Trinity Mirror plc – Annual report – 31 December 2017

Industry: publishing

Directors’ report (extract)

Dividends and share buyback

The Board proposes a final dividend for 2017 of 3.55 pence per share (2016: 3.35 pence per share) which, subject to shareholder approval, will be payable on 8 June 2018 to shareholders on the register on 11 May 2018. The proposed final dividend together with the interim dividend of 2.25 pence per share (2016: 2.10 pence per share) results in a total dividend for 2017 of 5.80 pence per share (2016: 5.45 pence per share).

On 1 August 2016 the Group announced a Share Repurchase Programme of the Company’s 10p Ordinary Shares, up to a maximum consideration of £10 million. The purpose of the Share Repurchase Programme was to reduce the Company’s share capital, with the repurchased shares being held in Treasury. The Share Repurchase Programme, which completed on 14 November 2017, repurchased 10,017,620 10p Ordinary shares with an aggregate nominal value of £1,001,762, representing 3.53% of the issued share capital of the Company.

Treasury shares do not receive dividends and are not included when calculating the total voting rights in the Company. The Company, if deemed fit, can sell the shares for cash or transfer the shares for use in an employee share scheme. The Company intends to hold the repurchased shares in Treasury for the foreseeable future.

Dividend Policy

As the Group continues to manage the business through the structural challenges facing print media the Board has adopted a progressive dividend policy that is aligned to free cash generation of the business. The free cash generation for the purposes of assessing the dividend is the net cash flow generated by the Group before the repayment of debt, dividend payments, other capital returns to shareholders and additional contributions made to the defined benefit pension schemes as a result of a substantial increase in dividends and/or capital returns to shareholders. When setting the level of dividends the Board will ensure that the Group maintains adequate headroom for investment and any unexpected cash flow requirements for historical events or to fund further restructuring. Based on the Board’s expectation of future cash flows the Board expects dividends to increase by at least 5% per annum.

The Company will also continue to consider, if appropriate, the return of capital to shareholders through a share buyback if it has generated surplus cash and sees an opportunity to enhance earnings per share and therefore shareholder value. Prior to initiating a share buyback programme the Company will carefully consider the cash generation of the business and the Group’s obligations to the Group’s defined benefit pension schemes.

The risks associated with the delivery of the dividend policy are as follows:

- The availability of distributable reserves: In 2014, as a result of an impairment of the carrying value of investments held by the Company were impaired and this resulted in a negative balance on the profit and loss reserve and therefore the Company had no distributable reserves. This was addressed by undertaking a court approved capital reduction to eliminate the negative balance in the profit and loss reserve and thereafter the distributable reserves have been re built through dividends received from subsidiary companies from profits. The Company would undertake a similar exercise in the future if such an event was to occur, as it still has a £606.7 million balance on the share premium account;

- A significant fall in profits and cash flows which materially reduces free cash flow: Under these circumstances the Group would review all the investment requirements, pension obligations and future debt payments. In such circumstances we would seek to hold dividends unless it would place increased pressure on the ability of the Group to fund investment to deliver its strategy or if it was to create any financing issues; and

- The payment of dividends would potentially restrict the ability of the Group to meet payments due under the recovery plans agreed with the Group’s defined benefit pension schemes: The Group agrees recovery plans with the Trustees of the Group’s defined benefit pension schemes at each triennial valuation and these may be revised as a result of material corporate activity. The Group has also agreed that additional contributions will be made to the schemes in the event dividends are increased by more than 10% in any one year. The additional contributions to the defined benefit pension schemes will be equivalent to at least 75% of the amount by which dividend payments are more than the amount they would have been if dividends had been increased by 10%. Further, the Group has agreed that dividend payments or any other return of capital to shareholders in any year will not be in excess of payments to the defined benefit pension schemes to address past deficits. These obligations may restrict future increases in dividends.

Notes to the parent company financial statements (extract)

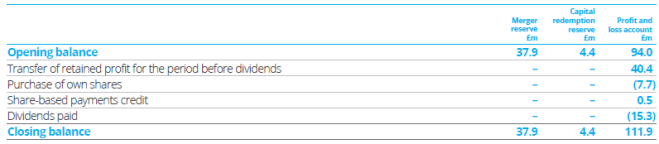

11 Other reserves

The merger reserve comprises the premium on the shares allotted in relation to the acquisition of Local World net of £0.8 million of issue costs. The capital redemption reserve represents the nominal value of the shares purchased and subsequently cancelled as part of share buyback programmes. The profit and loss account reserves are all distributable.