easyJet plc – Annual report – 30 September 2025

Industry: transport

1A. MATERIAL ACCOUNTING POLICIES (extract)

Leases

The Group assesses at contract inception whether a contract is, or contains, a lease.

The Group as lessee

When a contractual arrangement contains a lease, easyJet recognises a lease liability and a corresponding right of use asset at the commencement of the lease.

At the commencement date the lease liability is measured at the present value of the future lease payments, discounted using the Group’s incremental borrowing rate where the interest rate in the lease is not readily determined. Lease payments include fixed payments and variable payments which are dependent on an index or rate. Where an index or rate is used this is initially measured using the index or rate at commencement. Subsequently, the lease liability is adjusted by increasing the carrying amount to reflect interest on the lease liability, reducing the carrying amount to reflect the lease payments made, and remeasuring the carrying amount to reflect any reassessment or lease modifications.

The lease term is determined from the commencement date of the lease and the duration of the non-cancellable term. If easyJet has an extension option, which it considers it is reasonably certain to exercise, then the lease term will be considered to extend beyond that non-cancellable period to the end of the extension period available. Where easyJet has previously assessed that there is no intention to exercise an extension option but subsequently opts to exercise the option, then the lease liability is remeasured for the revised lease term and change in future lease payments. If easyJet has a termination option, which it considers it is reasonably certain to exercise, then the lease term will be accounted for until the point when the termination option will take effect.

At the commencement date the right of use asset is measured at an amount equal to the lease liability plus any lease payments made before the commencement date and any initial direct costs, less any lease incentive payments received. An estimate of costs to be incurred in restoring an asset before return to the lessor, in accordance with the terms of the lease, is also included in the right of use asset at initial recognition. Subsequently, for leased aircraft, the right of use asset attracts maintenance work in accordance with the contractual obligations of the lease, and a provision for the maintenance work is built up as the aircraft is flown, with the offset being against the right of use asset. The maintenance asset created is immediately fully depreciated as the liability is incurred as the aircraft is flown. Additionally, in the event that a corresponding lease liability is remeasured, an adjustment is also made to the right of use asset. The right of use assets form part of the Airline CGU and are therefore subject to review for impairment annually or when there is an indication of impairment within the Airline CGU.

Short-term leases less than 12 months in length and low-value leases are not recognised as lease liabilities and right of use assets but are recognised as an expense on a straight-line basis over the lease term.

In the consolidated statement of cash flows, payments for the interest element of recognised lease liabilities are included in interest and other financing charges paid within cash flows from operating activities. Payments for the principal element of recognised lease liabilities are presented within cash flows from financing activities.

Sale and leaseback

easyJet periodically enters into sale and leaseback transactions whereby it sells either new or mid-life aircraft or engines to a third-party and immediately leases them back. Each transaction is assessed as to whether a sale of the asset has occurred under IFRS 15, ‘Revenue from Contracts with Customers’, taking into consideration whether the contract contains a substantive purchase option for easyJet to repurchase the asset.

If a sale of the asset is determined to have occurred, the asset is derecognised and a right of use asset and lease liability are recognised. Where the transaction is judged to reflect the assets fair value, any gain or loss arising on disposal is recognised in the income statement, to the extent that it relates to the rights that have been transferred. Gains and losses that relate to the rights that have been retained are included in the carrying amount of the right of use asset recognised at commencement of the lease. If sale proceeds received were determined to not be at the asset’s fair value, any below market terms would be recognised as a prepayment of lease payments, and above market terms recognised as additional financing provided by the lessor. Gains on sale and leaseback transactions are recognised in other income, with losses on sale and leaseback transactions recognised in other costs. Proceeds received for the sale of the fair value of the asset are recognised in the statement of cash flows within investing activities as it relates to property, plant and equipment.

If a sale is determined to have not occurred, then the contract is not accounted for as a lease. The asset is retained on the consolidated statement of financial position within property, plant and equipment and a financial liability is recognised within other borrowings for the sale proceeds received. The financial liability is recognised at amortised cost as detailed in the financial instruments policy.

Purchase of leased assets

Where easyJet acquires an asset that was previously leased to the Group, and the original lease contract did not contain a purchase option, the asset is recognised within property, plant and equipment at fair value. The difference between the fair value and the purchase consideration paid is recognised in the income statement together with the derecognition of the right of use asset, lease liability and associated maintenance and restoration provisions. Payments to acquire the asset are presented in the consolidated statement of cash flows within investing activities as they relate to the purchase of property plant and equipment.

Provisions (extract)

Leased aircraft maintenance

easyJet incurs liabilities for maintenance and restoration costs in respect of leased aircraft during the term of the lease. These arise from legal and constructive contractual obligations relating to the condition of the aircraft when it is returned to the lessor or when heavy maintenance events are expected to occur during the period of the lease. Contractual maintenance obligations arising from the ongoing use of the aircraft are provided for over the term of the lease based on the estimated future costs of the maintenance events, or forecast penalty charges, discounted to present value. The provision is built as the aircraft are flown, and recognised against the right of use asset, where it is immediately fully depreciated as the flying hours that determine the provision have taken place. The restoration cost obligation is described in the lease section.

1B. ACCOUNTING JUDGEMENTS AND ESTIMATES (extract)

1B.(II) CRITICAL ACCOUNTING ESTIMATES (extract)

Aircraft maintenance provisions – £939 million (2024: £894 million) (note 19)

easyJet incurs liabilities for maintenance costs arising during the lease term of leased aircraft. These costs arise from legal contractual obligations relating to the condition of the aircraft when it is returned to the lessor. To discharge these obligations, it is usual for easyJet to carry out at least one heavy maintenance check on each of the engines and the airframe of the aircraft during the lease term. A material provision representing the estimated cost of this obligation is built up over the course of the lease. The estimates and assumptions used in the calculation of the provision are reviewed at least annually, and when information becomes available that is capable of causing a material change to an estimate, such as the renegotiation of end of lease return conditions, increased or decreased aircraft utilisation, or changes in the cost of heavy maintenance services and the expected uplift in future prices.

A significant portion of the future maintenance costs and cost increases are under contract and provide certainty to the provision. Where cost increases are not under contract, an estimation of the likely future increases are made in the calculation of the provision. Given the significant value of the provision, the provision is sensitive to changes in the future increase of uncontracted costs including the impact of inflationary factors. Additionally, with many maintenance costs incurred in US dollars, the provision remains sensitive to changes in the GBP/USD exchange rate. The rates used to discount the provision to arrive at a present value are based on observable market rates as an estimate of the relevant risk-free rate.

The provision can also be materially influenced by the maintenance status of aircraft when they enter the easyJet fleet. To give flexibility within the fleet plan easyJet may lease ‘mid-life’ aircraft. When mid-life aircraft enter the fleet, a ‘catch-up’ maintenance provision is created to reflect the maintenance obligation for the flying cycles undertaken before the aircraft entered the easyJet fleet. The trigger for the recognition of this addition to the provision is the signing of the lease contract. It is of note that where contractually agreed a mid-life delivery asset is also created when the mid-life leased aircraft enter the fleet, creating a separate related asset on the statement of financial position. A sensitivity analysis is included in note 19.

1B.(III) OTHER AREAS OF JUDGEMENT AND ACCOUNTING ESTIMATES (extract)

Owned aircraft carrying values – £4,685 million (2024: £4,192 million) (note 11)

The key estimates used in arriving at aircraft carrying values are the UELs and residual values of the owned aircraft.

Aircraft are depreciated over their UEL to their residual values in line with the property, plant and equipment accounting policy. The UEL is based on easyJet’s long-term fleet plan and intended utilisation of the current fleet, which include long-term assumptions of market conditions and customer demands, which by their nature are inherently uncertain.

Residual value estimates for aircraft are reviewed annually based on independent aircraft valuations. The valuations are based on an assessment of the current state of the global marketplace for specific aircraft assets. Residual values have continued to increase, with ongoing delivery delays from aircraft original equipment manufacturers, together with the recovery in demand for air travel post the covid pandemic, resulting in strong demand for the previous generation narrowbody aircraft, including the A320ceo. Changes to residual value estimates are applied prospectively, and the review performed on 30 September 2025 resulted in a c.£500 million increase to the residual value of assets that continue to be depreciated. This will result in a c.£60 million reduction in the depreciation charge for the year ended 30 September 2026, which will reduce in subsequent years as the Group disposes its older aircraft. Should the marketplace for an asset class deteriorate unpredictably, there could be a risk that the recoverable amount for some aircraft assets would fall below their current carrying value or that residual values are subject to downward adjustment.

Owned and leased aircraft asset recoverable amounts are included in the Airline CGU and are therefore subject to review for impairment annually or when there is an indication of impairment within the Airline CGU. Further details of the impairment testing applied are included in note 10.

2. NET FINANCE CHARGES/(INCOME)

1) See note 26 for details.

2) Included within net exchange loss/(gain) on monetary assets and liabilities is a £4 million loss (2024: £80 million loss) relating to the fair value loss on US dollar foreign exchange derivatives designated as fair value through profit or loss.

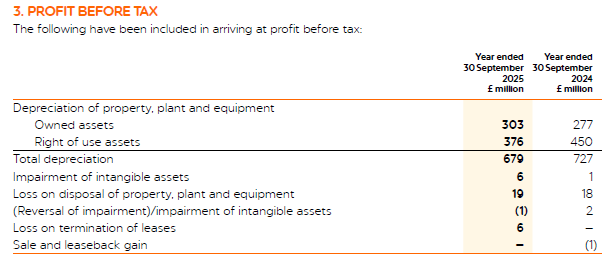

3. PROFIT BEFORE TAX (extract)

The following have been included in arriving at profit before tax:

5. NON-HEADLINE ITEMS (extract)

Sale and leaseback gain

No sale and leaseback transactions were entered into in the current reporting year. In the prior year, easyJet completed the sale and leaseback of 11 A319 aircraft resulting in a £1 million profit on disposal.

18. LEASES (extract)

easyJet holds aircraft under leasing arrangements that are recognised as right of use assets and lease liabilities, with remaining lease terms ranging up to ten years. easyJet is contractually obliged to carry out maintenance on these aircraft, and the cost of this is provided based on the number of flying hours, days and cycles operated and the estimated cost of the maintenance events. Further details are given in note 1.

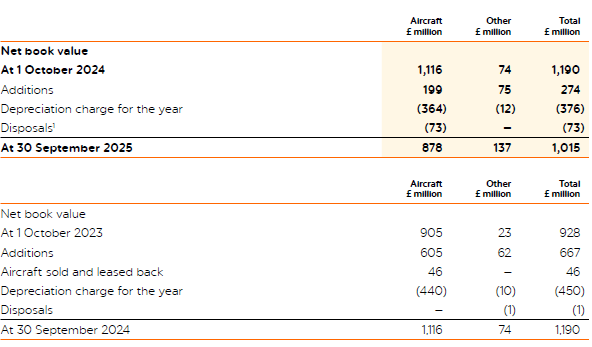

Right of use assets

Information in respect of right of use assets, including the carrying amount, additions and depreciation, is set out below. The right of use assets have been re-presented from property, plant and equipment in note 11. Refer to note 1a for further detail.

1) Right of use asset disposals includes £73 million (2024: £nil) relating to the purchase of eight aircraft that were previously leased, with a corresponding £237 million (2024: £nil) of additions to aircraft owned assets in note 11.

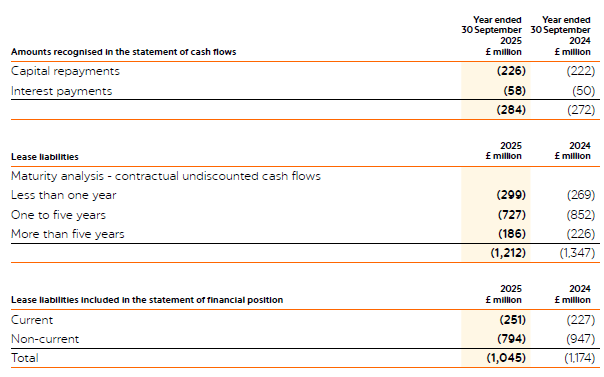

Lease liabilities

Information in respect of the carrying value and interest arising on lease liabilities is set out in note 25 and note 2 respectively. A maturity analysis of lease liabilities is set out below.

easyJet also enters into short-term leases and low-value leases which are not recognised as right of use assets and lease liabilities. The expense recognised in the year in relation to these leases is disclosed below.

19. PROVISIONS FOR LIABILITIES AND CHARGES

The maintenance provisions provide for maintenance costs arising from legal and constructive obligations relating to the condition of the aircraft when returned to the lessor. As a result of the early exit of eight aircraft leases, with the aircraft subsequently being purchased, £61 million (2024: £nil) of the maintenance provision has been released. The early exit of the leases and subsequent purchase of the aircraft resulted in a £54 million (2024: £nil) credit to the income statement. Restructuring and other provisions include amounts in respect of potential liabilities for employee-related matters and litigation which arose in the normal course of business.

The split of the current/non-current maintenance provision is based on the expected maintenance event timings. If actual aircraft usage varies from expectation the timing of the utilisation of the maintenance provision could result in a material change in the classification between current and non-current. Maintenance provisions are expected to be utilised within seven years.

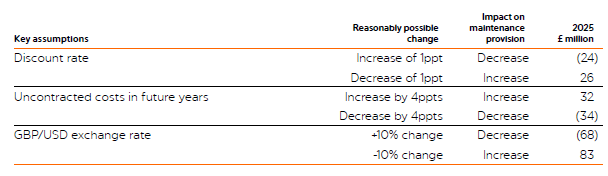

As detailed in note 1B.(II), the aircraft maintenance provision is sensitive to changes in uncontracted costs including the impact of inflationary factors in future years, discount rates and the GBP/USD exchange rate. The following table provides an estimate of the impact on the aircraft maintenance provision of reasonably possible changes to these assumptions.

Within other provisions are provisions for litigation matters. The split of these provisions between current and non-current is based on the dates of expected court judgements. Provisions for restructuring could be fully utilised within one year from 30 September 2025 and therefore are classified as current.