AGL Energy Limited – Annual report – 30 June 2019

Industry: utilities

38. Summary of other significant accounting policies (extract)

(c) Adoption of new and revised accounting standards and Interpretations (extract 1)

AGL has applied the required amendments to Standards and Interpretations that are relevant to its operations and effective for the current reporting period for the first time for the financial year commencing 1 July 2018.

• AASB 9 Financial Instruments

• AASB 15 Revenue from Contracts with Customers.

The following standards were early adopted:

• AASB 16 Leases (AGL has voluntarily elected to early adopt AASB 16 from 1 July 2018).

Disclosures with respect to the application of these new Standards and Interpretations are provided in this note. There were a range of other new or amended Standards and Interpretations applicable from 1 July 2018, however these did not have any material impact on the disclosures or on the amounts recognised in AGL‘s consolidated financial statements. With the exception of AASB 16 Leases, AGL has not early adopted any other accounting standards, interpretations or amendments that have been issued, but are not yet effective.

(c) Adoption of new and revised accounting standards and Interpretations (extract 2)

AASB 16 Leases (AASB 16)

AASB 16 Leases is effective for annual reporting periods commencing on or after 1 January 2019, with early application permitted for entities that also apply AASB 15. AGL elected to early adopt AASB 16 for the reporting period beginning 1 July 2018 using the full retrospective method of transition. Consequently, the impact of the new standard has been calculated as if the standard had always applied, subject to the practical expedients permitted on transition (outlined below). The cumulative retrospective impact has been recognised as at 1 July 2017, being the beginning of the earliest

comparative period presented. The comparative information has been restated for the effects of the new accounting policy. Previously, AGL accounted for leases in accordance with AASB 117 Leases and AASB Interpretation 4 Determining whether an arrangement contains a lease. The new accounting policy for leases in accordance with AASB 16 is provided at note 18. Detailed disclosures of the impact of transition are provided below. AGL has elected to apply the grandfathering practical expedient on transition to AASB 16. This means that for arrangements entered into before 1 July 2018, AGL has not reassessed whether it is, or contains, a lease in accordance with the new AASB 16 lease definition. Consequently, existing contracts as at 1 July 2018 continued to be assessed per the previous accounting policy described below in accordance with AASB 117 and AASB Interpretation 4. Given this, the transition and new requirements of AASB 16 per the new accounting leases policy described at note 18, have only been applied to arrangements entered into, or modified after, 1 July 2018.

AGL as lessee

In accordance with previous lease standards, assets held pursuant to finance leases were initially recognised as assets of AGL at their fair value at the inception of the lease or, if lower, at the present value of the minimum lease payments. The corresponding liability to the lessor was included in the Consolidated Statement of Financial Position as a finance lease liability. Lease payments were apportioned between finance charges and reduction of the lease liability so as to achieve a constant rate of interest on the remaining balance of the liability. Finance charges were recognised immediately in profit or loss. Assets held pursuant to finance leases were depreciated over their expected useful lives on the same basis as owned assets or, where shorter, the term of the relevant lease. Operating leases were not recognised on the Consolidated Statement of Financial Position. Instead, operating lease payments were recognised as an expense on a straight-line basis over the lease term. Contingent rentals arising pursuant to operating leases were recognised as an expense in the period in which they were incurred. Lease incentives received to enter into operating leases were recognised as a liability. The aggregate benefit of incentives was recognised as a reduction of rental expense on a straight-line basis. In accordance with AASB 16, there is no distinction between operating and finance leases. Instead, practically all leases are accounted for using a single on-balance sheet model similar to finance leases pursuant to AASB 117. At the inception date of a lease, a liability is recognised representing an obligation to make future lease payments (i.e. the lease liability) and an asset is recognised representing the right to use the underlying asset for the lease term (i.e. right-of-use (ROU) asset). Interest expense on the lease liability and depreciation expense on the ROU asset is recognised in the statement of profit or loss. The lease expense recognition pattern is generally accelerated as compared to the pattern under previous accounting standards. AASB 16 includes two recognition exemptions for lessees – leases of ’low-value’ assets (e.g., personal computers) and short-term leases (i.e., leases with a lease term of 12 months or less). Lease liabilities are remeasured upon the occurrence of certain events (e.g., a change in the lease term, a change in future lease payments resulting from a change in an index or rate used to determine those payments). The amount of the remeasurement of the lease liability is generally recognised as an adjustment to the ROU asset.

AGL as lessor

Lessor accounting in accordance with AASB 16 is substantially unchanged from the requirements pursuant the previous standard. Lessors continue to classify all leases using the same classification principles pursuant to the previous standards and distinguish between two types of leases: operating and finance leases.

In contracts where AGL is a lessor, AGL determines whether the lease is an operating lease or finance lease at the inception of the lease. The lease is a finance lease if it transfers substantially all of the risks and rewards incidental to ownership of the underlying asset to the lessee in the contract. If not, the lease is classified as an operating lease. AGL assesses the classification of a lease considering the following indications of finance leases:

• the lease transfers ownership of the underlying asset to the lessee by the end of the lease term;

• the lessee has the option to purchase the underlying asset at a price that is expected to be sufficiently lower than the fair value at the date the option becomes exercisable for it to be reasonably certain, at the inception date, that the option will be exercised;

• the lease term is for the major part of the economic life of the underlying asset even if title is not transferred;

• at the inception date, the present value of the lease payments amounts to at least substantially all of the fair value of the underlying asset; and

• the underlying asset is of such a specialised nature that only the lessee can use it without major modifications.

The limited changes in accounting for lessors do not impact AGL.

Finance leases

Amounts due from lessees pursuant to finance leases are recognised as receivables at the amount of AGL’s net investment in the leases. Finance lease income is allocated to accounting periods so as to reflect a constant periodic rate of return on AGL’s net investment outstanding in respect of the leases.

Operating leases

Amounts due from lessees pursuant to operating lease are recognised as lease income on a straight-line basis over the lease term.

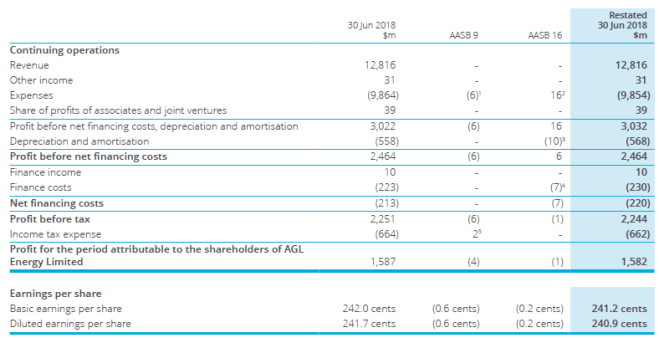

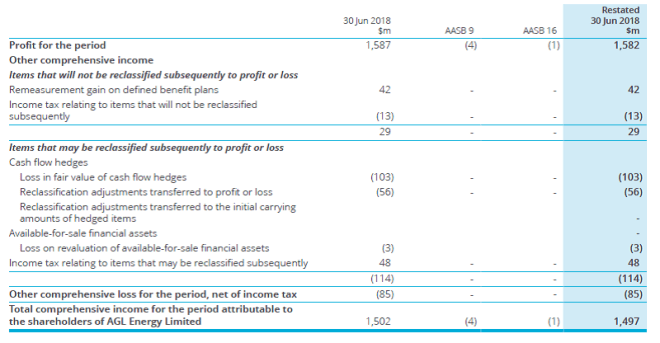

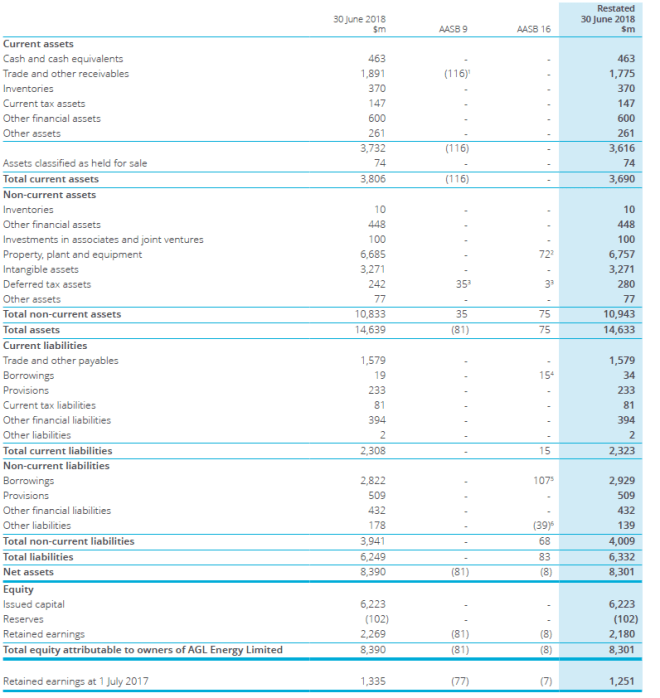

Overall impact of adopting AASB 9, AASB 15 and AASB 16

The following tables summarise the adjustments recognised against each individual line item within the relevant primary statements for all standards. Line items that were not affected by the changes have not been included in the table below. As a result, the sub-totals and totals disclosed cannot be recalculated from the numbers provided. The specifics of the adjustments for each standard are explained in more detail below. AASB 15 did not have a material impact on adoption.

- The additional credit loss on trade receivables recognised pursuant the simplified expected credit loss model.

- The reduction in rental expenses on the adoption of AASB 16 Leases.

- The depreciation expense on the right-of-use asset recognised on the adoption of AASB 16 Leases.

- The interest expense on the lease liability recognised on the adoption of AASB 16 Leases.

- The tax effect of accounting standard adjustments.

- The remeasurement of the expected credit loss allowance recognised pursuant the simplified expected credit loss model.

- The recognition of the right-of-use asset on the adoption of AASB 16 Leases .

- The tax effect of the accounting standards adjustments.

- The lease liability obligations due within a 12 month period from the balance date.

- The non-current element of lease liabilities recognised on the adoption of AASB 16 Leases.

- The derecognition of the straight line lease liability previously recognised pursuant to AASB 117 Leases.

18. Borrowings (extract)

ACCOUNTING POLICY

Borrowings

Interest bearing liabilities

All loans and borrowings are initially recognised at fair value, being the amount received less attributable transaction costs. After initial recognition, interest bearing liabilities are stated at amortised cost with any difference between cost and redemption value being recognised in profit or loss over the period of the borrowings on an effective interest basis.

Leases

At inception of a contract, AGL assesses whether a contract is, or contains a lease. A contract is, or contains a lease, if the contract conveys to the customer a right to control the use of an identified asset for a period of time in exchange for consideration.

AGL assesses whether:

• The contract involves the use of an identified asset – the asset may be explicitly or implicitly specified in the contract. Capacity portions of larger assets would be considered an identified asset if the portion is physically distinct or if the portion represents substantially all of the capacity of the asset. An asset is not considered an identified asset if the supplier has the substantive right to substitute the asset throughout the period of use.

• The customer in the contract has the right to obtain substantially all of the economic benefits from the use of the asset throughout the period of use.

• The customer in the contract has the right to direct the use of the asset throughout the period of use – the customer is considered to have the right to direct the use of the asset only if either:

– The customer has the right to direct how and for what purpose the identified asset is used throughout the period of use; or

– The relevant decisions about how and for what purposes the asset is used are predetermined and the customer has the right to operate the asset, or the customer designed the asset in a way that predetermines how and for what purpose the asset will be used throughout the period of use.

AGL has applied the above approach in identifying leases in contracts entered into, or modified, on or after 1 July 2018. For contracts entered into before 1 July 2018, AGL has elected to apply the grandfathering practical expedient on transition as detailed in note 38(c). Consequently, the transition and measurement requirements only apply to arrangements that were identified as leases pursuant to the previous leases standards as at and subsequent to 1 July 2018.

AGL as lessee

In contracts where AGL is a lessee, AGL recognises a right-of-use asset and a lease liability at the commencement date of the lease for all leases other than short-term or low-value asset leases.

Lease liabilities

A lease liability is recognised in relation to each lease and is initially measured at the present value of future lease payments at the commencement date. To calculate the present value, the future lease payments are discounted using the interest rate implicit in the lease (IRIL), if the rate is readily determinable. If the IRIL cannot be readily determined, the incremental borrowing rate at the commencement date is used. Lease payments included in the measurement of the lease liability comprise the following:

• Fixed payments, including in-substance fixed payments;

• Variable lease payments that depend on an index or a rate, initially measured using the index or rate as at the commencement date (e.g. payments that vary due to changes in CPI, or commodity prices); and

• Amounts expected to be payable by the lessee under residual value guarantees, purchase options and termination penalties (where relevant).

Variable payments other than those included in the measurement of the lease liability above (i.e. those not based on an index or rate) are recognised in profit or loss in the period in which the event or condition that triggers those payments occur.

For contracts containing lease and non-lease components, AGL accounts for each lease component separately from the non-lease components of the contract, where material. The consideration in the contract is allocated to the components based on their relative stand-alone prices.

Subsequently, the lease liability is measured in a manner similar to other financial liabilities, i.e., at amortised cost using the effective interest rate method. This means the liability is:

• Increased to reflect interest on the lease liability;

• Decreased to reflect lease payments made; and

• Remeasured to reflect any reassessment of lease payments or lease modifications, or to reflect revised in-substance fixed lease payments.

After commencement date, the following amounts are recognised in profit or loss with respect to the payments pursuant to the lease:

• interest expense: recognised as finance cost; and

• variable lease payments not based on an index or a rate: recognised in profit or loss in the period in which the event or condition that triggers those payments occurs.

Short-term and low value leases

AGL has elected to apply the practical expedients available for short-term leases (i.e. where the lease term is less than 12 months) and low-value asset leases. As a result of application of these practical expedients, the measurement requirements above do not apply and the expense for these leases is recognised on a straight-line basis.

CRITICAL ACCOUNTING ESTIMATES AND ASSUMPTIONS

Leases

Lease term

Where lease arrangements contain options to extend the term or terminate the contract, AGL assesses whether it is ‘reasonably certain’ that the option to extend or terminate the contract will be made. Consideration is given to the prevalence of other contractual arrangements and or the economic circumstances relevant to the lease contract, that may indicate the likelihood of the option being exercised. Lease liabilities and ROU assets are measured using the reasonably certain contract term.

Lease discount rates

The discount rate applicable to a lease arrangement is determined at the inception of the contract or when certain modifications are made to the contract. The discount rate applied is the rate implicit in the arrangement, or if unknown, AGL’s incremental borrowing rate. The incremental borrowing rate is determined with reference to AGL’s borrowing portfolio at the inception of the arrangement or the time of the modification and the amount and nature of the lease arrangement. If the arrangement relates to a specialised asset, incremental project financing assumptions are considered.

14. Property, plant and equipment (extract)

ACCOUNTING POLICY (extract)

Right-of-use assets (ROU assets)

A ROU asset is recognised in relation to each lease and is initially measured at cost comprising the initial measurement of the lease liability adjusted for any lease payments made before the commencement date (reduced by lease incentives received), plus initial direct costs incurred in obtaining the lease and an estimate of costs to be incurred in dismantling and removing the underlying asset, restoring the site on which it is located or restoring the underlying asset to the condition required by the terms and conditions of the lease, unless those costs are incurred to produce inventories.

A ROU asset is subsequently measured using the cost model less any accumulated depreciation and any accumulated impairment losses; and adjusted for any remeasurement of the lease liability. AGL does not apply the revaluation model but instead carries all ROU assets at cost. The ROU asset is depreciated over its useful life. The useful life of a ROU asset for depreciation purposes is the shorter of the useful life of the asset and the lease term. Where the ROU asset is adjusted due to changes in the lease liability, the depreciation for the ROU asset is adjusted on a prospective basis.

The following estimated useful lives are used in the calculation of depreciation on ROU assets:

• Plant and equipment – ROU assets: lesser of lease period or up to 50 years

• Other – ROU assets: lesser of lease period or up to 50 years

Short-term and low value leases as lessee

AGL has elected to apply the practical expedients available for short-term leases (i.e. where the lease period is 12 months or less) and low-value asset leases. As a result of application of these practical expedients, the measurement requirements of accounting standards do not apply and the expense for these leases is recognised on a straight-line basis.