CRH plc – Annual report – 31 December 2022

Industry: construction, distribution

Accounting Policies (extract)

Leases – Notes 13 and 20

The Group enters into leases for a range of assets, principally relating to property. These property leases have varying terms, renewal rights and escalation clauses, including periodic rent reviews linked with a consumer price index and/or other indices. The Group also leases plant and machinery, vehicles and equipment. The terms and conditions of these leases do not impose significant financial restrictions on the Group.

A contract contains a lease if it is enforceable and conveys the right to control the use of a specified asset for a period of time in exchange for consideration, which is assessed at inception. A right-of-use asset and lease liability are recognised at the commencement date for contracts containing a lease, with the exception of leases with a term of 12 months or less which do not contain a purchase option, leases where the underlying asset is of low value and leases with associated payments that vary directly in line with usage or sales. The commencement date is the date at which the asset is made available for use by the Group.

The lease liability is initially measured at the present value of the future lease payments, discounted using the incremental borrowing rate or the interest rate implicit in the lease, if this is readily determinable, over the remaining lease term. Lease payments include fixed payments less any lease incentives receivable, variable payments that are dependent on a rate or index known at the commencement date, amounts expected to be paid under residual value guarantees and any payments for an optional renewal period and purchase and termination option payments, if the Group is reasonably certain to exercise those options. The lease term is the non-cancellable period of the lease adjusted for any renewal or termination options which are reasonably certain to be exercised.

Variable lease payments that do not depend on an index or a rate and rentals relating to low value or short-term leases are recognised as an expense in the period in which they are incurred. Management applies judgement in determining whether it is reasonably certain that a renewal, termination or purchase option will be exercised.

Incremental borrowing rates are calculated using a portfolio approach, based on the risk profile of the entity holding the lease and the term and currency of the lease.

After initial recognition, the lease liability is measured at amortised cost using the effective interest method. It is remeasured when there is a change in future lease payments or when the Group changes its assessment of whether it is reasonably certain to exercise an option within the contract. A corresponding adjustment is made to the carrying amount of the right-of-use asset.

The right-of-use asset is initially measured at cost, which comprises the lease liability adjusted for any payments made at or before the commencement date, initial direct costs incurred, lease incentives received and an estimate of the cost to dismantle or restore the underlying asset or the site on which it is located at the end of the lease term. The right-of-use asset is depreciated over the lease term or, where a purchase option is reasonably certain to be exercised, over the useful economic life of the asset in line with depreciation rates for owned property, plant and equipment. The right-of-use asset is tested periodically for impairment if an impairment indicator is considered to exist.

Non-lease components in a contract such as maintenance and other service charges are separated from lease payments and are expensed as incurred.

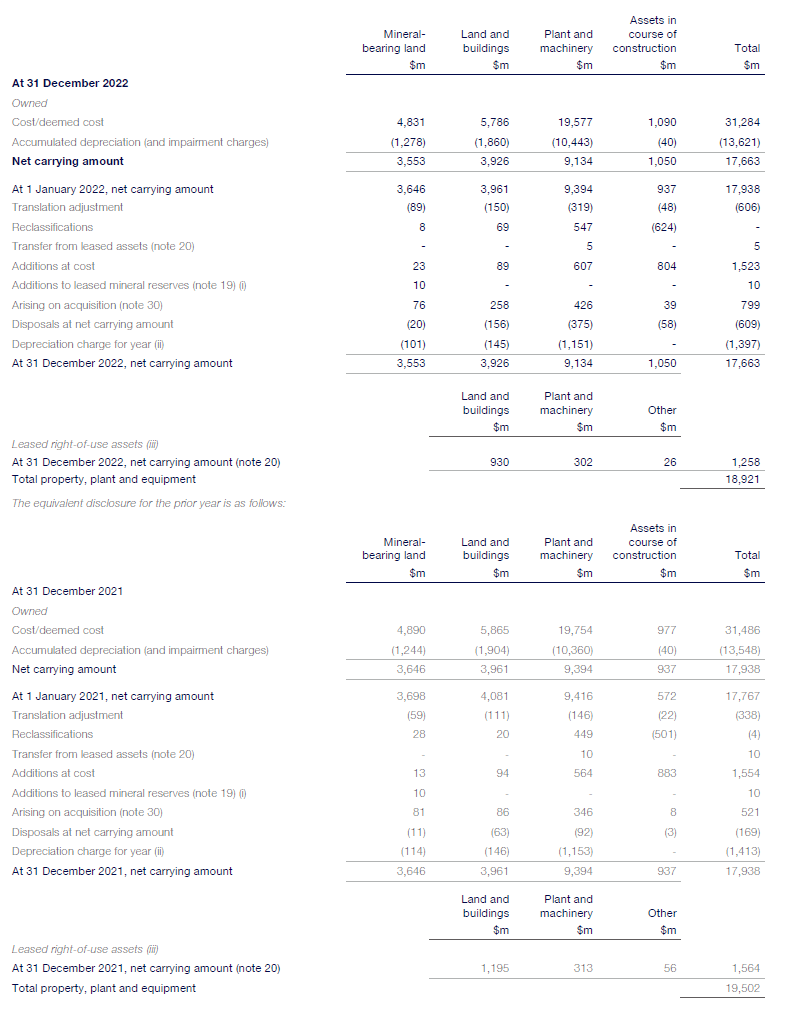

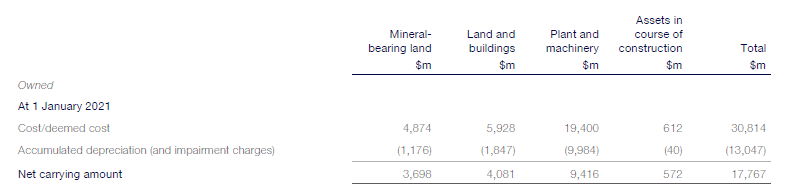

13. Property, Plant and Equipment

(i) Additions relating to leased mineral reserves which fall outside the scope of IFRS 16.

(ii) The depreciation charge includes $15 million (2021: $44 million; 2020: $41 million) relating to discontinued operations.

(iii) See note 20 for more detailed information on right-of-use assets and lease liabilities of the Group.

Climate risk and impairment of property, plant and equipment

Property, plant and equipment (PP&E) is reviewed for potential impairment by applying a series of external and internal indicators including climate-related risks. Specific climate-related considerations during 2022 included:

- considering potential future business optimisation levers that may occur and the impact on useful lives;

- assessing the useful lives of transport and mobile equipment in the context of decarbonisation of our transport and mobile equipment, this being identified as one of our decarbonisation roadmap levers. It is assumed that transport and mobile equipment will be transitioned to lower carbon emitting units in line with normal asset retirement timelines;

- assessing the impact of the capital expenditure required to meet the Group’s carbon emissions reduction targets on the useful lives of existing PP&E. The nature of the proposed projects required to deliver our targets, including technology advancements, and their impact on existing PP&E was also considered; and

- assessing the impact of physical risk to PP&E, in the context of the exposure of the Group’s locations to potential future adverse weather impacts

Capital expenditure will continue to be required to deliver our targets and mitigate potential physical risks. Therefore, the useful lives of future capital expenditure may differ from current assumptions. However, as a result of the assessments set out above, there were no significant changes in the estimates of useful lives or asset values during the current financial year.

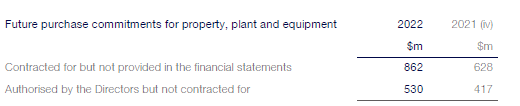

(iv) Includes contracted for but not provided for and authorised by the Directors but not contracted for commitments of $11 million and $25 million respectively relating to discontinued operations.

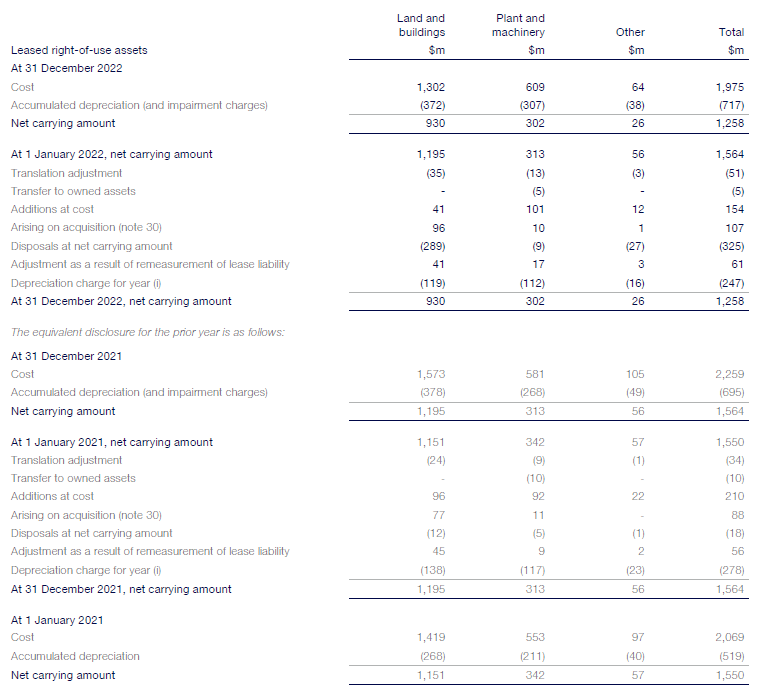

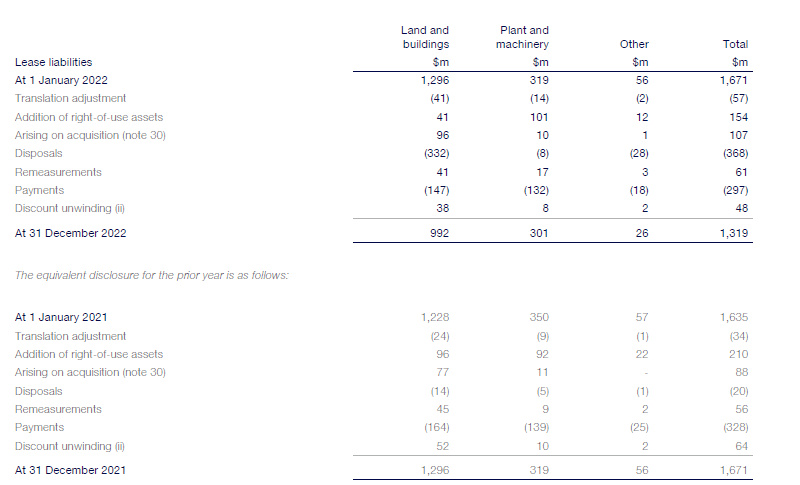

20. Leases

(i) The depreciation charge includes $11 million (2021: $34 million; 2020: $33 million) relating to discontinued operations.

(ii) Discount unwinding includes $6 million (2021: $18 million; 2020: $19 million) relating to discontinued operations.

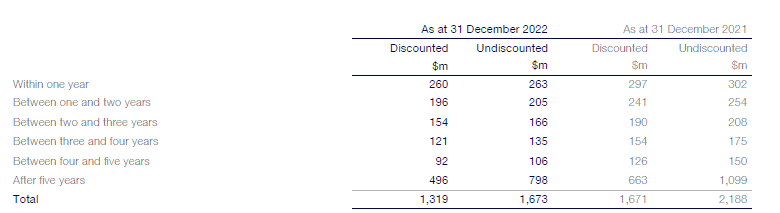

The table below shows a maturity analysis of the discounted and undiscounted lease liability arising from the Group’s leasing activities. The projections are based on the foreign exchange rates applying at the end of the relevant financial year and on interest rates (discounted projections only) applicable to the lease portfolio.

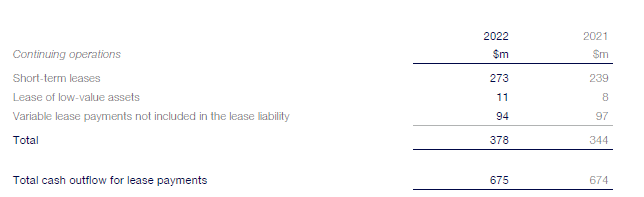

The Group avails of the exemption from capitalising lease costs for short-term leases and low-value assets where the relevant criteria are met. Variable lease payments directly linked to sales or usage are also expensed as incurred. The following lease costs have been charged to the Consolidated Income Statement as incurred:

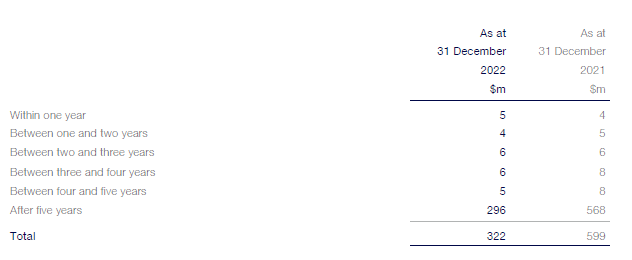

Lease commitments for short-term leases are similar to the portfolio of short-term leases for which the costs, as above, were expensed to the Consolidated Income Statement. The effect of excluding future cash outflows arising from variable lease payments, termination options, residual value guarantees and leases not yet commenced from lease liabilities was not material for the Group. The potential undiscounted future cash outflows arising from the exercise of renewal options that are not expected to be exercised (and are therefore not included in the lease term) are as follows:

Income from subleasing and gains/losses on sale and leaseback transactions were not material for the Group.