HSBC Holdings plc – Annual report – 31 December 2025

Industry: banking

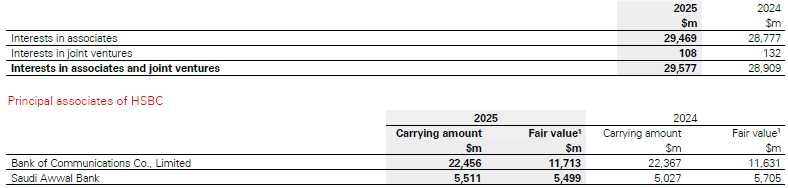

18 Interests in associates and joint ventures

1 Principal associates are listed on recognised stock exchanges. The fair values are based on the quoted market prices of the shares held (Level 1 in the fair value hierarchy).

1 The Group’s interest in Bank of Communications Co., Limited (‘BoCom’) reduced from 19.03% to 16.00% following the completion of a capital issuance by BoCom on 17 June 2025. There has been no percentage change in HSBC’s shareholding interest in the Saudi Awwal Bank when compared with 2024.

A list of all associates and joint ventures is set out in Note 38.

Bank of Communications Co., Limited

The results for the period ended 31 December 2025 included a $1.1bn loss from the dilution of our shareholding and a $1.0bn impairment to the carrying amount of the Group’s interest in BoCom.

The Group’s interest in BoCom reduced from 19.03% to 16.00% following the completion of a capital issuance by BoCom on 17 June 2025. The dilution of the Group’s interest resulted in a pre-tax loss of $1.1bn, recognised in ‘Other operating income/(expense)’ in the Group’s consolidated income statement. The loss is not deductible for tax purposes as a consequence of our shareholding in BoCom being held for long-term investment purposes.

In addition, the Group’s impairment test on the carrying amount at 30 June 2025 resulted in an impairment of $1.0bn, as the recoverable amount as determined by a value-in-use calculation was lower than the carrying amount. The impairment was recognised within ‘Impairment of interest in associate’. Consistent with prior periods, our value-in-use (‘VIU’) calculation uses both historical experience and market participant views to estimate future cash flows, relevant discount rates and associated capital assumptions. No further impairment (or reversal) was required for the period from 1 July 2025 to 31 December 2025 based on results of the quarterly impairment tests performed.

The impacts of the capital issuance have been incorporated in both the carrying amount and the VIU. The VIU assumptions incorporate updated expectations, taking into account both the impact of the capital issuance on BoCom’s financial position, and the latest macroeconomic, policy and industry factors in mainland China.

We remain strategically committed to mainland China and continue our valued, strategic partnership with BoCom.

HSBC’s Interest

The Group’s investment in BoCom continues to be classified as an associate. Significant influence in BoCom was established with consideration of all relevant factors, including the Group’s latest shareholding, representation on BoCom’s Board of Directors, and participation in a resource and experience sharing agreement (‘RES’). Under the RES, HSBC staff have been seconded to assist in the maintenance of BoCom’s financial and operating policies. Investments in associates are recognised using the equity method of accounting in accordance with IAS 28 ‘Investments in Associates and Joint Ventures’, whereby the investment is initially recognised at cost and adjusted thereafter for the post-acquisition change in the Group’s share of associate’s net assets. An impairment test is required if there is any indication of impairment or reversal.

The fair value of the Group’s investment in BoCom had been below its carrying amount. No impairment (or reversal) was required for the year ended 31 December 2024.

If the Group did not have significant influence in BoCom, the investment would be carried at fair value rather than the current carrying amount.

Impairment testing

The Group’s impairment test at 30 June 2025 concluded that there were indications of impairment. As part of this assessment, an impairment test on the carrying amount with an updated VIU calculation was performed which resulted in an impairment of $1.0bn, as the recoverable amount as determined by the VIU calculation was lower than the carrying amount. The impairment was recognised within ‘Impairment of interest in associate’. The impairment loss is not deductible for tax purposes.

At 31 December 2025, no further impairment (or reversal) was required and the investment had a carrying amount of $22.5bn (2024: $22.4bn) and a fair value of $11.7bn (2024: $11.6bn).

Basis of recoverable amount

The VIU calculation uses discounted cash flow projections based on management’s best estimates of future earnings available to ordinary shareholders prepared in accordance with IAS 36 ’Impairment of Assets’. Those cash flows used estimates based on BoCom’s current condition and so do not include estimated cash flows arising from uncommitted future actions that may affect the performance of the investment which will be considered at the relevant time should they arise. Significant management judgement is required in arriving at the best estimate.

The VIU may increase or decrease depending on the effect of changes to model inputs. The main model inputs are described below and are based on factors observed at period-end. The factors that could result in increases or reductions in the VIU include changes in BoCom’s short-term performance, a change in regulatory capital requirements or revisions to the forecast of BoCom’s future profitability.

There are two main components to the VIU calculation. The first component is management’s best estimate of BoCom’s earnings. Forecast earnings growth over the short to medium term continues to be lower than recent (within the last five years) actual growth, and reflects the impact of recent macroeconomic, policy and industry factors in mainland China. As a result of management‘s intent to continue to retain its investment for the long term, earnings beyond the short to medium term are extrapolated into perpetuity using a long-term growth rate to derive a terminal value, which comprises the majority of the VIU. The second component is the capital maintenance charge (‘CMC’), which is management’s forecast of the earnings that need to be withheld in order for BoCom to meet capital requirements over the forecast period, meaning that CMC is deducted when arriving at management’s estimate of future earnings available to ordinary shareholders. The CMC reflects the revised capital requirements arising from revisions of the ratio of risk-weighted assets to total assets assumption. The principal inputs to the CMC calculation include estimates of asset growth, the ratio of risk-weighted assets to total assets and the expected capital requirements. An increase in the CMC as a result of a change to these principal inputs would reduce VIU. Additionally, management considers other qualitative factors, to ensure that the inputs to the VIU calculation remain appropriate.

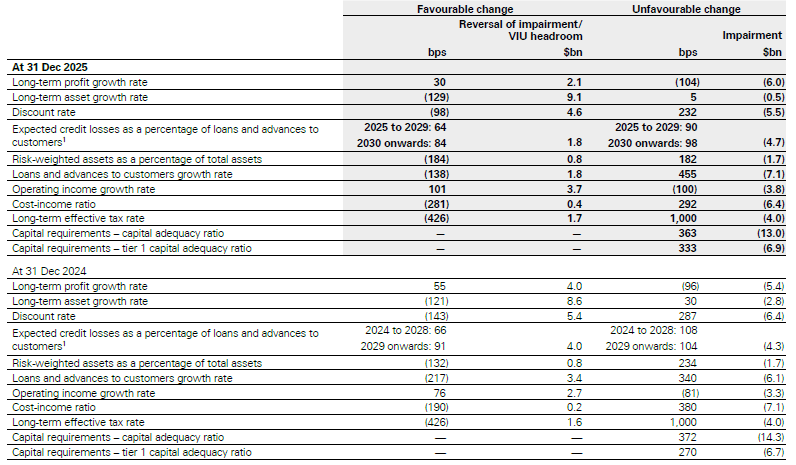

Key assumptions in value in use calculation

We used a number of assumptions in our VIU calculation, in accordance with the requirements of IAS 36:

- Long-term profit growth rate: 3.00% (2024: 3.00%) for periods after 2029, which does not exceed forecast GDP growth in mainland China and is similar to forecasts by external analysts.

- Long-term asset growth rate: 3.25% (2024: 3.25%) for periods after 2029, which is the rate that assets are expected to grow to achieve long-term profit growth of 3.00%.

- Discount rate: 8.08% (2024: 8.53%), which is based on a capital asset pricing model (‘CAPM’), using market data. The discount rate used is within the range of 7.1% to 8.7% (2024: 7.1% to 8.8%) indicated by the CAPM, and decreased primarily as a consequence of a market-driven reduction in the risk-free rate.

- Expected credit losses (‘ECL’) as a percentage of loans and advances to customers: ranges from 0.67% to 0.87% (2024: 0.74% to 0.93%) in the short to medium term, reflecting reported credit experience in mainland China. For periods after 2029, the ratio is 0.87% (2024: 0.97%), reflecting the anticipated continuation of BoCom’s lower average ECL as a percentage of loans and advances to customers experienced in recent years.

- Risk-weighted assets as a percentage of total assets: ranges from 62.0% to 64.2% (2024: 62.0% to 62.5%) in the short to medium term, reflecting higher risk-weights in the short term followed by an expected reversion to recent historical levels. For periods after 2029, the ratio is 62.0% (2024: 62.0%), which continues to be similar to BoCom’s actual results in recent years.

- Loans and advances to customers growth rate: ranges from 7.5% to 8.0% (2024: 7.5% to 9.5%) in the short to medium term, which is similar to BoCom’s actual results in recent years. Decreases in the forecast growth rate of loans and advances to customers result in lower forecast ECL.

- Operating income growth rate: ranges from 0.5% to 7.4% (2024: 0.1% to 9.9%) in the short to medium term, which is similar to BoCom’s actual results in recent years. The projected net interest income over the short to medium term reduced to reflect expected pressure on net interest margin compared with the prior period, which led to a net reduction in the VIU.

- Cost-income ratio: ranges from 34.8% to 40.0% (2024: 34.6% to 39.8%) in the short to medium term. These ratios are similar to BoCom’s actual results in recent years.

- Long-term effective tax rate: 15.0% (2024: 15.0%) for periods after 2029, which is higher than the recent historical average, and aligned to the minimum tax rate as proposed by the OECD/Group of 20 (‘G20’) Inclusive Framework on Base Erosion and Profit Shifting.

- Capital requirements: capital adequacy ratio of 12.5% (2024: 12.5%) and tier 1 capital adequacy ratio of 9.5% (2024: 9.5%), based on BoCom’s capital risk appetite and capital requirements respectively.

The following table illustrates the impact on the carrying amount of reasonably possible changes to key assumptions used in the VIU calculation. This reflects the sensitivity of each key assumption on its own and it is possible that more than one favourable and/or unfavourable change may occur at the same time. The selected rates of reasonably possible changes to key assumptions are based on external analysts’ forecasts, statutory requirements and other relevant external data sources, which can change period to period. Unless specified, favourable and unfavourable changes are consistently applied throughout short-to-medium and long-term forecast years, based on a straight-line average of the base case assumption.

Sensitivity of the carrying amount to the key VIU assumptions

1 The expected credit losses as a percentage of loans and advances to customers reflect selected favourable and unfavourable rates.

Considering the interrelationship of the changes set out in the table above, management estimates that the reasonably possible range of VIU is $13.4bn to $31.0bn (2024: $13.5bn to $30.8bn), acknowledging that the fair value of the Group’s investment has ranged from $7.5bn to $13.1bn over the last five years as at the date of the impairment tests. The possible range of VIU is based on impacts set out in the table above arising from the favourable/unfavourable change in the operating income in the short to medium term, the expected credit losses as a percentage of loans and advances to customers, and a 50bps increase/decrease in the discount rate. All other long-term assumptions, and the basis of the CMC have been kept unchanged when determining the reasonably possible range of the VIU.

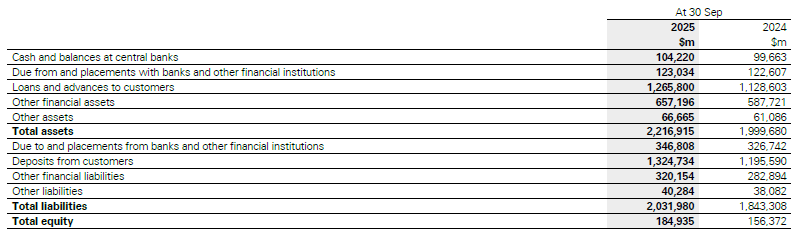

Selected financial information of BoCom

The statutory accounting reference date of BoCom is 31 December. For the year ended 31 December 2025, HSBC included the associate’s results on the basis of the financial statements for the 12 months ended 30 September 2025, taking into account any known changes in the subsequent period from 1 October 2025 to 31 December 2025 that would have materially affected the results.

Selected balance sheet information of BoCom

Reconciliation of BoCom’s total shareholders’ equity to the carrying amount in HSBC’s consolidated financial statements

1 This balance includes goodwill originally arising on acquisition and reflects the impacts from the dilution of our shareholding in BoCom as well as BoCom’s interim dividend for the six months ended 30 June 2025.

2 This balance includes the impact of foreign exchange movements.

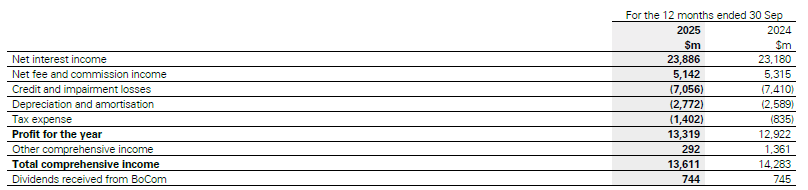

Selected income statement information of BoCom

Saudi Awwal Bank

The Group’s investment in Saudi Awwal Bank (‘SAB’) is classified as an associate. HSBC is the largest shareholder in SAB with a shareholding of 31%. Significant influence in SAB is established via representation on the Board of Directors. Investments in associates are recognised using the equity method of accounting in accordance with IAS 28, as described previously for BoCom.

Impairment testing

The fair value of the Group’s investment in SAB was marginally below the carrying amount as at 31 December 2025. An impairment test on the carrying amount with a VIU calculation was performed. The recoverable amount as determined by the VIU calculation was higher than the carrying amount using discounted cash flow projections. SAB has also had increasing profits each year. On that basis, the Group has concluded there is no indication of impairment.

The VIU calculation was based on management’s best estimates of future earnings available to ordinary shareholders prepared in accordance with IAS 36 ‘Impairment of Assets’. Those cash flows used estimates based on SAB’s current condition and so do not include estimated cash flows arising from uncommitted future actions that may affect the performance of the investment, which will be considered at the relevant time should they arise.