential sources of ineffectiveness include changes in the timing of the hedged item, significant changes in the credit risk of parties to the hedging relationship and changes in the total amount of the hedged item, for instance if the underlying cash flow forecast is not accurate enough, that can result in overhedging. However, as Finnair usually hedges less than 100% of its exposure, the risk of overhedging is insignificant. Realised profit or loss on derivatives hedging JPY-denominated operating cash flows is presented in revenue, realised profit or loss on derivatives hedging a group of similar USD costs is proportionally recognised in corresponding expense lines, while profit or loss on derivatives hedging cash flows denominated in other currencies is presented in Other expenses.

The hedge ratio is defined as the relationship between the quantity of the hedging instrument and the quantity of the hedged item in terms of their relative weighting. With currency hedging, the hedge ratio is typically 1:1. For forward and option contracts, an economic relationship exists between the hedged item and the hedging instrument as there is an expectation that the value of the hedging instrument and the value of the hedged item would move in opposite directions because of the common underlying exposure.

Changes in the fair value of interest rate derivatives not qualifying for hedge accounting are recognised in financial income and expenses in the income statement. Changes in the fair value as well as realised gain or loss on forward contracts used to hedge foreign currency denominated balance sheet items of Finnair Group are recognised in financial expenses. Changes in the fair value and the realised result of hedges of assets held for sale are recognised in Items affecting comparability.

Cost of hedging

At Finnair, the time value of an option is excluded from the designation of a financial instrument and accounted for as a cost of hedging. Upon initial recognition, Finnair defers any paid premium in the cost of hedging reserve within other comprehensive income. The fair value changes of the time value are recognised in the cost of hedging reserve within other comprehensive income. The premium will be transferred to the consolidated income statement in the same period that the underlying transaction affects the consolidated income statement for transaction-related hedges. As of 31 December 2023, Finnair has deferred premiums only on transaction-related hedges.

Critical accounting estimates and sources of uncertainty

Finnair accounts for its cash flow hedges of forecasted foreign currency denominated purchases and sales and future jet fuel purchases in accordance with the IFRS 9. Under the hedge accounting principles, a forecast transaction can be designated as a hedged item only if that transaction is considered as highly probable. The evaluation of probability is based on the management forecasts about the future level of Finnair’s operations and cash flows. Such forecasts require the use of management judgement and assumptions, which inherently contain some degree of uncertainty. Should the expected circumstances or outcome change in the future, the management would need to reassess whether a hedged forecast transaction is still highly likely to occur. This could be the case if, for example, the expected recovery and thus the expected jet fuel consumption levels would not realize as expected. Should the forecast transaction no longer be highly probable, it would no longer qualify as an eligible hedged item and hedge accounting would need to be discontinued. Should it no longer be expected to occur at all, the balance of the cash flow hedge reserve included in other comprehensive income would need to be reclassified to profit or loss.

* Positive (negative) fair value of hedging instruments as of 31.12.2023 is presented in the statement of financial position in the item derivative financial instruments within current assets (derivative financial instruments within current liabilities). However, during the year 2023 Finnair has resumed normal hedging operations.

3.9 Equity-related information (extract)

*Forward and option contracts hedging forecasted sales and purchases denominated in foreign currencies are hedges of a group of similar hedged items, and the amounts reclassified from OCI to P&L are proportionally allocated to different cost lines based on the realised cost amounts. Amounts reclassified to revenue and different cost lines are specified in the table ”Derivatives realised through profit or loss” in note 3.8.

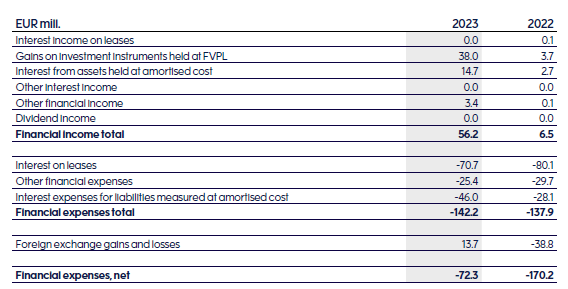

3.1 Financial income and expenses

The notes related to financial assets, liabilities and equity have been gathered into the capital structure and financing costs-section in order to give a better overview of the Group’s financial position. The note ´Earnings per share´ has been added to the equity section.

Interest income and expenses

Interest income and expenses are recognised on a time-proportion basis using the effective interest method. Interest expenses related to the financing of significant investments are capitalised as part of the asset acquisition cost and depreciated over the useful life of the asset.

More detailed information about financial assets can be found in note 3.2 and about interest bearing liabilities in note 3.3.

In the effectiveness testing of the Group’s hedge accounting, both cash flow and fair value hedging were found to be effective at year end 2023. Thus, as in the comparison year 2022, no inefficiency is included in the financial items for 2023. Financial income and expenses include an identical amount of profit and loss for fair value hedging instruments and for hedged items resulting from the hedged risk.

In 2023, foreign exchange gains and losses recognised in financial expenses consist of a net realised exchange loss of 1.1 million euro and a net unrealised exchange gain of 14.8 million euro which were mostly, caused by strengthening of US dollar relative to euro. During the year 2023, 3.0 million euros of interest expense was capitalised in connection with the A350 investment program (1.8). More information about the capitalised interest can be found in note 2.1 Fleet and other fixed assets.

Other financial expenses include for example guarantee fees as well as interest and penalties related to taxes.