GN Store Nord A/S – Annual report – 31 December 2025

Industry: manufacturing

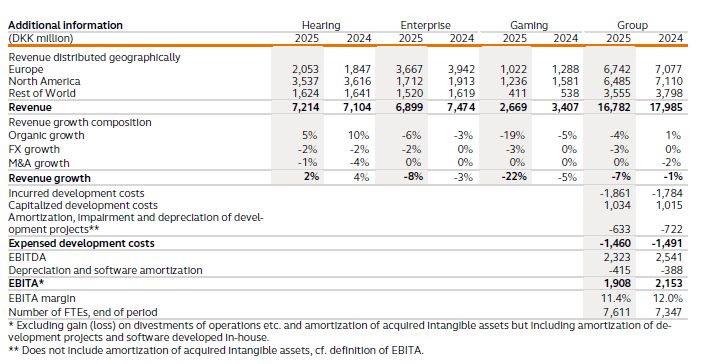

2025 segment disclosures (extract)

3.1 Intangible assets (extract)

Accounting policies (extract)

Development projects, Software, Patents, Licenses and Other Intangible Assets

Intangible assets are measured at cost less accumulated amortization and impairment. Amortization is provided on a straight-line basis over the expected useful lives of the assets. When changing the depreciation period, the effect on the depreciation is recognized prospectively as a change in accounting estimates. Amortization and impairment is recognized in the income statement as production costs, development costs, distribution costs and administrative expenses.

The expected useful lives are as follows:

2025

Completed development projects 1-5 years

Software 3-10 years

Customer relationships up to 10 years

Patents, licenses, trademarks and other intellectual property rights up to 20years

Development projects that are clearly defined and identifiable, where the technical utilization degree, sufficient resources and a potential future market or development opportunities in the Company is evidenced, and where Group intends to produce, market or use the project, are recognized as intangible assets if it is probable that costs incurred will be covered by future earnings. The cost of such development projects includes direct wages, salaries, materials and other direct and indirect costs attributable to the development projects. Amortization and write-down of such capitalized development projects are started at the date of completion and are included in development costs. Other development costs are recognized in the income statement as incurred.

Gains or losses on the disposal of intangible assets are determined as the difference between the selling price less selling costs and the carrying amount at the disposal date and are recognized in the income statement as other operating income or other operating costs, respectively.

Key accounting estimates

Valuation of intangible assets – development projects

Development projects are measured at cost less accumulated amortization and impairment. An impairment test is performed of the carrying amount of recognized development projects. The impairment test is based on assumptions regarding strategy, product lifecycle, market conditions, discount rates and budgets, etc., after the project has been completed and production has commenced. If market-related assumptions, etc., are changed, development projects may have to be written down. Management examines and assesses the underlying assumptions when determining whether or not the carrying amount should be written down.