Coats Group plc – Annual report – 31 December 2017

Industry: manufacturing

FINANCIAL REVIEW (extract)

Pensions and other post-employment benefits

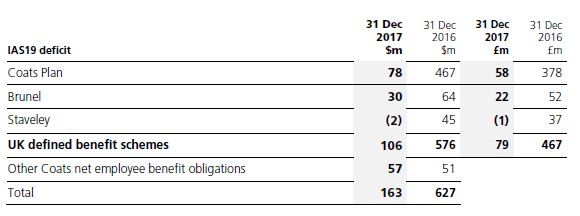

The net obligation for the Group’s retirement and other post-employment defined benefit liabilities, on an IAS19 financial reporting basis, was $163 million as at 31 December 2017, down from $627 million at 31 December 2016.

The deficits in the Group’s UK defined benefit schemes, namely the UK Coats Plan, and Brunel and Staveley schemes, decreased to $106 million (£79 million) from the position at 31 December 2016 ($576 million, £467 million). The decrease in liabilities in the period of $470 million primarily consisted of deficit repair payments of $373 million (which included agreed upfront settlement payments of £270 million ($348 million) made in the first half), actuarial gains of $141 million (mainly related to asset outperformance) offset by the impact of foreign exchange on Sterling liabilities of $31 million.

Pensions investigations

As previously reported in the announcements of 16 December 2016, 17 February 2017, and 26 June 2017 Coats has signed binding settlement agreements with the Trustees of all three UK pension schemes; the UK Coats Pension Plan, the Brunel Holdings Pension scheme and the Staveley Industries Retirement Benefit Scheme. The settlements with the three schemes were completed in the first half of 2017, and as a result the UK Pension Regulator confirmed that its regulatory action has ceased in relation to the warning notices issued to the Company in 2013 and 2014.

The principal commercial terms of the combined three settlements are:

- Financial support on the basis of a combined technical provisions deficit as at April 2015 of £582 million ($786 million) to be repaired by:

a) upfront payments totalling £329.5 million ($447 million) from the Company’s parent group cash paid directly into the schemes (inclusive of the agreed Recovery Plan contributions paid to the Brunel and Staveley schemes since 1 January 2016); and

b) annual deficit contributions totalling £17.5 million ($24 million), including estimated administration expenses and levies of £5 million p.a. to be paid until 2028.

- Access to sponsor support from Coats for future funding needs together with a Company guarantee.

As a result of the settlements reached with the three schemes, the total cash Recovery Plan contributions in 2017, including estimated administration expenses and levies, were £290 million ($373 million). This comprised £270 million upfront settlement payments (which were paid in H1), and £20 million annual deficit contributions, including estimated administration expenses and levies. These cash payments continue to be excluded from the Group’s adjusted Free Cash Flow.

Triennial funding valuations

The next triennial funding valuations for the Coats UK, Brunel and Staveley schemes have an effective date of 31 March 2018.

Although there is a relatively small IAS19 accounting deficit as at 31 December 2017 in comparison to the defined benefit obligations, the pension trustees are required to calculate the funding position on the more prudent ‘technical provisions’ basis. In addition, real UK interest rates have reduced since the first quarter of 2015 and in aggregate the UK schemes now hedge c.70% of interest rate and inflation linked liabilities. These triennial valuations will determine the Group’s agreed future contribution requirements and the process is expected to be completed in the first half of 2019.

NOTES TO THE FINANCIAL STATEMENTS (extract)

10 Retirement and other post-employment benefit arrangements (extract 1)

ii) UK regulatory investigation

In 2013 and 2014 the UK Pension Regulator (‘tPR’) issued warning notices to the Group in respect of its three UK defined benefit schemes. During 2017 the Group signed binding settlement agreements with the Trustees of all three UK pension schemes. The binding settlement agreements in respect of the UK Coats Pension Plan and Brunel Holdings Pension Scheme were signed on 16 February 2017. The binding settlement agreement in respect of the Staveley Industries Retirement Benefit Scheme was signed on 25 June 2017. The settlements with the three schemes completed shortly after the signing of the binding settlement agreements, and as a result tPR confirmed that its regulatory action in respect of the warning notices issued to the Group in respect of the three UK schemes had ceased.

The principal commercial terms of the combined settlements were:

- Financial support on the basis of a combined technical provisions deficit as at April 2015 of £582 million to be repaired as set out in the UK funding commitments section iii) below; and

- Access to sponsor support from Coats Limited for future funding needs together with a Company guarantee.

iii) UK funding commitments

The information provided below for defined benefit plans has been prepared by independent qualified actuaries based on the most recent actuarial valuations of the schemes, updated to take account of the valuations of assets and liabilities as at 31 December 2017. For the principal schemes, the date of the most recent actuarial valuations at the year end were 1 April 2015 for the Coats UK scheme, 31 December 2015 for the Coats US scheme, 5 April 2015 for the Staveley scheme and 31 March 2015 for the Brunel scheme.

At the year end the position of the triennial actuarial valuations of the UK defined benefit pension schemes was as follows:

The triennial valuation of the Coats UK pension plan as at 1 April 2015 showed an actuarial deficit of £405 million, which equated to a funding level of 79%. A recovery plan has been agreed with the trustees comprising contributions from 1 April 2015 up to settlement, a one off settlement payment of £200 million in February 2017 and contributions of £8.2 million per annum payable from February 2017 until 30 June 2028.

The triennial valuation of the Brunel scheme as at 31 March 2015 showed an actuarial deficit of £80 million, which equated to a funding level of 59%. A recovery plan has been agreed with the trustees comprising contributions from 1 April 2015 up to settlement, a one off settlement payment of £34.5 million in February 2017 and contributions of £1.7 million per annum payable with effect from January 2017 until 31 March 2028.

The triennial valuation of the Staveley scheme as at 5 April 2015 showed an actuarial deficit of £97 million, which equated to a funding level of 66%. A recovery plan has been agreed with the trustees comprising contributions from 1 April 2015 up to settlement, a one off settlement payment of £34.5 million in June 2017 and contributions of £2.2 million per annum payable with effect from June 2017 until 31 March 2028.

The Group will also fund the administrative expenses of the three UK schemes; and the next triennial valuations are due as at 31 March 2018 and are anticipated to be completed by 30 June 2019.

The actuarial valuation deficits above are used to determine the level of deficit repair contributions that the Group is required to pay into the UK pension schemes. The actuarial valuation is different to the IAS 19 accounting valuation (set out below), which are based on accounting rules concerning employee benefits and shown on the consolidated statement of financial position. The actuarial valuations are generally based on the more prudent “Technical Provisions” basis than that used for accounting purposes and as a result the actuarial deficits are generally higher than the accounting deficits. It should also be noted that the accounting deficit figures are calculated as at the balance sheet date of 31 December 2017. The actuarial valuations were performed on the dates set out above and are before the one-off pension settlement payments and subsequent deficit repair contributions.

10 Retirement and other post-employment benefit arrangements (extract 2)

xiii) Expected contributions for 2018

The total estimated amount to be paid in respect of all of the Group’s retirement and other post-employment benefit arrangements during the 2018 financial year (excluding administrative expenses paid by the Company) is $23.5 million.