BP p.l.c. – Annual report – 31 December 2025

Industry: oil and gas

1. Material accounting policy information, significant judgements, estimates and assumptions (extract)

Impairment of property, plant and equipment, intangible assets, goodwill, and equity-accounted entities

The group assesses assets or groups of assets, called cash-generating units (CGUs), for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset or CGU may not be recoverable; for example, changes in the group’s business plans, plans to dispose rather than retain assets, changes in the group’s assumptions about discount rates, commodity prices, low plant utilization, evidence of physical damage or, for oil and gas assets, significant downward revisions of estimated reserves or increases in estimated future development expenditure or decommissioning costs. If any such indication of impairment exists, the group makes an estimate of the asset’s or CGU’s recoverable amount. Individual assets are grouped into CGUs for impairment assessment purposes at the lowest level at which there are identifiable cash inflows that are largely independent of the cash inflows of other groups of assets. A CGU’s recoverable amount is the higher of its fair value less costs of disposal and its value in use. If it is probable that the value of the CGU will be primarily recovered through a disposal transaction, the expected disposal proceeds are considered in determining the recoverable amount. Where the carrying amount of a CGU exceeds its recoverable amount, the CGU is considered impaired and is written down to its recoverable amount.

The business segment plans, which are approved on an annual basis by senior management, are the primary source of information for the determination of value in use. They contain forecasts for oil and natural gas production, power generation, refinery throughputs, sales volumes for various types of refined products (e.g. gasoline and lubricants), revenues, costs and capital expenditure. Carbon taxes and costs of emissions allowances are included in estimates of future cash flows, where applicable, based on the regulatory environment in each jurisdiction in which the group operates. As an initial step in the preparation of these plans, various assumptions regarding market conditions, such as oil prices, natural gas prices, power prices, refining margins, refined product margins and cost inflation rates are set by senior management. These assumptions take account of existing prices, global supply-demand equilibrium for oil and natural gas, other macroeconomic factors and historical trends and variability. In assessing value in use, the estimated future cash flows are adjusted for the risks specific to the asset group to the extent that they are not already reflected in the discount rate and are discounted to their present value typically using a pre-tax discount rate that reflects current market assessments of the time value of money.

Fair value less costs of disposal is the price that would be received to sell the asset in an orderly transaction between market participants and does not reflect the effects of factors that may be specific to the group and not applicable to entities in general. Fair value may be determined by reference to agreed or expected sales proceeds, recent market transactions for similar assets or using discounted cash flow analyses. Where discounted cash flow analyses are used to calculate fair value less costs of disposal, estimates are made about the assumptions market participants would use when pricing the asset, CGU or group of CGUs containing goodwill and the test is performed on a post-tax basis.

An assessment is made at each reporting date as to whether there is any indication that previously recognized impairment losses may no longer exist or may have decreased. If such an indication exists, the recoverable amount is estimated. A previously recognized impairment loss is reversed only if there has been a change in the estimates used to determine the asset’s or CGU’s recoverable amount since the last impairment loss was recognized. If that is the case, the carrying amount of the asset or CGU is increased to the lower of its recoverable amount and the carrying amount that would have been determined, net of depreciation, had no impairment loss been recognized for the asset or CGU in prior years. Impairment reversals are recognized in profit or loss. After a reversal, the depreciation charge is adjusted in future periods to allocate the asset’s or CGU’s revised carrying amount, less any residual value, on a systematic basis over its remaining useful life.

Goodwill is reviewed for impairment annually or more frequently if events or changes in circumstances indicate the recoverable amount of the group of CGUs to which the goodwill relates should be assessed. In assessing whether goodwill has been impaired, the carrying amount of the group of CGUs to which goodwill has been allocated is compared with its recoverable amount. Where the recoverable amount of the group of CGUs is less than the carrying amount (including goodwill), an impairment loss is recognized. An impairment loss recognized for goodwill is not reversed in a subsequent period.

The group assesses investments in equity-accounted entities for impairment whenever there is objective evidence that the investment is impaired, after recognizing its share of any losses of the equity-accounted entity itself. If any such objective evidence of impairment exists, the carrying amount of the investment is compared with its recoverable amount, being the higher of its fair value less costs of disposal and value in use. If the carrying amount exceeds the recoverable amount, the investment is written down to its recoverable amount.

Significant judgements and estimates: recoverability of asset carrying values

Determination as to whether, and by how much, an asset, CGU, or group of CGUs containing goodwill is impaired involves management estimates on highly uncertain matters such as the effects of inflation and deflation on operating expenses, discount rates, capital expenditure, carbon pricing (where applicable), production profiles, reserves and resources, and future commodity prices, including the outlook for global or regional market supply-and-demand conditions for crude oil, natural gas, power and refined products. Judgement is required when determining the appropriate grouping of assets into a CGU or the appropriate grouping of CGUs for impairment testing purposes. For example, individual oil and gas properties may form separate CGUs whilst certain oil and gas properties with shared infrastructure may be grouped together to form a single CGU. Alternative groupings of assets or CGUs may result in a different outcome from impairment testing. See Note 14 for details on how these groupings have been determined in relation to the impairment testing of goodwill.

As described above, the recoverable amount of an asset is the higher of its value in use and its fair value less costs of disposal. Fair value less costs of disposal may be determined based on expected sales proceeds or similar recent market transaction data.

Details of impairment charges and reversals recognized in the income statement are provided in Note 4 and details on the carrying amounts of assets are shown in Note 12, Note 14 and Note 15.

The estimates for assumptions made in impairment tests in 2025 relating to discount rates and oil and gas properties are discussed below. Changes in the economic environment including as a result of the energy transition or other facts and circumstances may necessitate revisions to these assumptions and could result in a material change to the carrying values of the group’s assets within the next financial year.

Discount rates

For discounted cash flow calculations, future cash flows are adjusted for risks specific to the CGU. Value-in-use calculations are typically discounted using a pre-tax discount rate based upon the cost of funding the group derived from an established model, adjusted to a pre-tax basis and incorporating a market participant capital structure and country risk premiums. Fair value less costs of disposal discounted cash flow calculations use a post-tax discount rate.

The discount rates applied in impairment tests are reassessed each year and, in 2025, the post-tax discount rate was 8% (2024 8%) other than for renewable power assets. Where the CGU is located in a country that was judged to be higher risk, an additional premium of 1% to 3% was reflected in the post-tax discount rate (2024 1% to 3%). The judgement of classifying a country as higher risk and the applicable premium takes into account various economic and geopolitical factors. The pre-tax discount rate, other than for renewable power assets, typically ranged from 9% to 18% (2024 9% to 20%) depending on the risk premium and applicable tax rate in the geographic location of the CGU. For renewable power assets tested on a value-in-use basis, primarily the CGUs for which goodwill was allocated following the Lightsource bp acquisition, a WACC-based post-tax discount rate of 7% was used. For renewable power assets tested on a fair-value basis, primarily offshore wind assets (including those in equity accounted entities), a post-tax cost of equity-based discount rate range of 8.75% to 9.5% (2024 8.75% to 9.5%) was used.

Oil and natural gas properties

For oil and natural gas properties in the oil production & operations and gas & low carbon energy segments, expected future cash flows are estimated using management’s best estimate of future oil and natural gas prices, production and reserves and certain resources volumes. Forecast cash flows include the impact of all approved emission reduction projects. The estimated future level of production in all impairment tests is based on assumptions about future commodity prices, production and development costs, field decline rates, current fiscal regimes and other factors.

In 2025, the group identified oil and gas properties in these segments with carrying amounts totalling $20,341 million (2024 $17,853 million) where the headroom, based on the most recent impairment test performed in the year on those assets, was less than or equal to 20% of the carrying value. A change in the discount rate, reserves, resources or the oil and gas price assumptions in the next financial year may result in a recoverable amount of one or more of these assets above or below the current carrying amount and therefore there is a risk of impairment reversals or charges in that period. Management considers that reasonably possible changes in the discount rate or forecast revenue, arising from a change in oil and natural gas prices and/or production could result in a material change in their carrying amounts within the next financial year, see Sensitivity analyses, below.

The recoverability of intangible exploration and appraisal expenditure is covered under Oil and natural gas exploration, appraisal and development expenditure above.

Oil and natural gas prices

The price assumptions used for value-in-use impairment testing are based on those used for investment appraisal. bp’s carbon emissions cost assumptions and their interrelationship with oil and gas prices are described in ‘Judgements and estimates made in assessing the impact of climate change and the transition to a lower carbon economy’ on page 160. The investment appraisal price assumptions were recommended by the senior vice president economic & energy insights after considering a range of external price sets, and supply and demand profiles associated with various energy transition scenarios. They were reviewed and approved by management. As a result of the current uncertainty over the pace of transition to lower-carbon supply and demand and the social, political and environmental actions that will be taken to meet the goals of the Paris climate change agreement, the scenarios considered include those where those goals are met as well as those where they are not met.

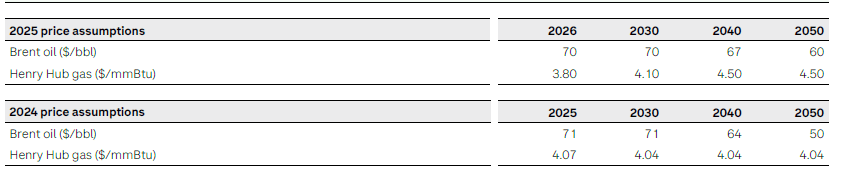

During the year, bp’s price assumptions applied in value-in-use impairment testing were revised. The revised price assumptions have been rebased in real 2024 terms. Brent oil prices in real 2024 terms were reduced to $70 per barrel. Medium to long term prices steadily decline to a higher price of $60 per barrel by 2050 continuing to reflect the assumption that the energy system decarbonizes but at a slower rate. The price assumptions for the Henry Hub price have been reduced in the near term, reflecting higher supply in the market. Prices then steadily increase in the medium term, as supply and demand remain steady at $4.50 per mmBtu up to 2050. These price assumptions are derived from the central case investment appraisal assumptions. A summary of the group’s revised price assumptions for Brent oil and Henry Hub gas, applied in 2025 and 2024, in real 2024 terms, is provided below. The assumptions represent management’s best estimate of future prices at the balance sheet date, which sit within the range of external scenarios considered as appropriate for the purpose. They are considered by bp to be in line with a range of transition paths, as collated into the Transition Scenario Catalogue we use in our TCFD assessment, that are considered by source data providers (such as IEA, UN PRI IPR and NGFS) to be consistent with holding the increase in the global average temperature to well below 2°C above preindustrial levels and pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels. However, they do not correspond to any specific Paris-consistent scenario. An inflation rate of 2.0% – 3.0% (2024 2.0%-2.5%) is applied to determine the price assumptions in nominal terms.

The majority of bp’s reserves and resources that support the carrying value of the group’s existing oil and gas properties are expected to be produced over the next 12 years.

The recoverability of deferred tax assets is also affected by the group’s oil and natural gas price assumptions as these could impact the estimate of future taxable profits. See Note 9 for further information.

Global oil production increased by 3mmb/d (3%) in 2025, with non-OPEC+ countries contributing nearly 60% of the growth. Global oil demand grew by only 0.8% in 2025, almost entirely accounted for by non-OECD countries, following sharp fall in oil demand from Brazil, India and China. The global supply/demand imbalance of around 2.2mmb/d weighed on prices, with Dated Brent down by nearly $12 per barrel. While geopolitical risk (e.g., tariffs, sanctions) may support prices in the short-term, bp’s long-term assumption for oil prices is lower than the 2025 average as oil demand is likely to fall such that the price levels needed to encourage sufficient investment to meet global oil demand will also be lower.

The US Henry Hub (HH) spot price averaged $3.5 per mmBtu in 2025, up from $2.2 per mmBtu in 2024 and the highest level since 2022, driven by increased LNG export demand and a colder-than-normal start to the year. Higher gas prices supported a recovery in drilling activity in non-associated (dry) shale plays which, combined with well productivity gains, increasing gas-to-oil ratios in the Permian, and increased pipeline connectivity, meant that US dry gas production grew by 4% year on year and reached record high levels. The level of US gas prices in 2025 was below bp’s long term price assumption based on the judgment of the price level required to incentivize new production.

Oil and natural gas reserves

In addition to oil and natural gas prices, significant technical and commercial assessments are required to determine the group’s estimated oil and natural gas reserves. Reserves estimates are regularly reviewed and updated. Factors such as the availability of geological and engineering data, reservoir performance data, acquisition and divestment activity and drilling of new wells all impact on the determination of the group’s estimates of its oil and natural gas reserves. bp bases its reserves estimates on the requirement of reasonable certainty with rigorous technical and commercial assessments based on conventional industry practice and regulatory requirements.

Reserves assumptions for value-in-use tests reflect the reserves and resources that management currently intend to develop. The recoverable amount of oil and gas properties is determined using a combination of inputs including reserves, resources and production volumes. Risk factors may be applied to reserves and resources which do not meet the criteria to be treated as proved or probable.

Sensitivity analyses

Management considers discount rates, oil and natural gas prices and production to be the key sources of estimation uncertainty in determining the recoverable amount of upstream oil and gas assets. The sensitivity analyses below, in addition to covering the key sources of estimation uncertainty, also indicate how the energy transition, potential future carbon emissions costs for operational GHG emissions and/or reduced demand for oil and gas may further impact forecast revenue cash inflows to a greater extent than currently anticipated in the group’s value-in-use estimates for oil and gas CGUs, if carbon emissions costs were to be implemented as a deduction against revenue cash flows. The analyses therefore represent a net revenue sensitivity.

A change in net revenue from upstream oil and gas properties can arise either due to changes in oil and natural gas prices, carbon emissions costs/carbon prices, changes in oil and natural gas production, or a combination of these.

Management tested the impact of changes in net revenue cash flows in value-in-use impairment testing under the following sensitivity analyses: an increase in net revenues of 8% in all years up to 2040, and 25% in all remaining years to 2050; and a decrease in net revenues of 20% in all years up to 2030, 35% in all subsequent years to 2040 and 50% in all remaining years to 2050.

Net revenue reductions of this magnitude in isolation could indicatively lead to a reduction in the carrying amount of bp’s currently held upstream oil and gas properties in the range of $20-21 billion which is approximately 34% of the associated net book value of property, plant and equipment as at 31 December 2025. If this net revenue reduction was due to reductions in prices in isolation, it reflects an indicative decrease in the carrying amount of using price assumptions for Brent oil trending broadly towards the bottom of the range of prices associated with the ‘family’ of scenarios in our Transition Scenario Catalogue considered, by source data providers, to be consistent with limiting global average temperature to 1.5°C above pre-industrial levels. This Catalogue of scenarios is also used in bp’s TCFD resilience scenario analysis.

Net revenue increases of this magnitude in isolation could indicatively lead to an increase in the carrying amount of bp’s currently held upstream oil and gas properties in the range of $1-2 billion which is approximately 2-3% of the associated net book value of property, plant and equipment as at 31 December 2025. This potential increase in the carrying amount would arise due to reversals of previously recognized impairments and represents approximately 15% of the total impairment reversal capacity available at 31 December 2025. If this net revenue increase was due to increases in prices in isolation, it reflects an indicative increase in the carrying amount of using price assumptions for Brent oil trending broadly aligned with the top end until the mid-2040s, and then towards the mean average at 2050, of the range of prices associated with the Transition Scenario Catalogue of scenarios (which included the IEA’s World Energy Outlook Net Zero Emissions by 2050 (NZE) scenario) considered by IEA to be consistent with limiting global average temperature to 1.5°C above pre-industrial levels.

These sensitivity analyses do not, however, represent management’s best estimate of any impairment charges or reversals that might be recognized as they do not fully incorporate consequential changes that may arise, such as changes in costs and business plans and phasing of development. For example, costs across the industry are more likely to decrease as oil and natural gas prices fall. The analyses also assume the impact of increases in carbon price on operational GHG emissions are fully absorbed as a decrease in net revenue (and vice versa) rather than reflecting how carbon prices or other carbon emissions costs may ultimately be incorporated by the market. The above sensitivity analyses therefore do not reflect a linear relationship between net revenue and value that can be extrapolated. The interdependency of these inputs and factors plus the diverse characteristics of the group’s upstream oil and gas properties limits the practicability of estimating the probability or extent to which the overall recoverable amount is impacted by changes to the price assumptions or production volumes.

Management also tested the impact of a one percentage point change in the discount rate used for value-in-use impairment testing of upstream oil and gas properties. This level of change reflects past experience of a reasonable change in rate that could arise within the next financial year. If the discount rate was one percentage point higher across all tests performed, the net impairment loss recognized in 2025 would have been approximately $0.2 billion higher. If the discount rate was one percentage point lower, the net impairment loss recognized would have been approximately $0.5 billion lower.

Management considers discount rate, renewable natural gas prices, and the level of capital expenditure and its consequential impact on production volumes to be the key sources of estimation uncertainty in determining the recoverable amount of the group’s renewable natural gas assets owned by Archaea Energy.

A change in revenue from renewable natural gas assets could arise either due to changes in renewable natural gas prices, changes in renewable natural gas production, principally as a result of changes in capital invested, or a combination of both.

Management tested the impact of changes in net revenue cash flows on its value-in-use impairment testing. It is estimated that a reduction in revenue across all Archaea Energy assets of 10% would have resulted in an additional impairment charge of $0.5 billion. It is estimated that an increase in revenue of 10% would have resulted in a reduction to the impairment charge of $0.8 billion.

These sensitivity analyses do not, however, represent management’s best estimate of any impairment charges or reversals that might be recognized as they do not fully incorporate consequential changes that may arise, such as changes in capital and operating costs, business plans and phasing of development. The above sensitivity analyses therefore do not reflect a linear relationship between net revenue and value that can be extrapolated. The interdependency of these inputs and factors limits the practicability of estimating the probability or extent to which the overall recoverable amount is impacted by changes to the price assumptions or production volumes.

It is estimated that an increase to the discount rate of 1% would have resulted in an additional impairment charge to Archaea Energy assets of $0.3 billion. It is estimated that a decrease in the discount rate of 1% would have resulted in a reduction to the impairment charge of $0.4 billion.

Management considers discount rates and refining margins to be the key sources of estimation uncertainty in determining the recoverable amount of refinery assets. The sensitivity analysis below, in addition to covering the key sources of estimation uncertainty, also indicates how the energy transition and/or reduced demand for refined products may further impact forecast cash inflows to a greater extent than currently anticipated in the group’s value-in-use estimates for refinery CGUs.

Management tested the impact of a $1 per barrel decrease in each refinery’s future margin assumption in all years of the value-in-use estimate. A reduction of this magnitude in isolation could indicatively lead to a reduction in the carrying amount of bp’s currently held refining property, plant and equipment in the range of $1-2 billion.

This sensitivity analysis does not, however, represent management’s best estimate of any impairment charges that might be recognized as it does not fully incorporate consequential changes that may arise, such as changes in costs and business plans and crude or product slates. The above sensitivity analysis therefore does not reflect a linear relationship between margins and value that can be extrapolated. The interdependency of these inputs and factors plus the varying configurations of the group’s refineries limits the practicability of estimating the probability or extent to which the overall recoverable amount is impacted by changes to the margin assumptions.

Management also tested the impact of a one percentage point change in the discount rate used for value-in-use impairment testing of refinery assets. This level of change reflects past experience of a reasonable change in rate that could arise within the next financial year. If the discount rate was one percentage point higher across all tests performed, the net impairment loss recognized in 2025 would have been approximately $0.5 billion higher. If the discount rate was one percentage point lower there would have been no impact on the net impairment loss recognized in 2025.

Goodwill

Irrespective of whether there is any indication of impairment, bp is required to test annually for impairment of goodwill acquired in business combinations. The group carries goodwill of $10.3 billion on its balance sheet (2024 $14.9 billion), principally relating to the Atlantic Richfield, Devon Energy, Reliance transactions and its transition businesses. Of this, $7.1 billion relates to goodwill in the oil production & operations segment and to hydrocarbon CGUs within the gas & low carbon energy segment (2024 $7.2 billion), for which oil and gas price and production assumptions are key sources of estimation uncertainty. A further $0.9 billion relates to the transition businesses in the gas & low carbon energy segment (2024 $2.9 billion), for which project development revenues and margins, terminal value growth rate and discount rate are key sources of estimation uncertainty. Sensitivities and additional information relating to impairment testing of goodwill in these segments are provided in Note 14.

Judgements and estimates made in assessing the impact of climate change and the transition to a lower carbon economy

Climate change and the transition to a lower carbon economy were considered in preparing the consolidated financial statements. These may have significant impacts on the currently reported amounts of the group’s assets and liabilities discussed below and on similar assets and liabilities that may be recognized in the future. The group’s assumptions for investment appraisal form part of an investment decision-making framework for currently unsanctioned future capital expenditure on property, plant and equipment, and intangibles including exploration and appraisal assets, that is designed to support the effective and resilient implementation of bp’s strategy. The price assumptions used for investment appraisal include oil and gas price assumptions, which are producer prices and are therefore net of any future carbon prices that the purchaser may be required to pay, and an assumption of a single carbon emissions cost imposed on the producer in respect of operational greenhouse gas (GHG) emissions (carbon dioxide and methane) in order to incentivize engineering solutions to mitigate GHG emissions on projects. The group’s oil and gas price assumptions for value-in-use impairment testing are aligned with those investment appraisal assumptions. The assumptions for future carbon emissions costs in value-in-use impairment testing differ from the investment appraisal assumptions and are described below.

Management has also not identified any off-balance sheet commodity purchase obligations to be onerous contracts as result of the transition to a lower carbon economy at 31 December 2025.

Impairment of property, plant and equipment and goodwill

The energy transition is likely to impact the future prices of commodities such as oil and natural gas which in turn may affect the recoverable amount of property, plant and equipment and goodwill in the oil and gas industry. Management’s best estimate of oil and natural gas price assumptions for value-in-use impairment testing were revised during 2025. The revised price assumptions have been rebased in real 2024 terms. Brent oil prices in real 2024 terms were reduced in the short-term reflecting greater crude supply. Medium to long term prices steadily decline to a higher price of $60 per barrel in 2050 continuing to reflect the assumption that the energy system decarbonises but at a slower rate. The price assumptions for Henry Hub gas price have been reduced in the short term, reflecting higher supply in the market. Prices then steadily increase in the medium term, as supply and demand rebalance before remaining steady at $4.50 per mmBtu up to 2050. The revised assumptions for Brent oil and Henry Hub gas sit within the range of external scenarios considered by management and are in line with a range of transition paths, as collated into the Transition Scenario Catalogue we use in our TCFD assessment, that are considered by source data providers (such as IEA, UN PRI IPR and NGFS) to be consistent with holding the increase in the global average temperature to well below 2°C above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels.

As noted above, the group’s investment appraisal process includes a carbon emissions price series for the investment economics which is applied to bp’s anticipated share of bp’s forecast of the investment assets’ scope 1 and 2 GHG emissions where they exceed defined thresholds, and is assumed to apply whether or not bp is the asset operator. However, for value-in-use impairment testing on bp’s existing cash generating units (CGUs), consistent with all other relevant cash flows estimated, bp is required to reflect management’s best estimate of any expected applicable carbon emission costs payable by bp, including where bp is not the operator, in the future for each jurisdiction in which the group has interests. This requires management’s best estimate of how future changes to relevant carbon emission cost policies and/or legislation are likely to affect the future cash flows of the group’s applicable CGUs, whether currently enacted or not. Future potential carbon pricing and/or costs of carbon emissions allowances are included in the value-in-use calculations to the extent management has sufficient information to make such an estimate. Currently this results in limited application of carbon price assumptions in value-in-use impairment tests given that carbon pricing legislation in most impacted jurisdictions where the group has interests is not in place and there is not sufficient information available as to the relevant policy makers’ future intentions regarding carbon pricing to support an estimate. A key input into the determination of impairment is the assumption, aligned with bp’s aim to reach net zero greenhouse gas emissions by 2050 or sooner, that the current recognized portfolio of oil and gas properties and refining assets will have an immaterial carrying value by 2050.

Where we consider that the outcome of a value-in-use impairment test could be significantly affected by a carbon price in place in any jurisdiction, this is incorporated into the value-in use impairment testing cash flows. The most significant instances where a carbon price has been incorporated in the 2025 value-in-use impairment tests is for the UK North Sea. The assumptions for UK North Sea were £65/tCO2e in 2026 gradually increasing to £243/tCO2e in 2050.

However, as bp’s forecast future prices are producer prices, the group considers it reasonable to assume that if, in addition to the costs already in place, further scope 1 and 2 emission costs were partially to be borne directly by oil and gas producers including bp in future and the prevalence of such costs were to become widespread, the gross oil and gas prices realized by producers would be correspondingly higher over the long term, resulting in no expected overall materially negative impacts on the group’s net cash flows. See significant judgements and estimates: recoverability of asset carrying values for further information including sensitivity analysis in relation to reasonably possible changes in the price assumptions and carbon costs.

Production assumptions within upstream property, plant and equipment and goodwill value-in-use impairment tests reflect management’s current best estimate of future production of the existing upstream portfolio. See significant judgements and estimates: recoverability of asset carrying values and Note 14 for sensitivity analyses in relation to reasonably possible changes in production for upstream oil and gas properties and goodwill respectively.

For the customers & products segment, though the energy transition may impact demand for certain refined products in the future, management anticipates sufficiently robust demand for the remainder of each refinery’s useful life. Management will continue to review price assumptions as the energy transition progresses and this may result in impairment charges or reversals in the future.

Exploration and appraisal intangible assets

The energy transition may affect the future development or viability of exploration prospects. The recoverability of the group’s exploration and appraisal intangible assets was considered during 2025. No significant write-offs were identified. These assets will continue to be assessed as the energy transition progresses. See significant judgement: exploration and appraisal intangible assets and Note 8 for further information.

Property, plant and equipment – depreciation and expected useful lives

The energy transition may curtail the expected useful lives of oil and gas industry assets thereby accelerating depreciation charges. However, a significant majority of bp’s existing upstream oil and natural gas properties are likely to have immaterial carrying values within the next 12 years and, as outlined in bp’s strategy, oil and natural gas production will remain an important part of bp’s business activities over that period. The significant majority of refining assets, recognized on the group’s balance sheet at 31 December 2025 that are subject to depreciation, will be depreciated within the next 11 years; demand for refined products is expected to remain sufficient to support the remaining useful lives of existing assets. Therefore, management does not expect the useful lives of bp’s reported property, plant and equipment to change and do not consider this to be a significant accounting judgement or estimate. Significant capital expenditure is still required for ongoing projects as well as renewal and/or replacement of aged assets and therefore the useful lives of future capital expenditure may be different. See material accounting policy: property, plant and equipment for more information.

Provisions: decommissioning

The energy transition may bring forward the decommissioning of oil and gas industry assets thereby increasing the present value of associated decommissioning provisions. The majority of bp’s existing upstream oil and gas properties are expected to start decommissioning within the next two decades. Currently, the expected timing of decommissioning expenditures for the upstream oil and gas assets in the group’s portfolio has not materially been brought forward. Management does not expect a reasonably possible change of two years in the expected timing of all decommissioning to have a material effect on the upstream decommissioning provisions, assuming cost assumptions remain unchanged.

Decommissioning cost estimates are based on the known regulatory and external environment. These cost estimates may change in the future, including as a result of the transition to a lower carbon economy. For refineries, decommissioning provisions are generally not recognized as the associated obligations have indeterminate settlement dates, typically driven by the cessation of manufacturing. Management does not expect manufacturing to cease at refineries within a determinate period of time, as existing property, plant and equipment is expected to be renewed or replaced. Management will continue to review facts and circumstances, including where cessation of manufacturing decisions have been made, to assess if decommissioning provisions need to be recognized. Decommissioning provisions relating to refineries at 31 December 2025 are not material. See significant judgements and estimates: provisions for further information.

Judgements and estimates made in assessing the impact of the geopolitical and economic environment

In preparing the consolidated financial statements, the following areas involving judgement and estimates were identified as most relevant with regards to the impact of the current geopolitical and economic environment.

Oil and gas price assumptions

Oil and gas price assumptions applied in value-in-use impairment testing have been updated (as noted above) including for inflation and have been rebased in real 2024 terms. See significant judgements and estimates: recoverability of asset carrying values for further information.

Discount rate assumptions

The discount rates used for impairment testing and provisions were reassessed during the year in light of changing economic and geopolitical outlooks. The impact on the nominal discount rate applied to provisions was determined not to be significant and so the rate remained unchanged from 2024. The post-tax impairment discount rate remained consistent with 2024 as did the risk premium applied to the majority of countries classified as higher-risk. See significant judgements and estimates: recoverability of asset carrying values and provisions for further information.

Pensions and other post-employment benefits

Volatility in financial markets impact assumptions used for determining the fair value of plan assets and the present value of defined benefit obligations in the group’s defined benefit pension plans. See significant estimate: pensions and other post-employment benefits and Note 24 for further information.

4. Disposals and impairment (extract 1)

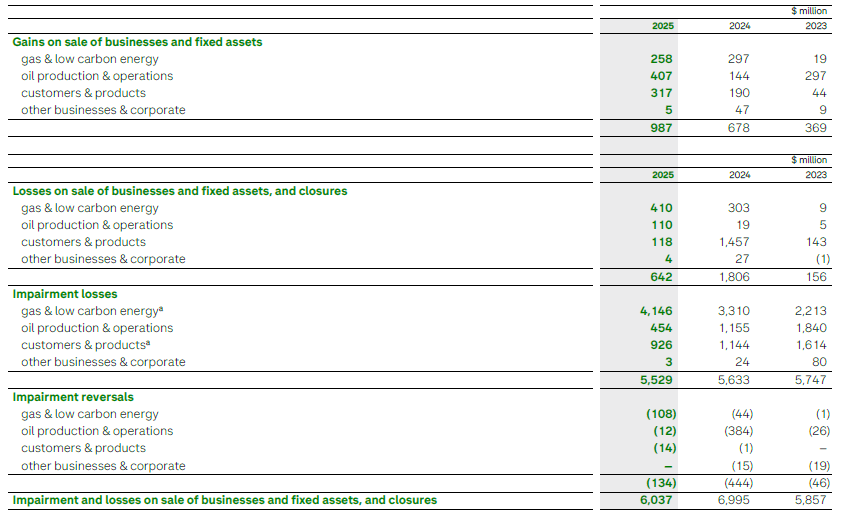

The following amounts were recognized in the income statement in respect of disposals and impairments.

a 2024 balances and related narrative has been restated to reflect the move of our Archaea Energy business from the customers & products segment to the gas & low carbon energy segment.

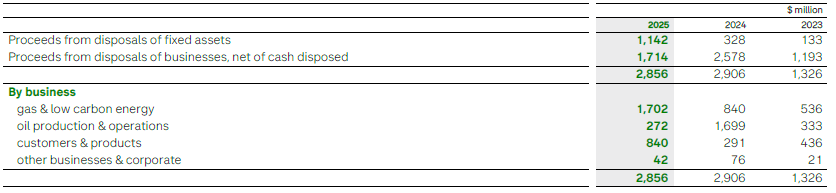

Disposals

Disposal proceeds and principal gains and losses on disposals by segment are described below.

4. Disposals and impairment (extract 2)

Impairments

Impairment losses and impairment reversals in each segment are described below. For information on significant estimates and judgements made in relation to impairments see Impairment of property, plant and equipment, intangibles, goodwill and equity-accounted entities within Note 1. See also Note 12, and Note 15 for further information on impairments by asset category.

gas & low carbon energy

The 2025 impairment loss of $4,146 million includes $3,537 million relating to the transition businesses, principally Archaea Energy and Lightsource bp, and $609 million relating to the upstream gas business, principally Mauritania and Senegal. The impairments arose as a result of revised assumptions including capital and operating expenditure and the impact of market conditions on project development. The recoverable amount of all CGUs for which impairment charges were recognized in 2025 is $8,805 million.

The 2024 impairment loss of $3,310 million includes amounts in Mauritania & Senegal ($1,495 million), which principally arose as a result of increased forecast future expenditure, and a number of other individually immaterial impairments across the segment principally as a result of portfolio management. The recoverable amounts of these cash generating units (CGUs) were based on value in use or fair value less costs of disposal calculations, as appropriate. The recoverable amount of all CGUs for which impairment charges were recognized in 2024 is $5,025 million.

The 2023 impairment loss of $2,213 million primarily relates to losses incurred in respect of certain assets in Mauritania & Senegal ($1,434 million) and principally arose as a result of increased forecast future expenditure. A further $565 million relates to producing assets in Trinidad and arose as a result of changes to the group’s oil and gas price and discount rate assumptions and activity phasing. The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2023 in total, based on their value in use, is $4,811 million.

oil production & operations

Impairment losses and reversals in all years relate primarily to producing assets.

The 2025 impairment loss of $454 million primarily arose as a result of changes to reserves and decommissioning provisions mainly driven by foreign exchange in the North Sea ($397 million). The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2025 in total, based on their value in use, is $2,058 million.

The 2024 impairment loss of $1,155 million primarily arose as a result of changes to reserves and tax assumptions in the North Sea ($1,035 million). The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2024 in total, based on their value in use, is $8,705 million.

The 2023 impairment loss of $1,840 million primarily arose as a result of changes to the group’s oil and gas price and discount rate assumptions, activity phasing and disposal decisions in relation to certain assets in North Sea ($852 million) and in bpx energy ($802 million). The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2023 in total, based on their value in use, is $14,072 million.

customers & products

The 2025 impairment loss of $926 million primarily relates to strategy implementation in the products business. The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2025 in total, based on their value in use, is $49 million.

The 2024 impairment loss of $1,144 million primarily arises from the ongoing review of the Gelsenkirchen refinery in Germany ($807 million) and a number of other individually immaterial impairments across the segment, principally as a result of changes to economic assumptions. The recoverable amount of the CGUs were based on value-in-use calculations. The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2024 in total, based on their value-in-use, is $57 million.

The 2023 impairment loss of $1,614 million primarily relates to strategy implementation and changes to economic assumptions in the products business including an impairment of the Gelsenkirchen refinery in Germany ($1,336 million). The recoverable amounts of the CGUs were based on value-in-use calculations. The recoverable amount of all CGUs for which impairment charges or reversals were recognized in 2023 in total, based on their value in use, is $327 million.

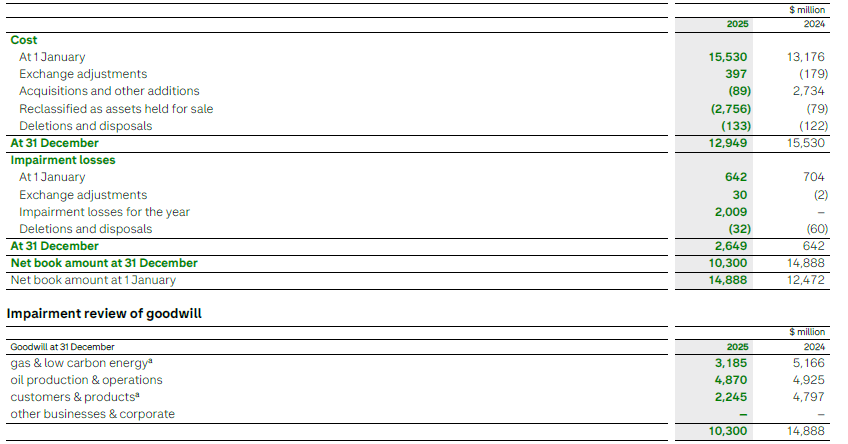

14. Goodwill and impairment review of goodwill

a 2024 restated to reflect the move of our Archaea Energy business from the customers & products segment to the gas & low carbon energy segment.

Goodwill acquired through business combinations has been allocated to groups of cash-generating units (CGUs) that are expected to benefit from the synergies of the acquisition. For oil production & operations goodwill is allocated to CGUs in aggregate at the segment level, for gas & low carbon energy, goodwill is allocated to the hydrocarbon CGUs (‘upstream gas businesses’) within the segment and to Lightsource bp (LSbp) and Archaea Energy (‘transition businesses’). For customers and products, goodwill has been allocated to Castrol, US Fuels, European Fuels and Other.

For information on significant estimates and judgements made in relation to impairments see Impairment of property, plant and equipment, intangible assets and goodwill in Note 1.

gas & low carbon energy and oil production & operations

The table above shows the carrying amount of goodwill for the segments at the period end and the excess of the recoverable amount over the carrying amount (headroom) at the date of the most recent test. The recoverable amounts for the upstream gas businesses and transition businesses are based on value-in-use calculations. The increase in headroom for the goodwill impairment tests for the upstream gas businesses is due to the passage of time and price impacts. For oil production & operations management have rolled-forward the most recent detailed calculation as the criteria set out in IAS 36 for doing so were met.

During 2025 impairment charges of $2,009 million were recognized against the transition businesses goodwill balance. The impairment charges arose as a result of changes in assumptions including future capital and operating expenditure and project development. No impairment of the goodwill in the upstream gas businesses was recognized in 2025 or 2024. No impairment of the goodwill in oil production & operations was recognized during 2025 or 2024.

Upstream gas businesses and oil production & operations

The value in use for relevant CGUs in both the upstream gas businesses and oil production & operations is based on the cash flows expected to be generated by the projected production profiles up to the expected dates of cessation of production of each field, based on appropriately risked estimates of reserves and resources. Midstream and supply and trading activities and equity-accounted entities are generally not included in the impairment reviews of goodwill, as they do not represent part of the grouping of CGUs to which the goodwill balances relate and which are used to monitor the goodwill balances for internal management purposes. Where such activities form part of wider CGUs to which goodwill relates they are reflected in the test. As the production profile and related cash flows can be estimated from bp’s past experience, management believes that the cash flows generated over the estimated life of field is the appropriate basis upon which to assess goodwill and individual assets for impairment in both the upstream gas businesses and oil & production operations. The estimated date of cessation of production depends on the interaction of a number of variables, such as the recoverable quantities of hydrocarbons, the production profile of the hydrocarbons, the cost of the development of the infrastructure necessary to recover the hydrocarbons, production costs, the contractual duration of the production concession and the selling price of the hydrocarbons produced. As each field has specific reservoir characteristics and economic circumstances, the cash flows of each field are computed using appropriate individual economic models and key assumptions agreed by bp management.

Estimated production volumes and cash flows up to the date of cessation of production on a field-by-field basis, including operating and capital expenditure, are derived from the business segment plans. The production profiles used are consistent with the reserve and resource volumes approved as part of bp’s centrally controlled process for the estimation of proved and probable reserves and total resources.

The average production for the purposes of goodwill impairment testing in the upstream gas businesses over the next 15 years is 146 mmboe per year (2024 154 mmboe per year) and in the oil production and operations segment is 400 mmboe per year (2024 400 mmboe per year). Production assumptions used for the goodwill impairment tests in both the upstream gas businesses and oil production & operations reflect management’s best estimate of future production of the existing portfolio at the time of the calculation.

The weighted-average pre-tax discount rate used in the review for the oil production & operations segment is 17%, and 11% for the gas businesses (2024 17% for the oil production & operations segment and 11% for the gas businesses).

The most recent reviews for impairment for the oil production & operations and the upstream gas businesses were carried out in the fourth quarter. The key assumptions used in the value-in-use calculations are oil and natural gas prices, production volumes and the discount rate. The value-in-use calculations have been prepared for the purposes of determining whether the goodwill balances were impaired. For the upstream gas businesses , estimated future cash flows were prepared on the basis of certain assumptions prevailing at the time of the tests. For the oil production & operations segment, as permitted by IAS 36, the detailed calculations for recoverable amounts performed in 2024 were used as a basis for the 2025 impairment tests. The recoverable amounts, key assumptions and sensitivity calculations for 2025 are prepared using the remaining future cashflows from the 2024 detailed calculations. The headrooms for 2025 do not represent the headrooms that would result if a test was run based on discounted future cashflows estimated using 2025 data and assumptions. The actual outcomes may differ from the assumptions made. For example, reserves and resources estimates and production forecasts are subject to revision as further technical information becomes available and economic conditions change. Due to economic developments, regulatory change and emissions reduction activity arising from climate concern and other factors, future commodity prices and other assumptions may differ from the forecasts used in the calculations.

Sensitivities to different variables have been estimated using certain simplifying assumptions. For example, lower oil and gas price or production sensitivities do not fully reflect the specific impacts for each contractual arrangement and will not capture all favourable impacts that may arise from cost deflation or savings. A detailed calculation at any given price or production profile may, therefore, produce a different result.

It is estimated that an 11% (2024 11%) reduction in revenue throughout each year of the remaining life of those assets, either as a result of adverse price or production conditions or a combination of each, would cause the recoverable amount to be equal to the carrying amount of goodwill and related net non-current assets of the oil production and operations segment. For the gas businesses a 9% (2024 6%) reduction would have the same result.

It is estimated that no reasonably possible change in the discount rate would cause the recoverable amount to be equal to the carrying amount of goodwill and related net non-current assets.

Transition businesses

The transition businesses goodwill relates to the acquisitions of Archaea Energy and Lightsource bp. Cash flows were derived from the approved business plans.

For Archaea Energy, cash flows are derived from the approved business plan, which covers the period up to 2050. To determine the value in use, approved business plan cash flows were discounted and aggregated with a terminal value.

For Lightsource bp, cash flows for a period of 10 years were discounted and aggregated with a terminal value. Management considers the use of 10 years of plan cash flows before adding a terminal value to be appropriate reflecting the maturity of the business with an early stage development portfolio and other aspects of business model changes such that 10 years reflected an appropriate ‘steady state’ of development project sales and other income from which terminal value cash flows could be determined.

The assumptions to which the impairment tests are most sensitive are for Lightsource bp, the solar project sell-down unit margin, terminal value growth rate and the discount rate and for Archaea Energy renewable natural gas prices, and the level of capital expenditure and its consequential impact on production volumes and discount rate. These assumptions are affected by market conditions. Discount rate assumptions are based on the group’s impairment discount rates as disclosed in Note 1. Other assumptions are based on management experience. The steady long-term growth rate used in the Lightsource bp goodwill impairment test terminal value is a risk-adjusted rate reflecting assumptions about inflation and project development growth.

It is estimated that a 1% decrease in the discount rates applied to the transition businesses would have resulted in a reduction to the goodwill impairment charges of $1.7 billion. It is estimated that a 1% increase to the discount rates would have resulted in an increase to the goodwill impairment charge of $0.9 billion.

These discount rate sensitivity analyses do not take into account any effect on the goodwill impairment test that would arise from first applying the changes in assumptions to the underlying assets of the businesses.

Lightsource bp project development margins could change as a result of changes in sales prices achieved, development costs incurred or changes in the number of projects sold. It is estimated that a 10% increase to project development unit margin would have resulted in a reduction to the goodwill impairment charge of $0.4 billion. It is estimated that a 10% decrease in project development unit margin would have resulted in an increase to the goodwill impairment charge of $0.5 billion. It is estimated that a 1% increase to the terminal value growth rate would have resulted in a reduction to the goodwill impairment charge of $1.0 billion. It is estimated that a 1% decrease in the terminal value growth rate would have resulted in an increase to the goodwill impairment charge of $0.6 billion.

These sensitivity analyses do not, however, represent management’s best estimate of any impairment charges or reversals that might be recognized as they do not fully incorporate consequential changes that may arise, such as changes in capital and operating costs, business plans and phasing of development. The above sensitivity analyses therefore do not reflect a linear relationship between development margins or growth rate and value that can be extrapolated. The interdependency of these inputs and factors limits the practicability of estimating the probability or extent to which the overall recoverable amount is impacted by changes to the price assumptions or production volumes.

Given the impairment charges taken in the year, the recoverable amount of the transition businesses CGUs’ goodwill is equal to its carrying amount. Therefore, no disclosures regarding what changes in assumptions would cause headroom to be eroded have been provided. Also reflecting that goodwill impairment reversals are not permitted by IFRS the sensitivities identified above are provided to give context to the estimates taken at December 2025. No reversals to goodwill would arise should the estimates be changed favourably in the year ended December 2026.

customers & products

Cash flows for each group of CGUs are derived from the business segment plans, which cover a period of up to five years. To determine the value in use for each of the groups of cash-generating units, cash flows for a period of 10 years, are discounted and aggregated with a terminal value. Pretax discount rates ranging from 10-12% are applied. It is estimated that no reasonably possible change in the key assumptions used in the US Fuels and European Fuels goodwill impairment assessments would cause the recoverable amount to be equal to the carrying amount of goodwill and related net non-current assets.

No material impairment of the goodwill balances in customers & products was recognized during 2025.

Castrol

The goodwill associated with Castrol was reclassified to assets held for sale during the year.