Rio Tinto plc – Annual report – 31 December 2023

Industry: mining

i. New standards issued and effective in the current year (extract)

Deferred Tax related to Assets and Liabilities arising from a Single Transaction (Amendments to IAS 12 “Income Taxes”), mandatory in 2023 and endorsed by the UK)

At 1 January 2023, we adopted narrow-scope amendments to IAS 12 and have restated comparative periods in accordance with the transition arrangements. These amendments introduce an exception to the initial recognition exemption application for transactions giving rise to equal and offsetting taxable and deductible temporary differences.

Under the amendments, separate deferred tax assets and liabilities are calculated and recognised, prior to application of any required recovery testing and permitted offsetting, and subsequent movements in those deferred tax assets and liabilities are recognised in the income statement. Our previous accounting policy stated that “where the recognition of an asset and liability from a single transaction gives rise to equal and offsetting temporary differences, we apply the initial recognition exemption allowed by IAS 12, and consequently recognise neither a deferred tax asset nor a deferred tax liability in respect of these temporary differences”.

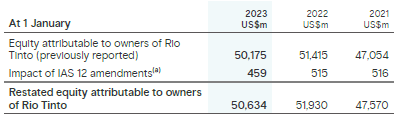

The most significant impact of implementing these amendments is from temporary differences related to the Group’s provisions for close-down and restoration, and lease obligations and corresponding capitalised closure costs and right-of-use assets. Adjustments to deferred tax assets and liabilities related to these balances have been recognised as at 1 January 2021, being the beginning of the earliest comparative period to be presented in the financial statements for the year ended 31 December 2023, with the cumulative effect recognised as an adjustment to retained earnings or other components of equity at that date. For other transactions, the impact of which was immaterial, the amendments apply only to those taking place on or after 1 January 2021. The impact on equity attributable to owners of Rio Tinto at 1 January 2023 of implementing the amendments to IAS 12 is as follows:

(a) Retained earnings adjustments at 1 January 2023 and 2022 include the impact of income statement adjustments for the years ended 31 December 2022 and 2021, respectively.

The restatement of deferred tax balances for the comparative reporting date is as follows:

Restatement of pre-offset balances at 31 December 2022 represents additional gross deferred tax liabilities of US$922 million and gross deferred tax assets of US$1,380 million in relation to close-down and restoration obligations and related capitalised closure costs, and additional gross deferred tax liabilities of US$140 million and gross deferred tax assets of US$149 million in relation to lease liabilities and related right-of-use assets.

The impact of restatement on net earnings for the years ended 31 December 2021 and 31 December 2022 were a net credit of US$22 million and net charge of US$28 million, respectively, related to depreciation of closure and right of use assets and settlement of closure and lease liabilities.