Smiths Group plc – Annual report – 31 July 2024

Industry: manufacturing

Key estimates and significant judgements (extract)

Sources of estimation uncertainty (extract)

Provisions for liabilities and charges

The Group has made provisions for claims and litigations where it has had to defend itself against proceedings brought by other parties. These provisions have been made for the best estimate of the expected expenditure required to settle each obligation, although there can be no guarantee that such provisions (which may be subject to potentially material revision from time to time) will accurately predict the actual costs and liabilities that may be incurred. The most significant of these litigation provisions is described below.

John Crane, Inc. (JCI), a subsidiary of the Group, is one of many co-defendants in litigation relating to products previously manufactured which contained asbestos. Provision of £220m (FY2023: £204m) has been made for the future defence costs which the Group is expected to incur and the expected costs of future adverse judgements against JCI. Whilst well-established incidence curves can be used to estimate the likely future pattern of asbestos-related disease, JCI’s claims experience is significantly impacted by other factors which influence the US litigation environment. These can include: changing approaches on the part of the plaintiffs’ bar; changing attitudes amongst the judiciary at both trial and appellate levels; and legislative and procedural changes in both the state and federal court systems. Because of the significant uncertainty associated with the future level of asbestos claims and of the costs arising out of the related litigation, there can be no guarantee that the assumptions used to estimate the provision will result in an accurate prediction of the actual costs that will be incurred.

In quantifying the expected costs JCI takes account of the advice of an expert in asbestos liability estimation. The following estimates were made in preparing the provision calculation:

- The period over which the expenditure can be reliably estimated is judged to be ten years, based on past experience regarding significant changes in the litigation environment that have occurred every few years and on the amount of time taken in the past for some of those changes to impact the broader asbestos litigation environment. See note 23 for a sensitivity analysis showing the impact on the provision of reducing or increasing this time horizon; and

- The future trend of legal costs, the rate of future claims filed, the rate of successful resolution of claims, and the average amount of judgements awarded have been projected based on the past history of JCI claims and well-established tables of asbestos incidence projections, since this is the best available evidence. Claims history from other defendants is not used to calculate the provision because JCI’s defence strategy generates a significantly different pattern of legal costs and settlement expenses. See note 23 for a sensitivity analysis showing the range of expected future spend.

23. Provisions and contingent liabilities

The John Crane, Inc. and Titeflex Corporation litigation provisions were the only provisions that were discounted; other provisions have not been discounted as the impact would be immaterial.

Trading

The provisions included as trading represent amounts provided for in the ordinary course of business. Trading provisions are charged and released through headline profit.

Warranty provision and product liability

At 31 July 2024, the Group had warranty and product liability provisions of £9m (FY2023: £6m). Warranties over the Group’s products typically cover periods of between one and three years. Provision is made for the likely cost of after-sales support based on the recent past experience of individual businesses.

Commercial disputes and litigation in respect of ongoing business activities

The Group has on occasion been required to take legal action to protect its intellectual property and other rights against infringement. It has also had to defend itself against proceedings brought by other parties, including product liability and insurance subrogation claims. Provision is made for any expected costs and liabilities in relation to these proceedings where appropriate, although there can be no guarantee that such provisions (which may be subject to potentially material revision from time to time) will accurately predict the actual costs and liabilities that may be incurred.

Contingent liabilities

In the ordinary course of its business, the Group is subject to commercial disputes and litigation such as government price audits, product liability claims, employee disputes and other kinds of lawsuits, and faces different types of legal issues in different jurisdictions. The high level of activity in the US, for example, exposes the Group to the likelihood of various types of litigation commonplace in that country, such as ‘mass tort’ and ‘class action’ litigation, legal challenges to the scope and validity of patents, and product liability and insurance subrogation claims. These types of proceedings (or the threat of them) are also used to create pressure to encourage negotiated settlement of disputes. Any claim brought against the Group (with or without merit) could be costly to defend. These matters are inherently difficult to quantify. In appropriate cases a provision is recognised based on best estimates and management judgement but there can be no guarantee that these provisions (which may be subject to potentially material revision from time to time) will result in an accurate prediction of the actual costs and liabilities that may be incurred. There are also contingent liabilities in respect of litigation for which no provisions are made.

The Group operates in some markets where the risk of unethical or corrupt behaviour is material and has procedures, including an employee ethics alert line, to help it identify potential issues. Such procedures will, from time to time, give rise to internal investigations, sometimes conducted with external support, to ensure that the Group properly understands risks and concerns and can take steps both to manage immediate issues and to improve its practices and procedures for the future. The Group is not aware of any issues which are expected to generate material financial exposures.

Non-headline and legacy

John Crane, Inc.

John Crane, Inc. (JCI) is one of many co-defendants in numerous lawsuits pending in the United States in which plaintiffs are claiming damages arising from alleged exposure to, or use of, products previously manufactured which contained asbestos. Until 2006, the awards, the related interest and all material defence costs were met directly by insurers. In 2007, JCI secured the commutation of certain insurance policies in respect of product liability. Provision is made in respect of the expected costs of defending known and predicted future claims and of adverse judgements in relation thereto, to the extent that such costs can be reliably estimated.

The JCI products generally referred to in these cases consist of industrial sealing products, primarily packing and gaskets. The asbestos was encapsulated within these products in such a manner that causes JCI to understand, based on tests conducted on its behalf, that the products were safe. JCI ceased manufacturing products containing asbestos in 1985.

JCI continues to actively monitor the conduct and effect of its current and expected asbestos litigation, including the most efficacious presentation of its ‘safe product’ defence, and intends to continue to resist these asbestos claims based upon this defence. The table below summarises the JCI claims experience over the last 40 years since the start of this litigation:

The number of claims outstanding at 31 July 2024 reflected the benefit of 2,000 (FY2023: 4,000) claims being dismissed in the year.

JCI has also incurred significant additional defence costs. The litigation involves claims for a number of allegedly asbestos-related diseases, with awards, when made, for mesothelioma tending to be larger than those for the other diseases. JCI’s ability to defend mesothelioma cases successfully is, therefore, likely to have a significant impact on its annual aggregate adverse judgement and defence costs.

John Crane, Inc. litigation provision

The provision is based on past history of JCI claims and well-established tables of asbestos-related disease incidence projections. The provision is determined using advice from asbestos valuation experts, Bates White LLC. The assumptions made in assessing the appropriate level of provision include: the period over which the expenditure can be reliably estimated; the future trend of legal costs; the rate of future claims filed; the rate of successful resolution of claims; and the average amount of judgements awarded. Trial delays arising from the COVID-19 pandemic have largely abated and trial activity has returned to pre-pandemic levels.

Established incidence curves can be used to estimate the likely future pattern of asbestos-related disease. However, JCI’s claims experience is also significantly impacted by other factors which influence the US litigation environment. These can include: changing approaches on the part of the plaintiffs’ bar; changing attitudes amongst the judiciary at both trial and appellate levels in specific jurisdictions which move the balance of risk and opportunity for claimants; and legislative and procedural changes in both the state and federal court systems.

The projections use a limited time horizon on the basis that Bates White LLC consider that there is substantial uncertainty in the asbestos litigation environment. So probable expenditures are not reasonably estimable beyond this time horizon. Asbestos is the longest-running mass tort litigation in American history and is constantly evolving in ways that cannot be anticipated. JCI’s defence strategy also generates a significantly different pattern of legal costs and settlement expenses from other defendants. Thus JCI is in an extremely rare position, and evidence from other litigation cannot be used to improve the reliability of the projections. A ten-year (FY2023: ten-year) time horizon has been used based on past experience regarding significant changes in the litigation environment that have occurred every few years and on the amount of time taken in the past for some of those changes to impact the broader asbestos litigation environment.

The rate of future claims filed has been estimated using well-established tables of asbestos incidence projections to determine the likely population of potential claimants, and JCI’s past experience to determine what proportion of this population will make a claim against JCI. The JCI products generally referred to in claims had industrial and marine applications. As a result, the incidence curve used for JCI projections excludes construction workers, and is a composite of the curves that predict asbestos exposure-related disease from shipyards and other occupations. This is consistent with JCI’s litigation history.

The rate of successful resolution of claims and the average amount of any judgements awarded are projected based on the past history of JCI claims, since this is the best available evidence, given JCI’s strategy of defending all claims.

The future trend of legal costs is estimated based on JCI’s past experience, adjusted to reflect the assumed levels of claims and trial activity, since the number of trials is a key driver of legal costs.

John Crane, Inc. litigation insurance recoveries

While JCI has certain excess liability insurance, JCI has met defence costs directly. The calculation of the provision does not take account of any potential recoveries from insurers.

John Crane, Inc. litigation provision sensitivities

The provision may be subject to potentially material revision from time to time if new information becomes available as a result of future events. There can be no guarantee that the assumptions used to estimate the provision will result in an accurate prediction of the actual costs that will be incurred because of the significant uncertainty associated with the future level of asbestos claims and of the costs arising out of related litigation, including the unpredictability of jury verdicts.

John Crane, Inc. statistical reliability of projections over the ten-year time horizon In order to evaluate the statistical reliability of the projections, a population of outcomes is modelled using randomised verdict outcomes. This generated a distribution of outcomes with future spend at the 5th percentile of £200m and future spend at the 95th percentile of £258m (FY2023: £180m and £245m, respectively). Statistical analysis of the distribution of these outcomes indicates that there is a 50% probability that the total future spend will fall between £245m and £271m (FY2023: between £228m and £257m), compared to the gross provision value of £261m (FY2023: £246m).

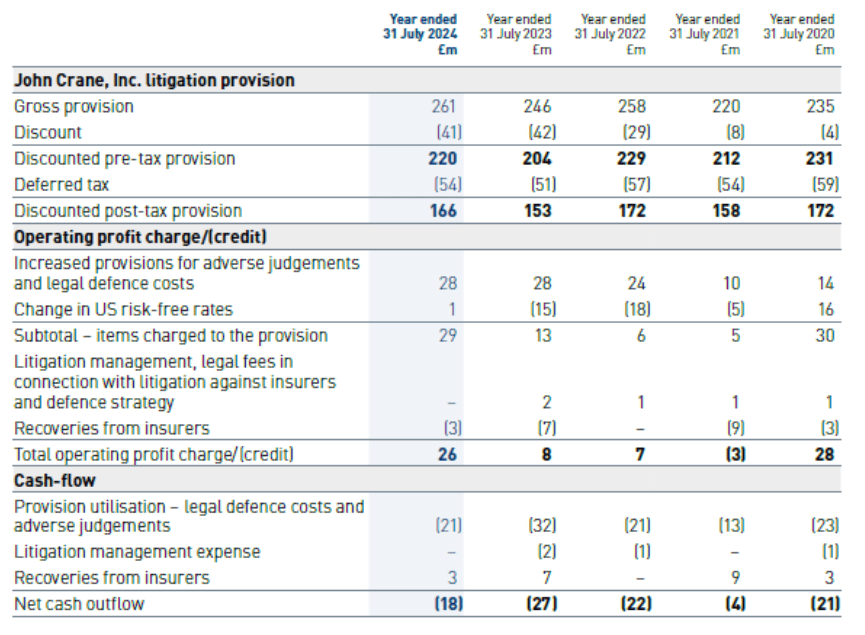

John Crane, Inc. litigation provision history

The JCI asbestos litigation provision of £220m (FY2023: £204m) is a discounted pre-tax provision using discount rates, being the risk-free rate on US debt instruments for the appropriate period. The deferred tax asset related to this provision is shown within the deferred tax balance (note 6).

The JCI asbestos litigation provision has developed over the last five years as follows:

John Crane, Inc. sensitivity of the projections to changes in the time horizon used

If the asbestos litigation environment becomes more volatile and uncertain, the time horizon over which the provision can be calculated may reduce. Conversely, if the environment became more stable, or JCI changed approach and committed to long-term settlement arrangements, the time period covered by the provision might be extended.

The projections use a ten-year time horizon. Reducing the time horizon by one year would reduce the provision by £16m (FY2023: £16m) and reducing it by five years would reduce the provision by £87m (FY2023: £87m).

We consider, after obtaining advice from Bates White LLC, that to forecast beyond ten years requires that the litigation environment remains largely unchanged with respect to the historical experience used for estimating future asbestos expenditures. Historically, the asbestos litigation environment has undergone significant changes more often than every ten years. If one assumed that the asbestos litigation environment would remain unchanged for longer and extended the time horizon by one year, it would increase the pre-tax provision by £13m (FY2023: £13m) and extending it by five years would increase the pre-tax provision by £47m (FY2023: £48m). However, there are also reasonable scenarios that, given certain recent events in the US asbestos litigation environment, would result in no additional asbestos litigation for JCI beyond ten years. At this time, how the asbestos litigation environment will evolve beyond ten years is not reasonably estimable.

John Crane, Inc. contingent liabilities

Provision has been made for future defence costs and the cost of adverse judgements expected to occur. JCI’s claims experience is significantly impacted by other factors which influence the US litigation environment. These can include: changing approaches on the part of the plaintiffs’ bar; changing attitudes amongst the judiciary at both trial and appellate levels; and legislative and procedural changes in both the state and federal court systems. As a result, whilst the Group anticipates that asbestos litigation will continue beyond the period covered by the provision, the uncertainty surrounding the US litigation environment beyond this point is such that the costs cannot be reliably estimated.

Although the methodology used to calculate the JCI litigation provision can in theory be applied to show claims and costs for longer periods, the Directors consider, based on advice from Bates White LLC, that the level of uncertainty regarding the factors used in estimating future costs is too great to provide for reasonable estimation of the numbers of future claims, the nature of such claims or the cost to resolve them for years beyond the ten-year time horizon.

Titeflex Corporation

Titeflex Corporation, a subsidiary of the Group in the Flex-Tek business segment, has received a number of claims in the US from insurance companies seeking recompense on a subrogated basis for the effects of damage allegedly caused by lightning strikes in relation to its flexible gas piping product. It has also received product liability claims regarding this product in the US, some in the form of purported class actions. Titeflex Corporation believes that its products are a safe and effective means of delivering gas when installed in accordance with the manufacturer’s instructions and local and national codes. However, some claims have been settled on an individual basis without admission of liability. Equivalent third-party products in the US marketplace face similar challenges.

Titeflex Corporation litigation provision

The continuing progress of claims and the pattern of settlement, together with recent marketplace activity, provide sufficient evidence to recognise a liability in the accounts. Therefore provision has been made for the costs which the Group is expected to incur in respect of future claims to the extent that such costs can be reliably estimated. Titeflex Corporation sells flexible gas piping with extensive installation and safety guidance designed to assure the safety of the product and minimise the risk of damage associated with lightning strikes.

The assumptions made in assessing the appropriate level of provision, which are based on past experience, include: the period over which expenditure can be reliably estimated; the number of future settlements; the average amount of settlements; and the impact of statutes of repose and safe installation initiatives on the expected number of future claims. The assumptions relating to the number of future settlements exclude the use of recent claims history due to the uncertain impact that the COVID-19 lockdown has had on the number of claims.

The provision of £36m (FY2023: £41m) is a discounted pre-tax provision using discount rates, being the risk-free rate on US debt instruments for the appropriate period. The deferred tax asset related to this provision is shown within the deferred tax balance (note 6).

Titeflex Corporation litigation provision history

A credit of £5m (FY2023: £8m credit) has been recognised by Titeflex Corporation in respect of changes to the estimated cost of future claims from insurance companies seeking recompense for damage allegedly caused by lightning strikes. The lower gross provision value has been principally driven by a reduction in the number of claims.

Titeflex Corporation litigation provision sensitivities

The significant uncertainty associated with the future level of claims and of the costs arising out of related litigation means that there can be no guarantee that the assumptions used to estimate the provision will result in an accurate prediction of the actual costs that will be incurred. Therefore the provision may be subject to potentially material revision from time to time, if new information becomes available as a result of future events.

The projections incorporate a long-term assumption regarding the impact of safe installation initiatives on the level of future claims. If the assumed annual benefit of bonding and grounding initiatives were 0.5% higher, the provision would be £2m (FY2023: £2m) lower, and if the benefit were 0.5% lower, the provision would be £2m (FY2023: £2m) higher.

The projections use assumptions of future claims that are based on both the number of future settlements and the average amount of those settlements. If the assumed average number of future settlements increased 10%, the provision would rise by £2m (FY2023: £3m), with an equivalent fall for a reduction of 10%. If the assumed amount of those settlements increased 10%, the provision would rise by £2m (FY2023: £2m), also with an equivalent fall for a reduction of 10%.

Other non-headline and legacy provisions

Non-headline provisions comprise all provisions that were disclosed as non-headline items when they were charged to the consolidated income statement. Legacy provisions comprise non-material provisions relating to former business activities and discontinued operations and properties no longer used by Smiths.

These non-material provisions include non-headline reorganisation, disposal indemnities, litigation and arbitration in respect of old products and discontinued business activities, which includes claims received in connection with the disposal of Smiths Medical. Provision is made for the best estimate of the expected expenditure related to the defence and/or resolution of such matters. There is an inherent risk in legal proceedings that the outcome may be unfavourable to the Group, and as such there can be no guarantee that such provisions (which may be subject to potentially material revision from time to time) will be sufficient.

Reorganisation

At 31 July 2024, there were reorganisation provisions of £1m (FY2023: £7m) relating to the various restructuring programmes that are expected to be utilised in the next 18 months.

Property

At 31 July 2024, there were provisions of £6m (FY2023: £10m) related to actual and potential environmental issues for sites currently or previously occupied by Smiths operations.