GlaxoSmithKline plc – Annual report – 31 December 2025

Industry: pharmaceuticals

Group financial review (extract 1)

Approach to tax

Business makes a major contribution to the public purse through its tax contribution. This includes direct taxes (such as corporate income tax) and indirect taxes (such as VAT, environmental taxes and customs duties) as well as other taxes (such as employment taxes and property taxes). It is therefore important that companies explain their approach to tax. This helps inform dialogue about tax and tax policy.

We are supportive of efforts to ensure companies are appropriately transparent about how their tax affairs are managed. To this end, our Tax Strategy (which includes a summary of our Total Tax Contribution (TTC) and country-by-country reporting (CBCR) data) is set out in detail within the Public policies section of our website and we regularly engage in discussions with stakeholders who are keen to understand our tax profile and our approach to tax.

As a global biopharmaceutical company, we have a substantial business and employment presence in many countries around the world and pay a significant amount of tax. This includes corporate income tax, other business taxes, and tax associated with our employees. We also collect a significant amount of tax on behalf of governments, such as income tax from payments to our employees and VAT along our supply chain. Further information in relation to GSK’s total tax contribution, giving a better reflection of our overall fiscal contribution in a particular country, can be found in our published Tax Strategy.

We are subject to taxation throughout our supply chain. The worldwide nature of our operations means that our cross-border supply routes, necessary to ensure supplies of medicines into numerous countries, can result in conflicting claims from tax authorities as to the profits to be taxed in individual countries. This can lead to double taxation (with profits taxed in more than one country).

To mitigate the risk of double taxation, profits are recognised in territories by reference to the activities performed there and the value they generate. To ensure the profits recognised in jurisdictions are aligned to the activity undertaken there, and in line with current OECD guidelines, we base our transfer pricing policy on the arm’s length principle and support our transfer prices with economic analysis and reports.

We do not engage in artificial tax arrangements – those without business or commercial substance. We do not seek to avoid tax by using ‘tax havens’ or transactions we would not fully disclose to a tax authority. We have a zero-tolerance approach to tax evasion and the facilitation of tax evasion.

Tax risk in all countries in which we operate is managed through robust internal policies, processes, training and compliance programmes. Our Board of Directors, supported by the Audit & Risk Committee (ARC), is responsible for approving our tax policies and risk management arrangements as part of our wider risk management and internal control framework. Our Risk Oversight and Compliance Council (ROCC) and the Audit and Assurance function help the ARC oversee tax risks and the strategies used to address them.

We seek to maintain open and constructive relationships with tax authorities worldwide, meeting regularly to discuss our tax affairs and real time business updates wherever possible to support their work and help manage tax risk in accordance with our framework.

We monitor government debate on tax policy in our key jurisdictions so that we can understand and share an informed point of view regarding any potential future changes in tax law, in support of a transparent and financially sustainable tax system. Where relevant, we provide pragmatic and constructive business input to tax policy makers either directly or through industry trade bodies, to help inform reforms that support economic growth and job creation.

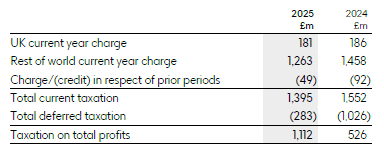

In 2025, the Group corporate tax charge was £1,112 million (2024: £526 million) on profits before tax of £7,401 million (2024: £3,477 million) representing an effective tax rate of 15.0% (2024: 15.1%). We made cash tax payments of £1,202 million in the year (2024: £1,307 million). In addition to the taxes we pay on our profits, we pay duties, levies, transactional and employment taxes.

The Group’s Total tax rate for 2025 of 15.0% (2024: 15.1%) was lower than the Core tax rate reflecting the different tax effects of various Adjusting items, including non-taxable revaluations of contingent consideration liabilities associated with recent acquisitions.

Our Core tax rate for 2025 was 17.1% (2024: 17.0%). The rate continues to benefit from innovation incentives available in key territories in which we operate, such as the UK and Belgium Patent Box regimes, albeit at a reduced level following introduction of global minimum corporate tax rate provisions, in line with the OECD’s Pillar Two model rules.

Further details about our corporate tax charges for the year are set out in Note 14, ‘Taxation’ to the financial statements.

Group financial review (extract 2)

Taxation

The charge of £1,112 million represented an effective tax rate on Total results of 15.0% (2024: 15.1%) and reflected the different tax effects of the various Adjusting items included in Total results, including non-taxable revaluations of contingent consideration liabilities associated with recent acquisitions. Tax on Core profit amounted to £1,584 million and represented an effective Core tax rate of 17.1% (2024: 17.0%). Issues related to taxation are described in Note 14, ‘Taxation’ to the financial statements. The Group continues to believe it has made adequate provision for the liabilities likely to arise from periods which are open and not yet agreed by tax authorities. The ultimate liability for such matters may vary from the amounts provided and is dependent upon the outcome of agreements with relevant tax authorities.

Principal risks and uncertainties (extract)

Financial controls and reporting

Risk definition

The risk that GSK fails to comply with current tax laws; fails to report accurate financial information in compliance with accounting standards and applicable legislation; or incurs significant losses due to treasury activities.

Risk impact

Non-compliance with financial, ESG or disclosure requirements, or deficiencies in internal controls during finance transformation and digital integration, could result in regulatory action, litigation and reputational harm and could materially and adversely affect our financial results. Transitional risks from system upgrades and acquisitions, combined with gaps in compliance culture, policy engagement or working capital management, increase the potential for fraud, error or inefficiency. Failures in safeguarding critical systems, managing third-party and banking dependencies, or overseeing data and AI risks could further lead to operational disruption, financial loss, and loss of stakeholder confidence.

Context

Externally, geopolitical tensions, economic uncertainty, stricter regulatory requirements, climate disruption and rapid technological change all drive higher scrutiny and operational complexity. Social expectations for transparency, ethical conduct and ESG disclosure continue to rise, reinforcing the link to reputational and compliance risks. Internally, large-scale transformation programmes – including SAP Enterprise Resource Planning evolution, acquisitions and digital initiatives – create interdependencies with third parties, offshore partners and banking counterparties. These connections heighten exposure to data, cyber and AI risks, while making governance, resilience and effective controls central to sustaining our financial integrity and long-term strategic objectives. The shift towards automation and technology-driven processes creates both efficiency and opportunities and risks from skills gaps, inadequate controls and evolving compliance expectations.

Mitigating actions

We keep up to date with the latest developments in financial reporting requirements by reviewing updates from regulators; working with our external auditor and legal advisors; and performing and responding to emerging risks. Financial results are reviewed and approved by regional management, before being reviewed by GSK’s Group Financial Controller and Chief Financial Officer (CFO). This allows our Group Financial Controller and CFO to assess the evolution of the business over time and to evaluate its performance to plan. Significant judgements are reviewed and confirmed by senior management.

We integrate technical or organisational transformation, newly acquired activities and external risks into our risk assessments and apply appropriate controls and reviews. We maintain a control environment designed to identify material errors in financial reporting and disclosure. We have a standardised global financial reporting operating model. Management’s testing process is designed to probe the design and operating effectiveness of key processes and controls within all five aspects of the Committee of Sponsoring Organizations of the Treadway Commission (COSO) framework.

The design and operating effectiveness of key financial reporting controls and ESG controls are regularly reviewed by management and tested by external third parties. The few locations which are not on the standard model apply a minimum standard set of controls which are reviewed by management and monitored independently. This gives us assurance that controls over key financial reporting and disclosure processes are operating effectively. Our Finance Risk Management & Controls team provides extra support during significant transformations, such as system or digital tool deployment or management/structural reorganisations. We add operational resources, provide training, and adapt programme timelines to ensure processes and controls are maintained during significant changes.

The Disclosure Committee, reporting to the Board, reviews our quarterly results and the Annual Report. Throughout the year, in consultation with its legal advisors, the Disclosure Committee also determines whether it is necessary to disclose publicly information about the Group through stock exchange announcements. The Treasury Management Group meets regularly to ensure that liquidity, interest rate, counterparty, foreign currency transaction and foreign currency translation risks are all managed in line with the prudent approach detailed in the risk strategies and policies adopted by our Board. Counterparty exposure is subject to defined limits approved by the Board for both credit rating and individual counterparties. The Middle Office within Treasury monitors the management of counterparty risk in line with agreed policy with oversight from a corporate compliance officer, operating independently of Treasury. Further details on mitigation of Treasury risks can be found on page 248.

We manage tax risk through robust internal policies, processes, training and compliance programmes and seek to maintain open and constructive relationships with tax authorities worldwide. To mitigate the risk of double taxation, profits are recognised in territories by reference to the activities performed and the value they generate in accordance with the Organisation for Economic Co-operation and Development’s (OECD) guidelines on the arm’s length principle and supported by economic analysis and reports. We monitor government debate on tax policy in our key jurisdictions, so that we can understand and share an informed point of view regarding potential future changes in tax law. Where relevant, we provide pragmatic and constructive business input to tax policymakers, either directly or through industry trade bodies, to help inform reforms to support economic growth and job creation.

Our tax affairs are managed by a team of tax professionals, led by the Global Head of Tax, who work closely with the business on a day-to-day basis. The Global Tax team is suitably qualified for the roles they perform, and we support their training needs so they can provide up to date technical advice in line with their responsibilities. We submit tax returns according to statutory time limits and engage proactively with tax authorities to ensure our tax affairs are current, entering co-operative compliance programmes and advance pricing agreements where appropriate to provide long-term certainty both for us and for tax authorities over the tax treatment of our business, based on full disclosure of all relevant facts. The complexity of tax regulations means that we may occasionally disagree with tax authorities on the technical interpretation of a particular area of tax law. We seek to resolve any differences of interpretation in tax legislation with tax authorities in a cooperative manner. In exceptional cases, we may have to resolve disputes through formal proceedings to establish clarity for all stakeholders.

3. Critical accounting judgements and key sources of estimation uncertainty (extract)

Taxation

The tax charge for the year was £1,112 million (2024: £526 million). At 31 December 2025, current tax payable was £498 million (2024: £703 million), and current tax recoverable was £288 million (2024: £489 million).

Judgement and estimate

The Group has open tax issues with a number of revenue authorities. Management makes a judgement of whether there is sufficient information to be able to make a reliable estimate of the outcome of the dispute. If insufficient information is available, no provision is made.

If sufficient information is available, in estimating a potential tax liability GSK applies a risk-based approach which takes into account, as appropriate, the probability that the Group would be able to obtain compensatory adjustments under international tax treaties. These estimates take into account the specific circumstances of each dispute and relevant external advice, are inherently judgemental and could change substantially over time as each dispute progresses and new facts emerge.

At 31 December 2025, the Group had recognised provisions of £649 million in respect of uncertain tax positions (2024: £636 million). Due to the number of uncertain tax positions held and the number of jurisdictions to which these relate, it is not practicable to give meaningful sensitivity estimates. No uncertain tax position is individually material to the Group.

Factors affecting the tax charge in future years are set out in Note 14, ‘Taxation’. GSK continues to believe that it has made adequate provision for the liabilities likely to arise from open assessments. Where open issues exist, the ultimate liability for such matters may vary from the amounts provided and is dependent upon the outcome of negotiations with the relevant tax authorities or, if necessary, litigation proceedings.

14. Taxation (extract 1)

As a global biopharmaceutical company, we have a substantial business and employment presence in many countries. The impact of differences in overseas taxation rates arose from profits being earned in countries with tax rates differing from the UK statutory rate, the most significant of which in 2025 was the US. This favourable impact was complemented by the benefit of intellectual property incentives such as the UK Patent Box and Belgian Innovation Income Deduction (IID) regimes, which provide a reduced rate of corporation tax on profits earned from qualifying patents. We claim these incentives in the manner intended by the relevant statutory or regulatory framework. Global minimum corporate income tax rules in the UK and Belgium (in line with the OECD’s Pillar Two framework) reduced the benefit of these incentives by £169 million.

14. Taxation (extract 2)

The deferred tax asset of £3,008 million (2024: £2,449 million) recognised on tax losses relates to trading losses. Such deferred tax assets are only recognised to the extent Group long-range forecasts indicate sufficient future taxable profits will be available to utilise such assets (forecast by around 2030). Other net temporary differences included accrued expenses for which a tax deduction is only available on a paid basis. The Group has adopted the mandatory temporary exception to the recognition and disclosure of deferred taxes arising from the jurisdictional implementation of the Pillar Two model rules, as required under IAS 12.

14. Taxation (extract 3)

Issues relating to taxation

We are subject to taxation throughout our supply chain. The worldwide nature of our operations means that our cross-border supply routes, necessary to ensure supplies of medicines into numerous countries, can result in conflicting claims from tax authorities as to the profits to be taxed in individual countries. This can lead to double taxation (with the same profits taxed in more than one country). To mitigate the risk of double taxation, profits are recognised in territories by reference to the activities performed there and the value they generate. To ensure the profits recognised in jurisdictions are aligned to the activity undertaken there, and in line with current OECD guidelines, we base our transfer pricing policy on the arm’s length principle and support our transfer prices with economic analysis and reports. The Group also has open items in several jurisdictions concerning such matters as the deductibility of particular expenses and the tax treatment of certain business transactions. GSK applies a risk-based approach to determine the transactions most likely to be subject to challenge and the probability that the Group would be able to obtain compensatory adjustments under international tax treaties.

The calculation of the Group’s total tax charge therefore necessarily involves a degree of estimation and judgement in respect of certain items whose tax treatment cannot be finally determined until resolution has been reached with the relevant tax authority or, as appropriate, through a formal legal process. At 31 December 2025, the Group had recognised provisions of £649 million in respect of such uncertain tax positions (2024: £636 million). The increase in recognised provisions during 2025 was driven by the reassessment of estimates, net of the impact of agreement of a number of open issues with tax authorities in various jurisdictions. Whilst the ultimate liability for such matters may vary from the amounts provided and is dependent upon the outcome of agreements with the relevant tax authorities, or litigation where appropriate, the Group continues to consider that it has made appropriate provision for periods which are open and not yet agreed by the tax authorities.

A provision for deferred tax liabilities of £178 million as at 31 December 2025 (2024: £159 million) has been made in respect of taxation that would be payable on the remittance of profits by certain overseas subsidiaries. Whilst the aggregate amount of unremitted profits at the balance sheet date was approximately £18 billion (2024: £18 billion), the majority of these unremitted profits would not be subject to tax (including withholding tax) on repatriation, as UK legislation relating to company distributions provides for exemption from tax for most overseas profits, subject to certain exceptions. Deferred tax is not provided on temporary differences of £739 million (2024: £696 million) arising on unremitted profits as management has the ability to control any future reversal and does not consider such a reversal to be probable.