Makita Corporation – Half year results – 30 September 2018

Industry: manufacturing

- Condensed Consolidated Financial Statements (Unaudited) (extract)

(5) Notes to Consolidated Financial Statements (extract)

First-time Adoption of IFRS

The Makita Group has disclosed quarterly consolidated financial statements prepared in accordance with IFRS from the three-month period ended June 30, 2018. The Group prepared the latest consolidated financial statements prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for the year ended March 31, 2018. The IFRS transition date is April 1, 2017.

(1) Exemptions of Retrospective Adoption of IFRS 1

IFRS 1 “First-time Adoption of International Financial Reporting Standards” (“IFRS 1”) requires an entity that adopts IFRS for the first time to prepare a complete set of financial statements based on IFRS retrospectively to prior periods. However, IFRS 1 provides mandatory exceptions and voluntary exemptions from full retrospective application. The effects of applying these provisions are adjusted in retained earnings or other components of equity on the transition date.

The main exemptions adopted by the Company are as follows:

- Business combinations

IFRS 1 allows an entity not to apply IFRS 3 “Business Combinations” (“IFRS 3”) retrospectively to business combinations that occurred prior to the transition date.

The Makita Group chose not to apply IFRS 3 retrospectively to business combinations that occurred prior to the transition date. Consequently, the Group recognized goodwill arisen from business combinations that occurred prior to the transition date at book value based on U.S. GAAP. Makita performed impairment tests on the goodwill at the transition date regardless of whether there was any indication that the goodwill may be impaired.

- Exchange differences on translating foreign operations

IFRS 1 allows an entity to choose to deem the cumulative amount of the exchange differences on translating foreign operations to be zero as of the transition date. The Makita Group deemed the cumulative amount of the exchange differences on translating foreign operations to be zero on the transition date.

- Designation of financial instruments recognized prior to the IFRS transition date

IFRS 1 allows an entity to designate financial instruments valued at fair value through other comprehensive income in accordance with IFRS 9 “Financial Instruments,” based on facts and circumstances that existed as of the transition date. The Makita Group designated its financial instruments based on the circumstances as of the transition date.

(2) Mandatory Exceptions of Retrospective Adoption of IFRS 1

IFRS 1 prohibits an entity from retrospectively applying IFRS with respect to “Accounting estimates,” “Derecognition of financial assets and liabilities,” “Non-controlling interest,” and “Classification and measurement of financial assets.” The Makita Group has applied the relevant IFRSs to these transactions prospectively from the transition date.

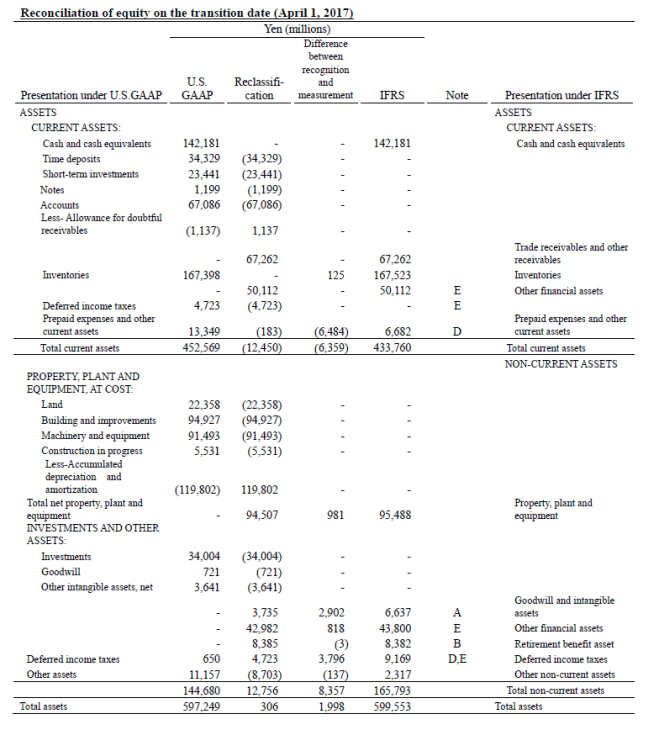

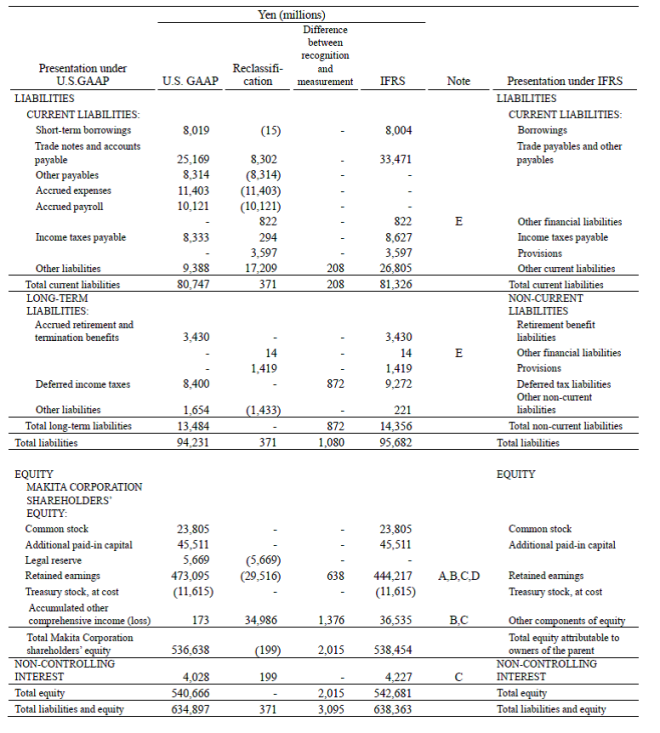

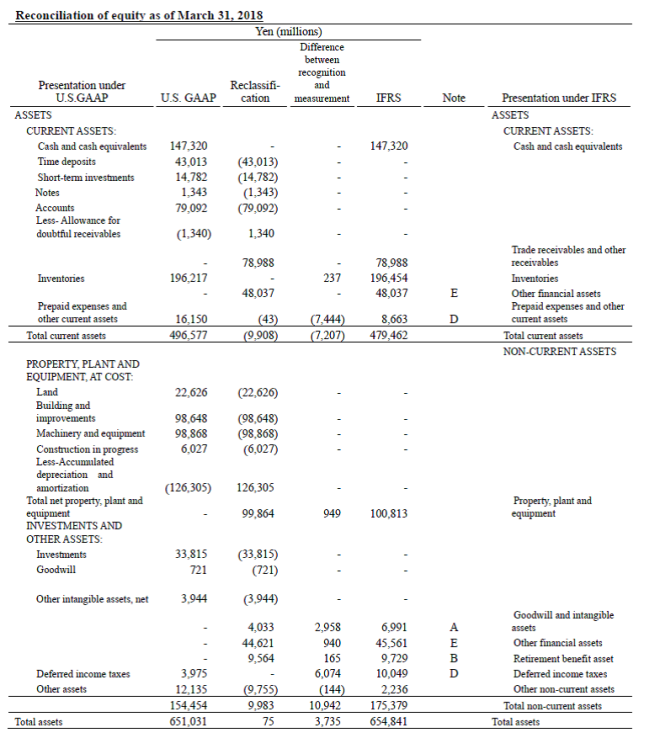

(3) Reconciliation

In preparing the consolidated financial position statement on the IFRS transition date, the Makita Group has reconciliated amounts in consolidated financial statements prepared based on U.S. GAAP. The effects of the transition from U.S. GAAP to IFRS on the Group’s financial position, financial results, and cash flow position are presented in the following table:

Notes to Reconciliation

A. Intangible assets

As some development costs, which are a part of expenditures related to R&D that were expensed under U.S. GAAP, meet the requirements to be capitalized under IFRS, they are recognized as intangible assets in its consolidated financial position statement and amortized over its expected useful lives on a straight-line basis.

Due to the above-mentioned differences in the accounting standards, the unamortized balance of capitalized development costs of 2,902 million yen, 2,967 million yen, and 2,958 million yen, respectively, were recorded as intangible assets on the transition date, at September 30, 2017, and at March 31, 2018, respectively. Consequently, retained earnings after deducting the adjusted deferred tax of 876 million yen, 896 million yen, and 893 million yen on the transition date, at September 30, and at March 31, 2018, respectively, increased by 2,026 million yen, 2,071 million yen, and 2,065 million yen, respectively.

B. Employee benefits

Under U.S. GAAP, regarding post-employment benefits under defined benefit pension plans, service cost, interest cost, and expected return on plan assets were recognized in profit or loss. The portion of actuarial differences arising from the relevant plans and past service cost incurred that was not recognized as expenses for the period was recognized in the amount net of tax in accumulated other comprehensive income (loss), and the amount recognized in accumulated other comprehensive income (loss) was subsequently recognized in income or loss over the average remaining service years of employees.

Under IFRS, regarding post-employment benefits under defined benefit pension plans, current service cost and past service cost are recognized in profit or loss, and the amount calculated by multiplying net defined benefit liability (asset) by the discount rate is recognized as interest expense (income) in profit or loss. Remeasurements of the net defined benefit liability (asset) are recognized in other comprehensive income, and transferred from other components of equity directly to retained earnings, not through profit or loss.

Due to the above-mentioned differences in the accounting standards, actuarial differences of 8,869 million yen (loss) and past service liability of 2,455 million yen (profit) on the transition date are transferred to retained earnings.

C. Exchange differences on translating foreign operations

IFRS allows an entity to choose to deem the full cumulative amount of the exchange differences on translating foreign operations to be zero on the transition date.

Consequently, the exchange differences on translating foreign operations of 28,572 million yen out of accumulated other comprehensive income on the transition date are transferred to retained earnings.

D. Income taxes

Under U.S. GAAP, regarding tax effect from the elimination of unrealized gains on intercompany transactions, income taxes paid by the seller were recorded as prepaid income taxes. Under IFRS, regarding the said tax effect, a deferred tax asset is recorded using the effective tax rate of the buyer as a temporary difference of assets held by the buyer.

Due to the above-mentioned differences in the accounting standards, on the transition date, at September 30, 2017, and at March 31, 2018, other comprehensive income, net of tax decreased by 6,484 million yen, 7,443 million yen, and 7,444 million yen, respectively, deferred tax assets increased by 5,730 million yen, 6,455 million yen, and 6,420 million yen, respectively, while retained earnings declined by 754 million yen, 988 million yen, and 1,024 million yen, respectively.

E. Reclassification of items in consolidated statement of financial position

Although some items are reclassified in the consolidated statement of financial position to conform with IFRS provisions, there is no effect on consolidated statements of income, consolidated statements of comprehensive income, and retained earnings. The following items represent major items that are reclassified in the consolidated statement of financial position.

(i) In accordance with the presentation provisions under IFRS, financial assets and financial liabilities are presented on an individual basis.

(ii) Under U.S. GAAP, deferred tax assets and deferred tax liabilities were presented separately in current assets/liabilities and non-current assets/liabilities. However, since they are not allowed to be presented in current assets/liabilities under IFRS, they are reclassified as non-current assets/liabilities.

(iii) Other reclassifications have been made by aggregating or separating presentation under U.S. GAAP to be consistent with the presentation under IFRS.

F. Reclassification of items in consolidated statements of profit or loss

Although some items are reclassified in the consolidated statements of profit or loss to conform with IFRS provisions, there is no effect on retained earnings. The following items represent major items that are reclassified in the consolidated statements of profit or loss.

(i) In accordance with the presentation provisions under IFRS, financial income and financial expenses are presented on an individual basis.

Reconciliation of consolidated cash flows for the six-month period ended September 30, 2017 and the year ended March 31, 2018

There is no material difference between consolidated statements of cash flows disclosed in accordance with U.S. GAAP and those disclosed in accordance with IFRS.