Swire Properties Limited – Annual report – 31 December 2025

Industry: investment property

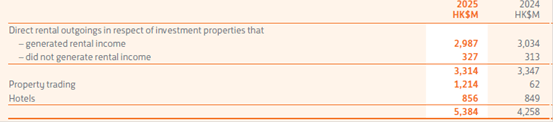

4. Revenue (extract)

Revenue represents sales by the Company and its subsidiary companies to external customers which comprises:

5. Cost of Sales

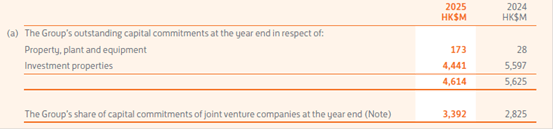

37. Capital Commitments

Note:

Of which the Group is committed to provide funding of HK$1,217 million (2024: HK$845 million).

At 31st December 2025, the Group was committed to inject capital of HK$982 million (2024: HK$1,549 million) into joint venture companies.

(b) At 31st December 2025, the Group had unprovided contractual obligations for future repairs and maintenance on investment properties of HK$243 million (2024: HK$521 million).

39. Lease Commitments

Accounting Policy

Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases. Receipts by the Group as a lessor under operating leases (net of any incentives paid to lessees) are recognised as income in the consolidated statement of profit or loss on a straight-line basis over the period of the lease.

For commenced leases (which are not identified as low-value or short-term leases) undertaken by the Group as a lessee, right-of-use assets and the corresponding lease liabilities are recognised in the financial statements when the leased assets become available for use. Commitments in respect of leases payable by the Group as a lessee represent the future lease payments for (i) committed leases which have not yet commenced at the year-end date and (ii) short-term leases.

The Group acts as both lessor and lessee under operating leases. Details of the Group’s commitments under non-cancellable operating leases are set out as follows:

(a) Lessor – lease receivables

The leases for investment properties typically run for periods of three to six years. The retail turnover-related rental income received from investment properties during the year amounted to HK$999 million (2024: HK$1,072 million).

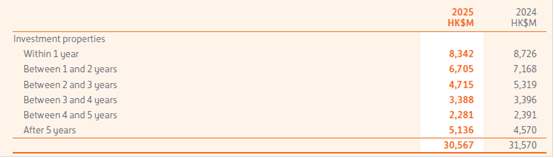

The future aggregate minimum lease receipts under non-cancellable operating leases were receivable by the Group at the year end as follows:

Assets held for deployment on operating leases at the year end were as follows:

(b) Lessee

At 31st December 2025, there were no future lease payments under leases committed but not yet commenced by the Group and no short-term leases commitments which were significantly dissimilar to those relating to the portfolio of short-term leases for which expenses were recognised for the year ended 31st December 2025 (2024: none).